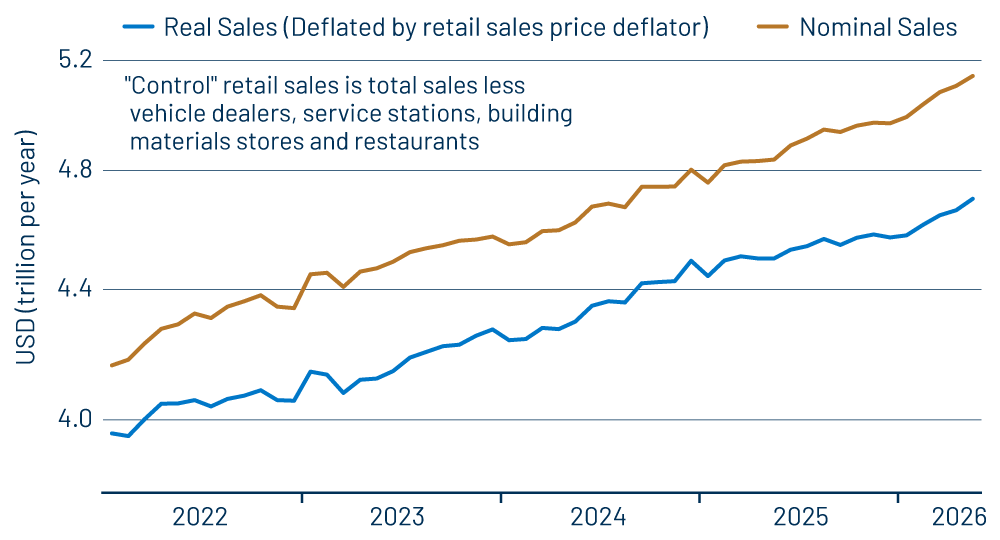

Headline retail sales rose 0.9% non-annualized in May, with the April sales estimate seeing essentially no revision. We and other analysts focus on a “control” sales measure that excludes sales at gas stations, car dealers, building material stores and restaurants, partly because of the short-term volatility in these sectors and partly because these sectors sell to businesses as much as consumers, and our focus here is on consumer spending. That control measure also rose nicely, up 0.7% in May, with a +0.1% revision to the April sales estimate.

In other words, while higher gas prices helped boost the headline gain, there was plenty of sales growth outside the fuel sector, where price gains were likely small or zero. As we mentioned last week with respect to the May Consumer Price Index (CPI), core goods prices within the CPI declined slightly in May. If that reported decline indeed held for retail prices, real control spending rose a very smart 0.8% in May, as indicated in Exhibit 1.

As we have mentioned repeatedly in recent posts concerning inflation and consumer spending, the CPI and Personal Consumption Expenditures (PCE) inflation measures have been showing vastly different rates of change in goods prices other than food and energy over the last six months, whereas historically they closely cohered prior to December 2025. Furthermore, budget cuts caused the Commerce Department to cease publishing a price index for retail sales exactly two years ago. Since then, our estimates of retail prices used to produce real control sales estimates have had to be based on CPI data, which, recently, again, have diverged from what PCE data are indicating. Bottom line, the real sales data shown in Exhibit 1 have been questionable over the last six months, but they are the best we can do with available information.

What we do know is that nominal sales have accelerated since January, after they had softened slightly in late 2025. Real sales have at least held steady and may have accelerated as well. Just four months ago, analysts were lamenting a possible slowing in retail sales and in consumer spending even as the Iran conflict was breaking out. We were more circumspect about the state of the consumer, given that consumer fundamentals were more positive and that the reported slowing then could have been related to holiday season vagaries. That contrary opinion has been vindicated by the data since then.

Where have sales picked up since January? Almost everywhere. The only retail sectors not showing a significant bounce in sales growth on net over the last four months are furniture, apparel and drug stores, yet these have at least held steady. Meanwhile, there have been very strong sales gains at building material, electronics and sporting/recreation stores, as well as online vendors. It is true that online sales have grown much faster than sales overall, a reflection of both ongoing trends and the recent surge in fuel prices that encourages online shopping. Still, one or two years ago, strong sales gains at online vendors were accompanied by generally sluggish sales at brick-and-mortar retailers. The latter have seen better results lately while online sales have also picked up.

Starting next month, fuel prices will likely turn to the downside, pulling service station sales lower, a reversal of recent results. However, our guess is that sales elsewhere will continue to grow, sustaining decent or good growth in control sales and its components.