The supply of new asset-backed securities (ABS) has been rising steadily in the past few years, driven by sectors such as autos, digital infrastructure and solar. The ABS market is expected to see increased issuance again in 2024, to the tune of at least $280 billion, surpassing 2021 local highs of around $270 billion, according to JPMorgan. At a time when consumer deposits have declined and banks face funding pressure, lenders are seeking alternative financing sources. Some lenders are even turning to securitization of auto loans as an efficient method of reducing risk. At least $10 billion of ABS were sold last year from banks and credit unions in various forms. Auto ABS issuance is expected to continue to be elevated in 2024 as auto lending risk shifts to non-banks. Newer asset classes such as digital infrastructure and renewable energy have grown exponentially in the past several years, driven by growth in data storage and clean energy, creating opportunities for investors. Investor demand for longer-duration assets is on the rise as a result of the growing demand from insurance investors as well as asset managers, especially as monetary policy is at a turning point.

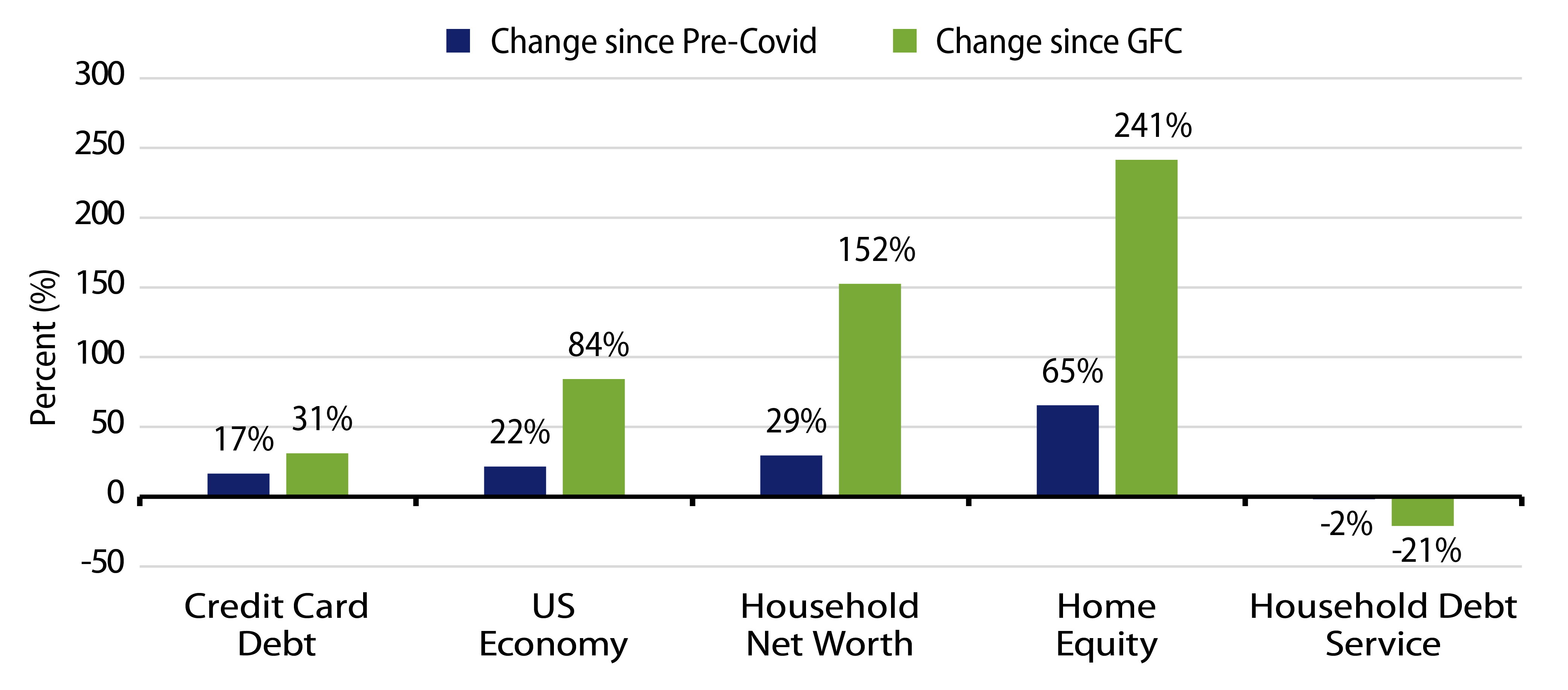

US consumer fundamentals are strong and we expect them to remain sound overall in 2024. Consumer spending has been a source of strength, supporting corporate earnings and fueling the economy. The labor market has rebalanced and continues to remain tight as healthy job growth supports the consumer, while layoff rates remain low relative to their historical averages. Strong wage growth continues to support incomes. Consumers are still resting on ample excess cash to last throughout 2024, although this has been less impactful with regard to consumer spending. Aggregate household balance sheets have strengthened following the recent increase in asset prices, and household net worth relative to disposable personal income remains near its all-time high. Consumer credit growth has slowed from the rampant pace in early 2023 and household leverage and debt service costs remain low by historical standards.

Our outlook for the consumer has been positive but cautious for some time. As consumer balance sheets remain robust, and weakness (higher borrowing costs/tighter lending) has been insulated, we turn more constructive on consumer performance and sector spreads for 2024, especially as monetary policy is set to change course. Auto delinquencies have been increasing toward pre-Covid levels on a normalization trajectory, but now appear to be on a flattening trend, suggesting the pace of deterioration is declining. Credit card delinquencies continue to rise beyond pre-Covid levels, driven by young borrowers entering the workforce and those that haven’t built wealth. We expect delinquencies to peak this year and slowly come down over time as tighter lending standards take effect. The student loan moratorium has ended, but borrower payments have yet to return to pre-pandemic levels. We expect a more gradual return to repayments into late 2024, while the new Saving on a Valuable Education (SAVE) repayment program is expected to reduce payments for low-income borrowers in need.

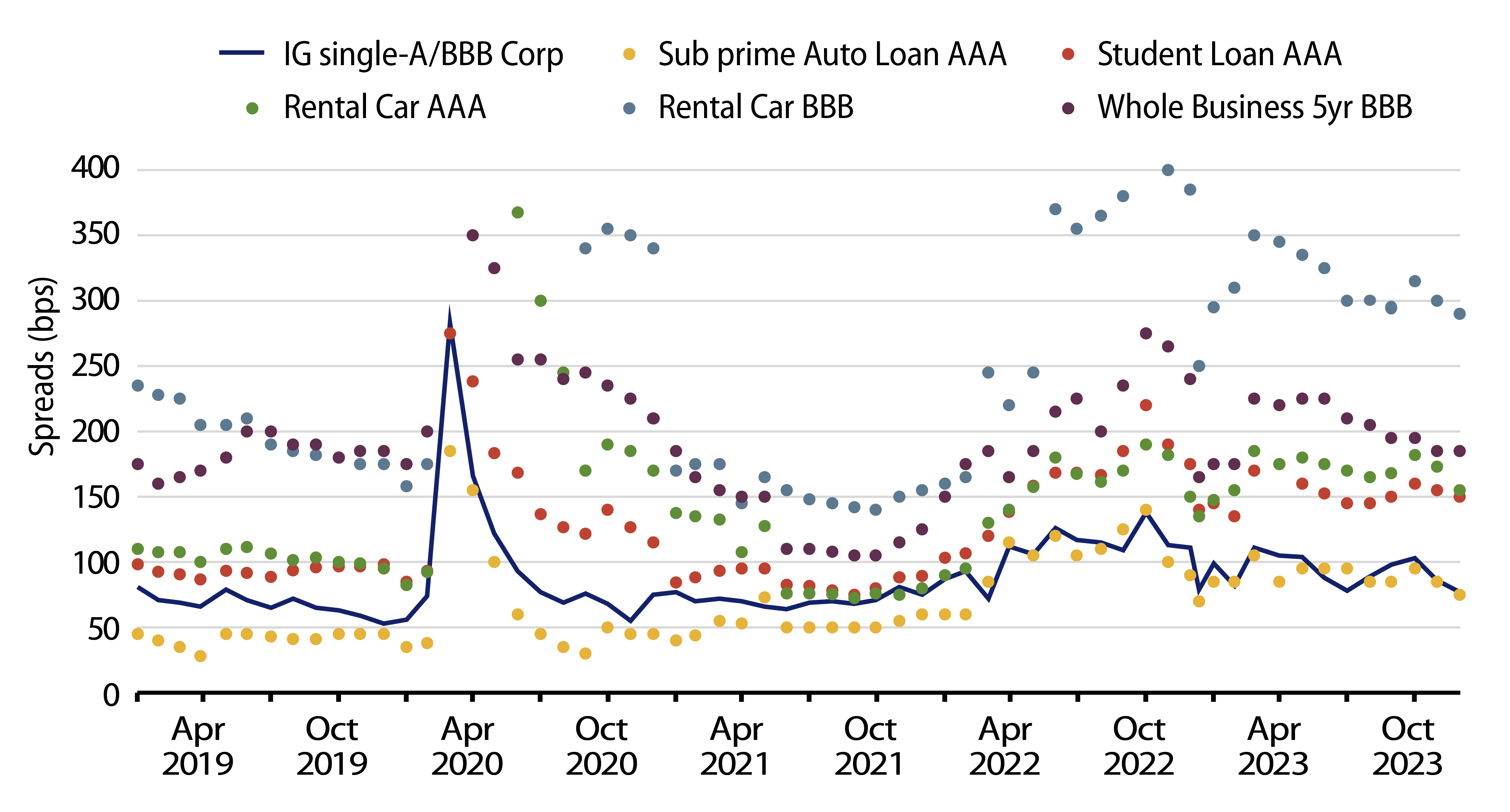

ABS spreads remain attractive as they continue to lag those of investment-grade credit. Specialty ABS sectors and mezzanine risk have seen more limited spread tightening, but they are currently wider than both investment-grade and high-yield spreads, providing a pickup of 50 to 100 bps from pre-Covid levels. Deal structures continue to remain generally robust, with rating agencies self-policing their own rating methodologies. Rating downgrades since the pandemic have been limited.

As issuer and sector tiering compresses further in 2024, forecasting divergence in performance will be crucial in discerning winners from losers, making active management an important differentiator among asset managers. Sector and issuer selection will be imperative as we identify unique opportunities for different investment styles and risk appetites.