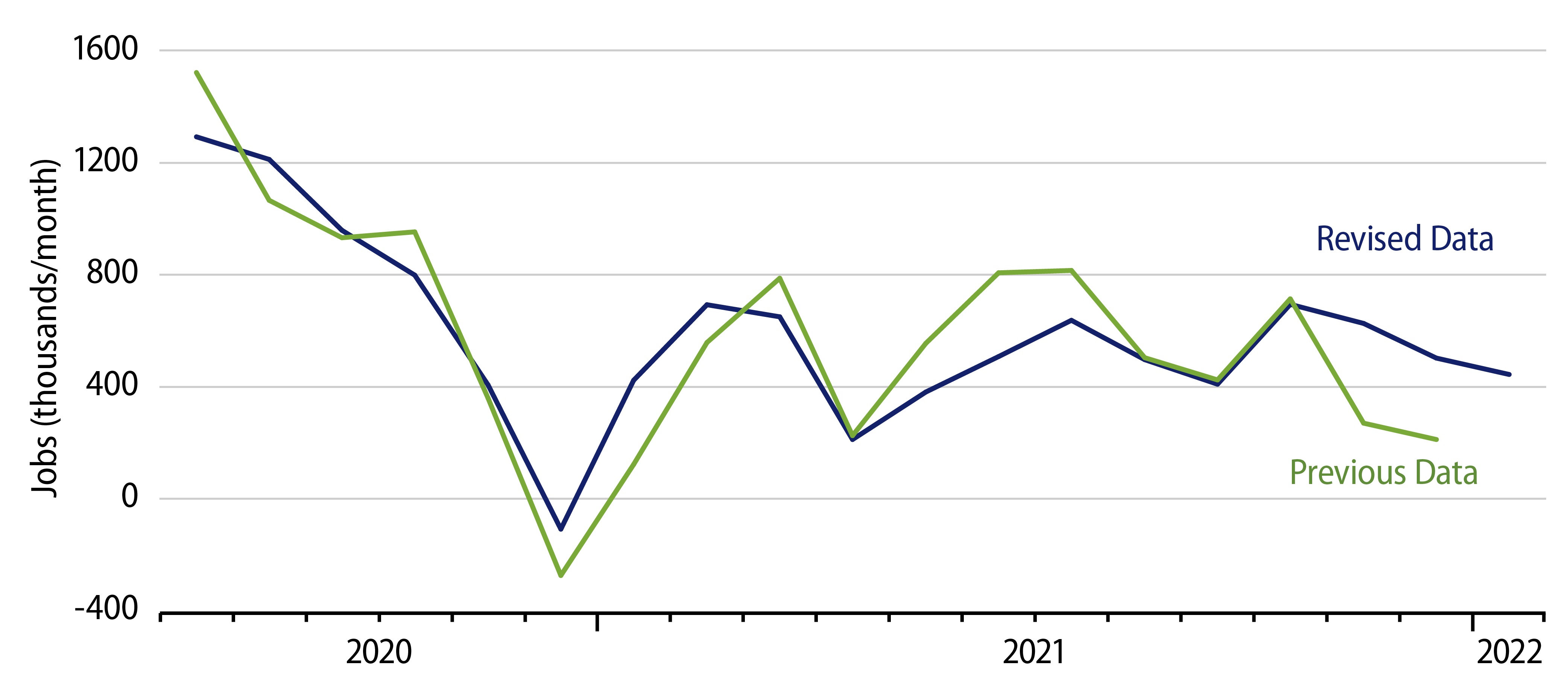

At one point In Lewis Carroll’s Alice In Wonderland, Alice finds she has to run faster and faster just to stay where she is. We were reminded of that when viewing today’s jobs data and related revisions. Early media headlines have trumpeted the fact that late-2021 job growth is now estimated to be “much stronger” than previously reported. What those headlines didn’t mention is that growth in mid-2021 and late-2020 is now expected to be much slower than previously reported. On net, the estimated level of jobs for December 2021 was revised downward by 2,000 jobs, 0.0016%. In other words, all those revisions leave us basically back where they said we were one month ago.

Jobs in construction, manufacturing, food service, recreation and accommodations were revised down. Jobs in health care, passenger travel and other sectors were revised up, with those changes, again, netting to essentially zero.

Granted, there were some changes in the pattern of employment growth. The chart we showed here a month ago indicated generally slowing job over the last half of 2021, as the red line in the chart here suggests. With the revisions, growth now looks more stable across 2021.

In previous data, restaurants, recreation and accommodations had all shown a flurry of job growth over the first half of 2021, followed by near-zero growth in the second half, suggesting that these sectors had grown as much as they could given the lingering Covid restrictions they were still operating under. These sectors now show stable growth throughout 2021, at a lower cumulative rate, suggesting they might grow further even under the current restrictions. Other sectors of the economy display the net changes mentioned earlier, slower growth in late-2020 and mid-2021, but less slowing recently.

A month ago, we were skeptical that omicron had anything to do with the slower growth reported then, as the slowing trends, again, had been in place since July. The more stable growth pace in the current data again still contradicts any suggestion that omicron has been a meaningful hit to date for the job markets.

Also in the post a month ago, we suggested that labor force participation would continue to rise, now that extended unemployment benefits have expired. This did occur in January, with the labor force participation rate rising by 0.3 percentage points. In fact, in the household survey, the 393,000 increase in the labor force was larger than the 199,000 gain reported for jobs, resulting in a slight increase in unemployment.

We had been looking for jobs gains around 300,000 per month, based on the belief that food service and leisure industries would show essentially zero growth. With some prospective growth now in place for these sectors, and with revisions elsewhere, it now looks likely that job growth could sustain around 450,000 per month.

Even at that rate, it will still take another two years for the economy to re-attain pre-Covid job growth trends. However, that better possible growth—next to our projected further increases in labor force participation—now stands to hold unemployment rates stable, rather than the modest increases in unemployment we thought likely a month ago.