In recent weeks, we’ve discussed the factors fueling the sharp bear-steepening of the US Treasury (UST) yield curve and the potential impact of higher interest rates on credit markets. The principal concern is that a “higher-for-longer” rate environment could further dent corporate valuations, raise worries about issuer refinancing and default risk and even pose the risk of destabilizing another area of the economy. Despite these concerns, we maintain a positive outlook for credit markets for three main reasons:

- Recent statements from Fed Chair Jerome Powell and other Fed governors indicate a more cautious approach to monetary policy, strengthening our conviction that the Fed likely will refrain from further rate hikes.

- The US economy is supported by a robust corporate sector and resilient consumer base which should allow the economy to slow without slipping into negative growth (i.e., recession). Moreover, companies have been proactively preparing for an anticipated recession, fortifying their balance sheets to withstand potential economic challenges.

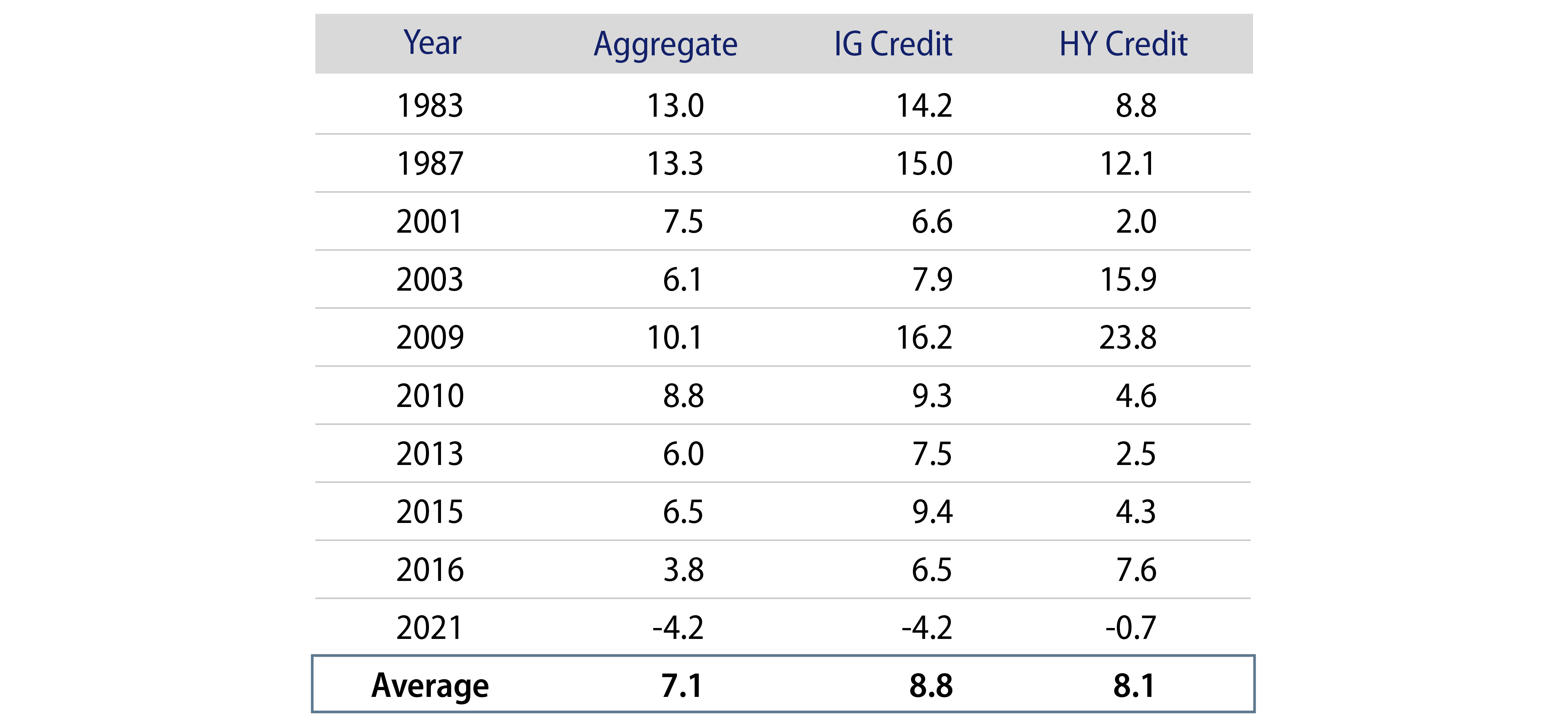

- Historical data spanning a 40-year period reveals that fixed-income, especially corporate credit, has consistently shown strong performance following periods of UST bear-steepening. This historical trend adds to our optimism regarding the resilience of corporate credit in the face of UST volatility.

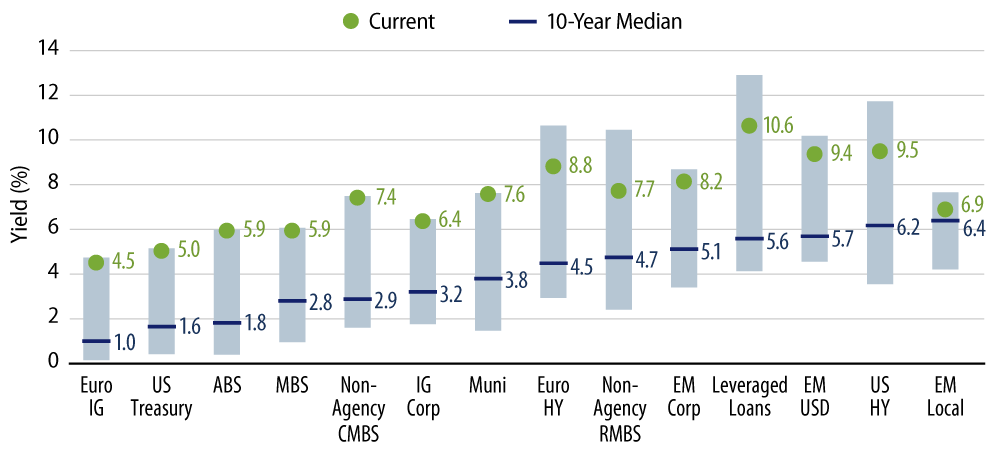

As highlighted in Exhibit 2, all fixed-income options are currently more appealing due to higher overall yields and higher income generation. We think credit is the way to take advantage of this environment due to the considerable spread above the risk-free rate, coupled with a supportive fundamental backdrop. More importantly, while attractive income serves as the main driver for investor returns, there is also the potential for additional returns if UST rates continue to rally or if spreads tighten further.

Given our outlook at this time, we have biased our multi-asset credit portfolios to seek to take advantage of the opportunity in higher quality credit. We believe the risk/reward potential of owning high-quality high-yield and investment-grade corporates remains an attractive opportunity for investors despite the already strong performance year to date (YTD). Higher quality allows investors to still capitalize on the generous yields in today’s fixed-income market, but also to endure a downturn should the economy slip into recession (though this is not our base case). We also believe commercial real estate is likely to present an opportunity later in the year and we are allocating significant resources to that sector in preparation.

Here we highlight the opportunities we see in each of the following fixed-income asset classes:

- High-yield credit: In the US, yields around 9% are providing significant cushion to offset modestly higher defaults as peak fundamentals adjust to higher rates and slower growth. We continue to see opportunity in service-related sectors such as airlines, cruise lines and lodging, and remain cautious on companies that have closer ties to housing-related activity which therefore lack pricing power. In Europe, corporate fundamentals are decent based on recent earnings, and we view yields north of 8% as fair. Given more macro headwinds, we are more focused on higher quality new issues and short-dated yield-to-call opportunities.

- Bank loans and CLOs: The loan market has delivered double-digit returns YTD and continues to benefit from strong technical demand due to collateralized loan obligation (CLO) issuance. We favor defensive sectors that have strong competitive positions, less cyclical industry dynamics and decent asset coverage. These include health care, property & casualty brokerage and environmental waste management companies. In the CLO space, we continue to see value in AAA rated tranches, which are currently offering yields north of 6%. With the structural protections of CLOs, an AAA rated security can absorb 60%-80% of the loan portfolio defaulting without taking a loss, which is well in excess of our expectations for a default rate of 3.5%-4.0% over the next year.

- Investment-grade credit: While yields on US investment-grade credit remain elevated, spread levels remain fair. We continue to maintain overweight positions to banking, energy and select reopening industries. In Europe, corporate fundamentals are deteriorating in some sectors, albeit from a strong level. Higher European government yields may ultimately be problematic for credit but after a firm 3Q23, spreads look reasonably attractive on a historical basis, particularly for shorter maturity paper.

- Mortgage and consumer credit: In the residential mortgage-backed securities (RMBS) space, we’re opportunistic on credit risk transfer (CRT) securities as well as non-QM deals that present attractive borrower profiles and higher credit qualities. In the commercial MBS (CMBS) space, low leverage exposures on high-quality real estate with meaningful borrower equity present compelling opportunities to lend in both the conduit and single-asset single-borrower (SASB) market. New origination screens particularly attractive on a yield versus credit risk basis; however, some high-quality seasoned credits offer attractive total return opportunities.

- EM debt: Yields across the emerging market (EM) asset class are near decade highs. While we’ve maintained a constructive outlook for EM, we’ve also maintained a cautious stance given the greater vulnerability of the asset class to US rate volatility, US dollar strength and geopolitical risk. That stated, we see US macro conditions and interest-rate dynamics aligning with our expectations and a Fed that appears to be adopting a more cautious stance on policy tightening. All of these factors lead us to the conclusion that EM (e.g., local market and frontier market debt) now looks compelling from a risk/return perspective.

In Closing

Throughout this year, credit markets have demonstrated impressive resilience despite challenges such as extraordinary UST volatility, unexpected economic data and geopolitical turmoil. Looking ahead, we have the US presidential election and a number of pivotal elections across other parts of both the developed market (DM) and EM world that could introduce additional uncertainties. That stated, we think the cloud of uncertainty that has been hanging over credit markets the past year—particularly the risk of Fed overtightening—appears to be lifting. We believe this clearer outlook should set the stage for credit outperformance as we move into 2024.