Central bank reserve managers around the world are increasingly being pushed beyond traditional US Treasury-heavy investment frameworks, as higher structural rates, more volatile geopolitical conditions and pressure to generate incremental income reshape reserve portfolio construction. This is particularly true for investment tranches of central bank portfolios, where the objective is earning reasonable income and preserving capital without compromising liquidity or credit quality. In that environment, agency mortgage-backed securities (MBS) deserve a closer look.

Agency MBS are securities collateralized by residential mortgage loans, issued and guaranteed by Fannie Mae, Freddie Mac or Ginnie Mae—agencies with US government backing. The agency MBS market is one of the largest fixed-income markets in the world, supported by broad institutional participation and active secondary-market trading. That combination gives reserve managers access to a large, liquid and high-quality segment of the US dollar fixed-income market with yield advantage over Treasuries.

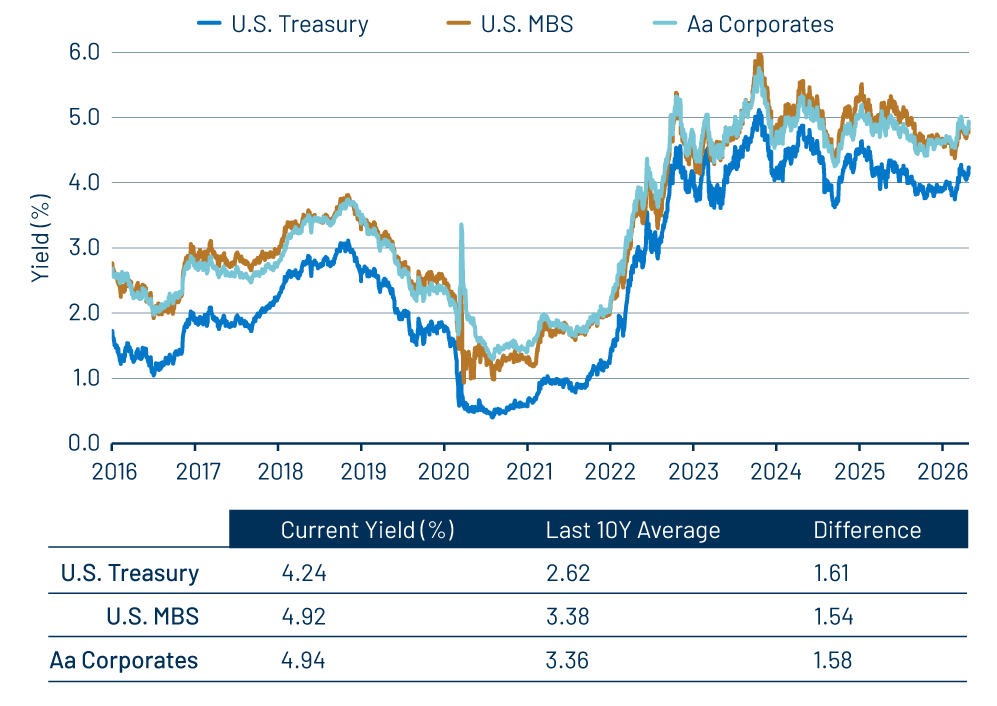

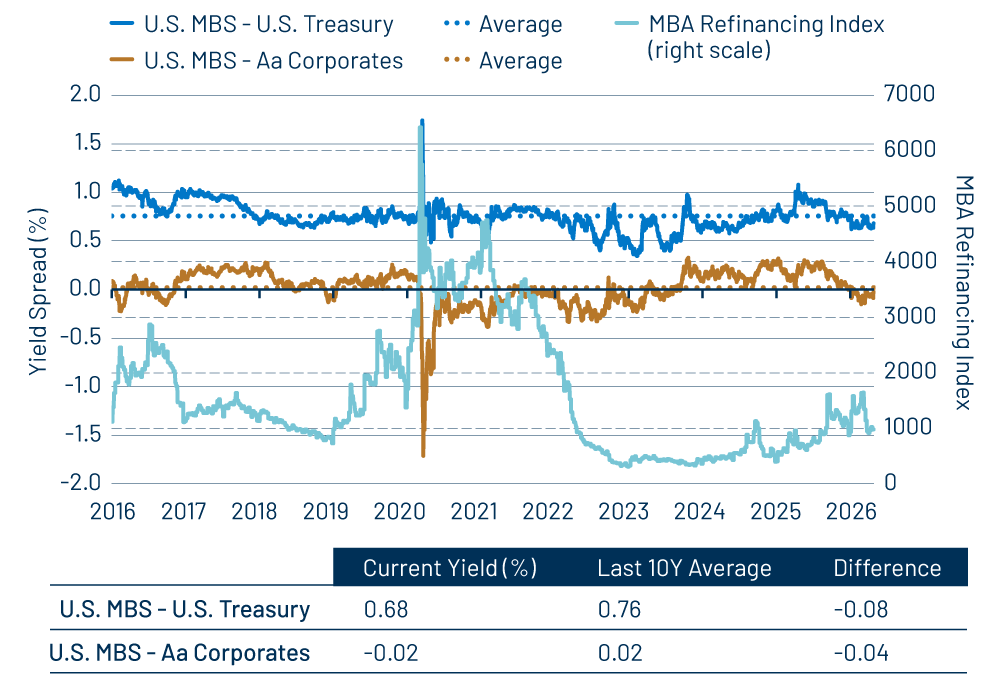

Today’s market backdrop looks different from the post-Global Financial Crisis era, or the Covid pandemic when large-scale Federal Reserve (Fed) purchases compressed spreads and reduced relative value opportunities in agency MBS. Following the Fed’s tightening cycle during 2022-2024, the Fed and US banks’ purchases turned to run-off, yield levels increased and agency MBS spreads widened relative to Treasuries and high-quality corporate bonds. Even after the broader fixed-income rally in 2025, agency MBS spreads remain attractive in early 2026. The yield of guaranteed agency MBS is similar to that of the same credit quality corporate bonds, while the yield advantage over Treasuries is compelling in the context of limited refinancing activity.

The yield advantage of agency MBS compensates for prepayment risk, as US mortgage borrowers can repay their mortgage loans in full or in part at any time prior to maturity. This risk factor is tied less to corporate solvency and more to prepayment behavior. This matters because many reserve managers remain understandably cautious about moving further out the risk spectrum. Investment-grade corporate bonds may offer additional spread, but they also introduce exposure to the credit cycle and sector-specific stress. In this context, agency MBS occupies a middle ground between pure sovereign exposure and higher-spread credit sectors. They can complement Treasury holdings without forcing reserve managers into traditional credit risk.

Unlike many other spread sectors, the agency MBS market is deeply tied to consumer confidence, household wealth, banking-system stability and the effectiveness of monetary policy itself. Housing remains one of the most systemically important sectors of the US economy, and agency MBS sits close to the center of that financial plumbing. That systemic importance has historically reinforced the market’s institutional depth and policy relevance during periods of stress—a point reserve managers should not overlook.

Of course, agency MBS carry negative convexity, meaning expected principal and interest cash flows can change as interest rates move. When rates decline, mortgage refinancing activity can accelerate, causing investors to receive principal back sooner than expected. When rates rise, refinancing slows and durations can extend. That extension risk can become uncomfortable in periods of higher interest rate volatility. However, higher rates also work to stabilize the agency MBS market as origination supply, refinancing and prepayment activity drops, and agency MBS income potential becomes more predictable.

Official institutions need to approach the asset class carefully, particularly around coupon selection, benchmark construction, liquidity and duration management. At present, agency MBS allocations remain relatively modest in reserve portfolios compared with Treasuries, while central banks have been gradually broadening the range of eligible reserve assets over the past several years. The World Bank’s RAMP survey on reserve management practices found that MBS are increasingly appearing within eligible reserve investment frameworks, while OMFIF’s Global Public Investor survey showed reserve managers increasingly looking at broader government and quasi-government sectors as part of their reserve allocation process. Additionally, the Fed’s custody holdings for foreign official and international accounts showed over $325 billion in US government agency MBS securities as of April 2026, reinforcing active participation.

In our view, agency MBS fit naturally into the broader evolution taking place in reserve management. The discussion isn’t about replacing Treasuries. It’s about whether reserve managers are using the full US high-quality fixed-income toolkit more deliberately in a world where liquidity, resilience and income generation increasingly need to coexist. For institutions with sufficient reserve buffers and clearly defined investment tranches, agency MBS may offer a more compelling balance between those objectives.

For interested readers, we also highlighted key features of the asset class in our paper, The Advantages of Agency Mortgage-Backed Securities.