Macros, Markets and Munis

Municipals posted negative returns last week, in line with most fixed-income sectors, as markets shifted focus to Federal Reserve (Fed) policy dynamics alongside mixed economic data. As confirmation hearings for Fed Chair nominee Kevin Warsh continued, the Fed held rates unchanged. Notably, the meeting featured an elevated level of dissent, as four members broke from the majority, with three objecting to an easing bias in light of higher energy prices. On the economic front, first-quarter GDP rose to 2.0% and core Personal Consumption Expenditures (PCE) moved higher as expected. Meanwhile, US Treasury yields moved higher across the curve, with rates rising approximately 10 basis points (bps) in shorter maturities and 5 bps in longer maturities, resulting in a flatter curve. Municipal bonds generally followed suit, with the curve exhibiting a similar flattening bias, and supply and demand both remained elevated. This week we provide a muni market review for the month of April.

Muni Demand Remained Steady Amid Elevated Supply Conditions

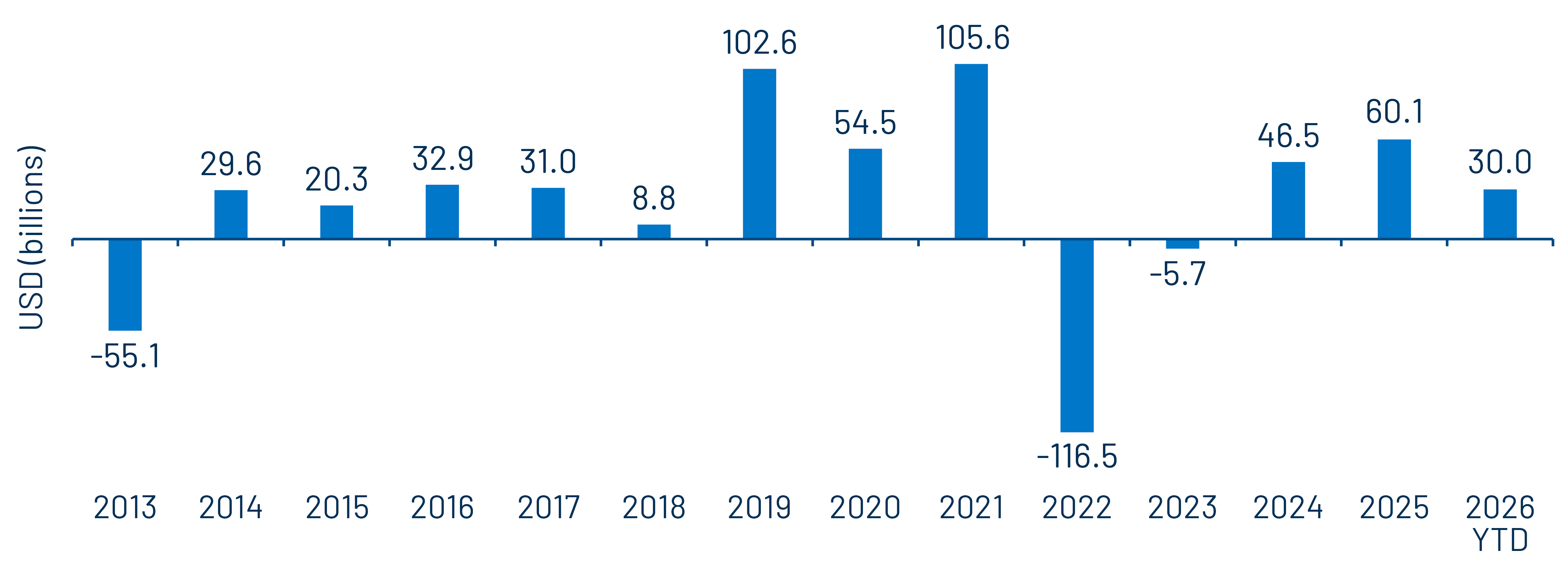

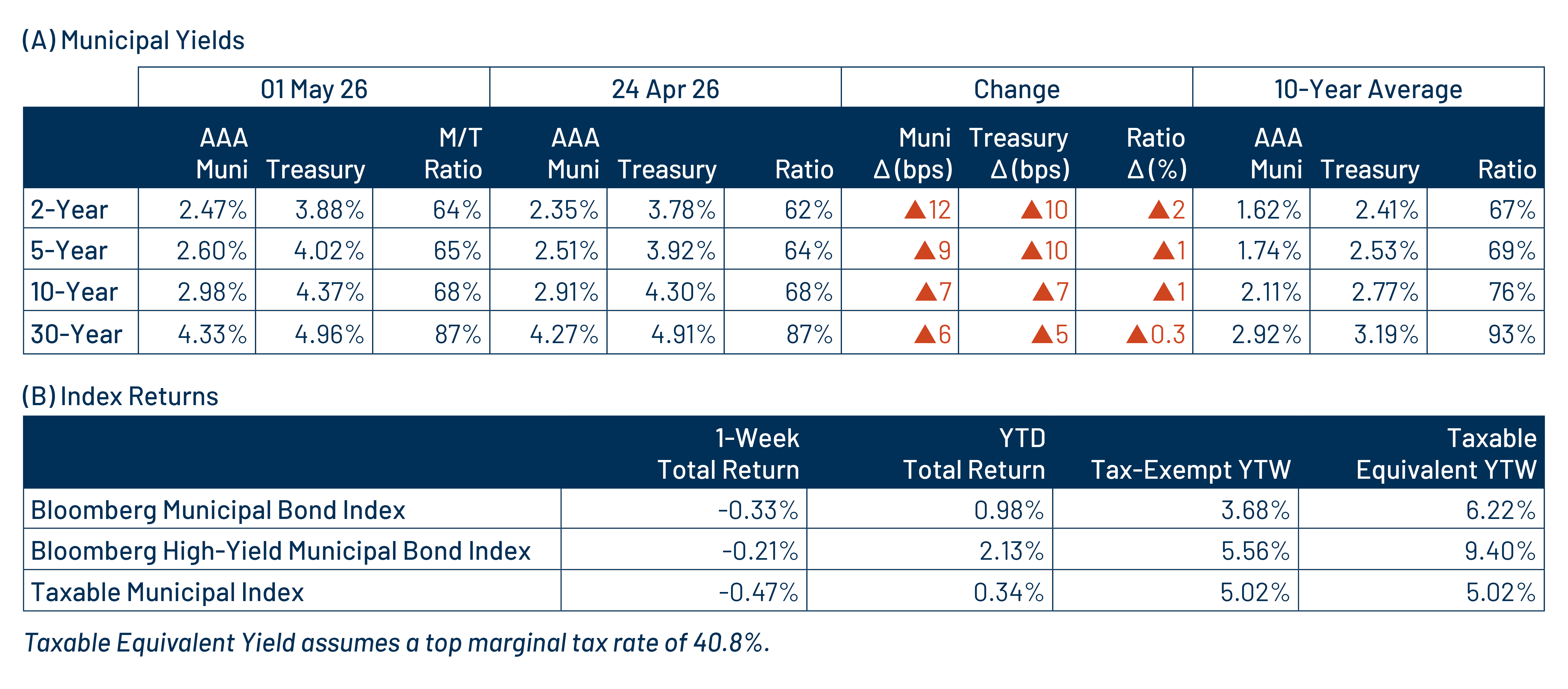

Fund Flows ($615 million of net inflows): During the week ending April 29, weekly reporting municipal mutual funds recorded $615 million of net inflows, according to Lipper. The long-term category recorded $196 million of inflows, the intermediate category reported $233 million of inflows and the short-term category recorded $85 million of net inflows. Last week’s inflows bring year-to-date (YTD) inflows to $30 billion.

Supply (YTD supply of $185 billion; up 17% YoY): The muni market recorded $10 billion of new-issue supply last week, down 20% from the prior week. YTD new-issue supply of $185 billion is 17% higher than the prior year, with tax-exempt issuance up 18% year-over-year (YoY) and taxable issuance up 10%, respectively. This week’s calendar is expected to pick up to $13 billion. Largest deals include $750 million Oklahoma City Public Property Authority and $400 million City of Philadelphia transactions.

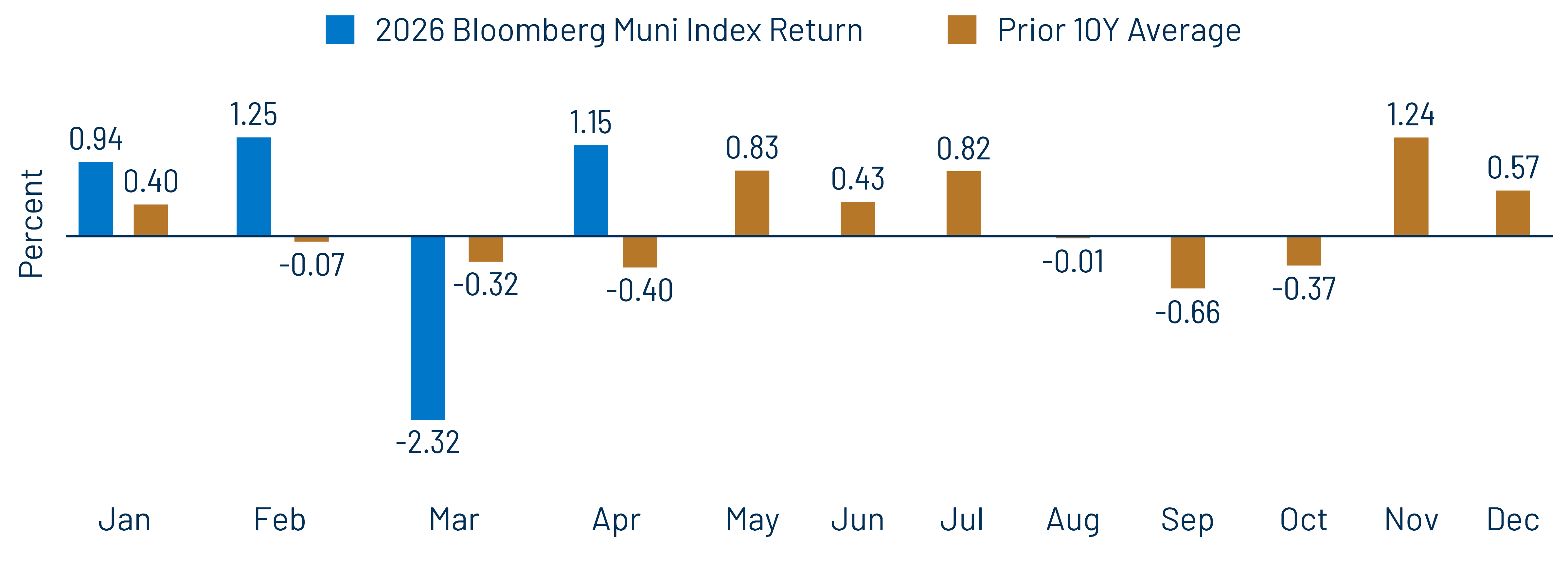

This Week in Munis: April Rebound

Fixed-income markets were focused on escalating geopolitical tensions in April, as rising oil prices fueled concerns about inflation. While ceasefire agreements provided some optimism early in the month, Treasury yields ultimately moved higher amid stalled diplomatic progress and uncertainty surrounding the Fed leadership transition. In total, Treasury yields increased by 5-8 bps across the curve. Municipals shrugged off the negative returns seen in taxable fixed-income markets, as well as the traditional technical weakness that typically pressures the asset class in April. High-grade municipal yields rallied 8-16 bps across intermediate and shorter maturities during the month, and the Bloomberg Municipal Bond Index returned 1.15%. The rebound from March’s steep underperformance led YTD returns back into positive territory at 0.97%.

Municipal technicals began the month on weaker footing as tax season concluded, but improved as April progressed. April new issuance was elevated at $51 billion, slightly below the $53 billion recorded both in March and April of 2025. Demand remained firm, with municipal mutual funds recording approximately $5 billion of net inflows during the month, largely comprised of long-term fund flows, according to Lipper. YTD inflows reached approximately $30 billion through April, which if sustained through year-end would outpace the prior year’s demand trend.

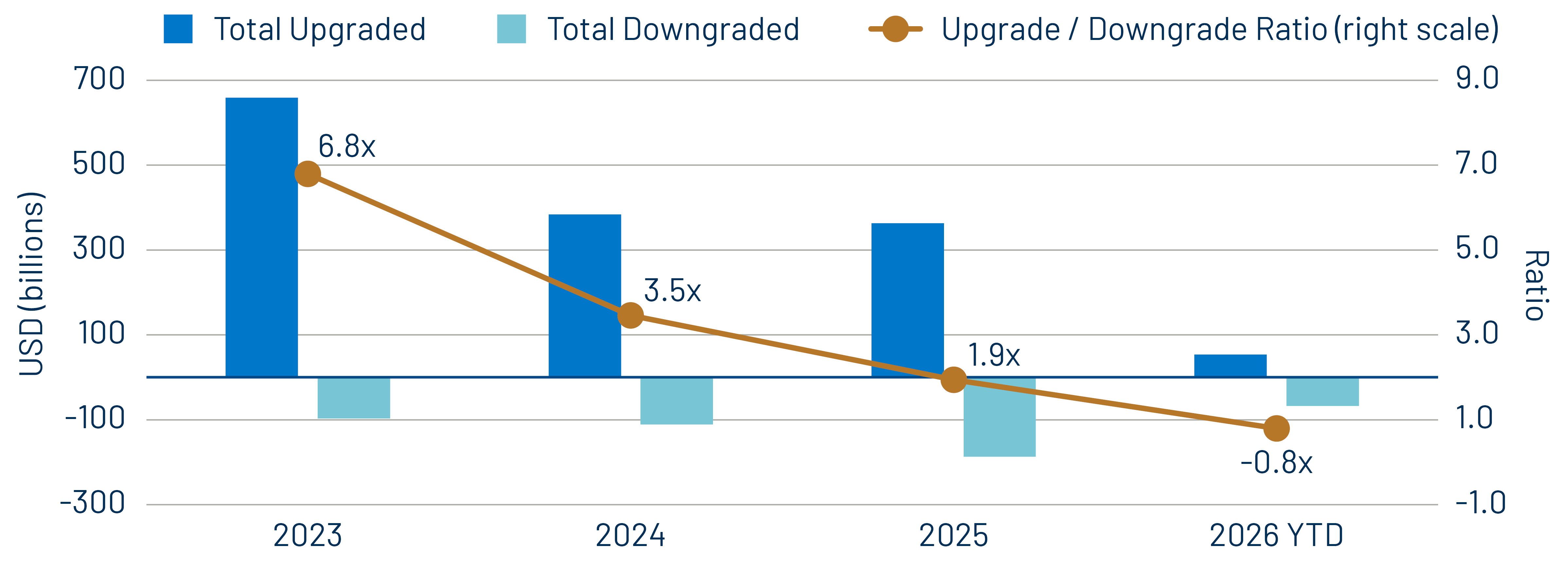

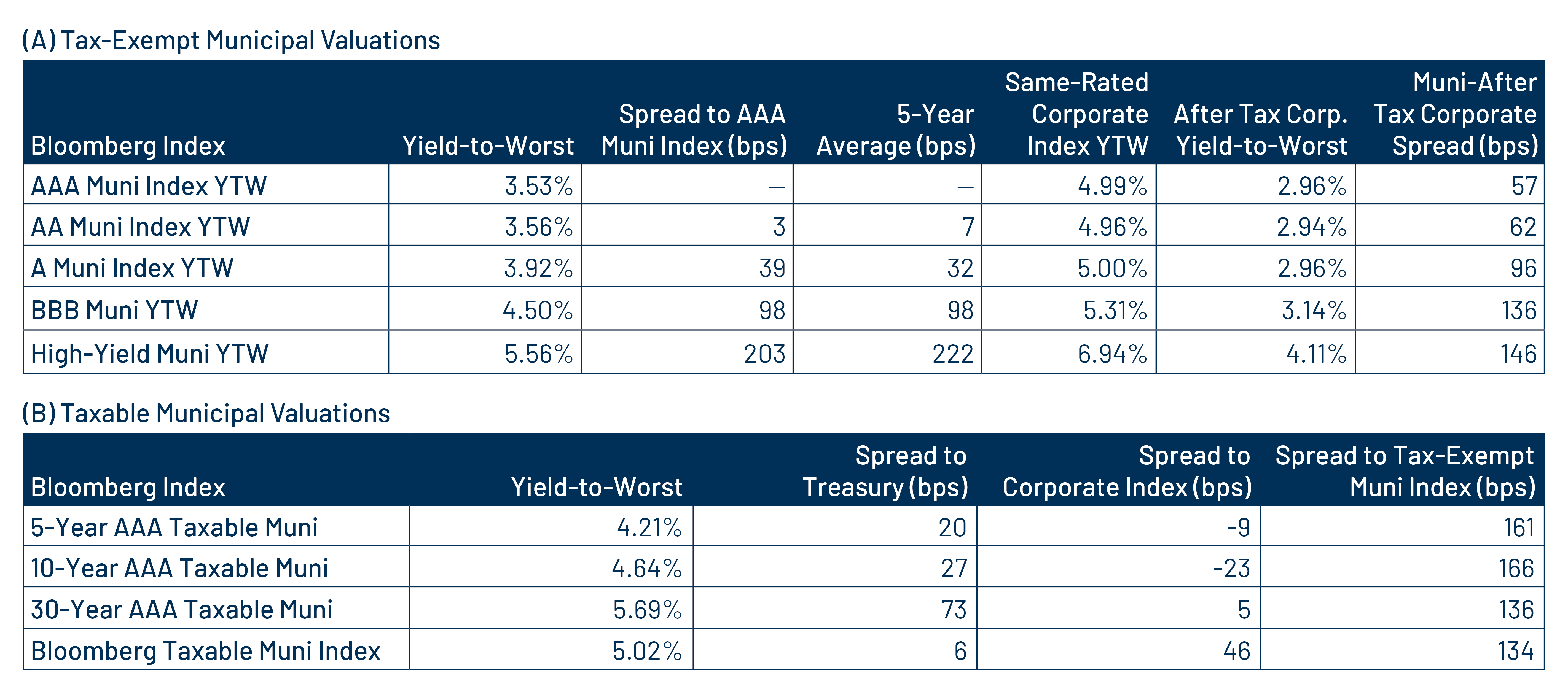

Credit fundamentals continue to demonstrate resilience, though late-cycle characteristics are emerging. Several large issuers are contending with delayed budgets and projecting longer-term budgetary shortfalls. So far this year, the three major rating agencies have downgraded more debt than they have upgraded, by a ratio of 1.3x. In the high-yield segment, some larger issuers have drawn on debt service reserve funds and may pursue restructurings. That said, the broader municipal market continues to benefit from strong revenue collections and elevated cash balances. However, given relatively tight spread levels, Western Asset believes active credit selection remains critical.

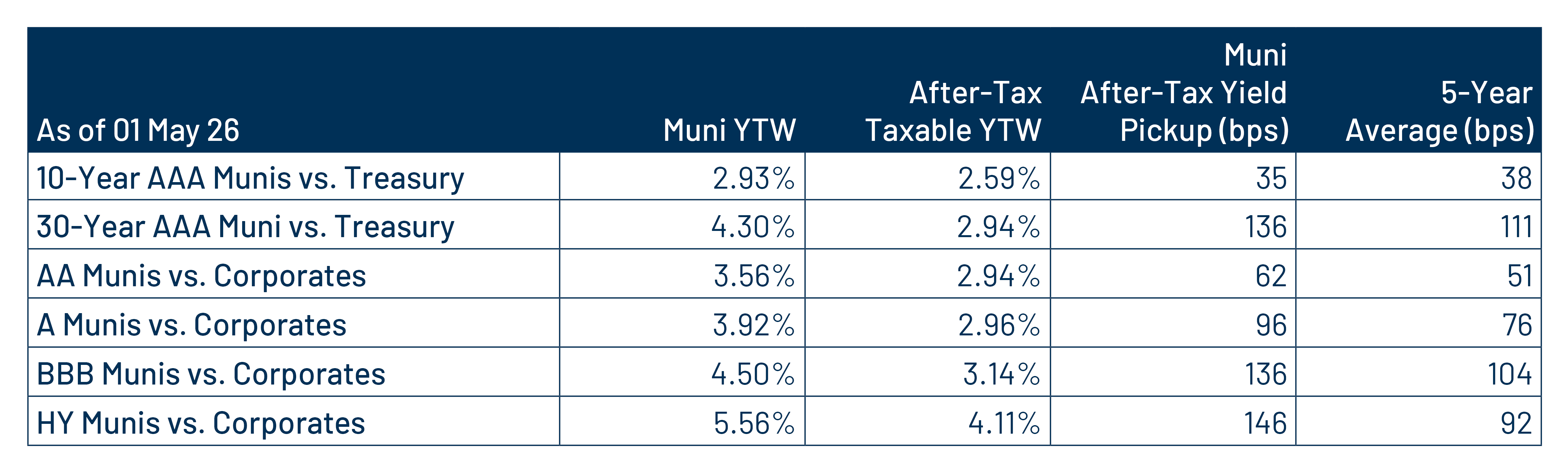

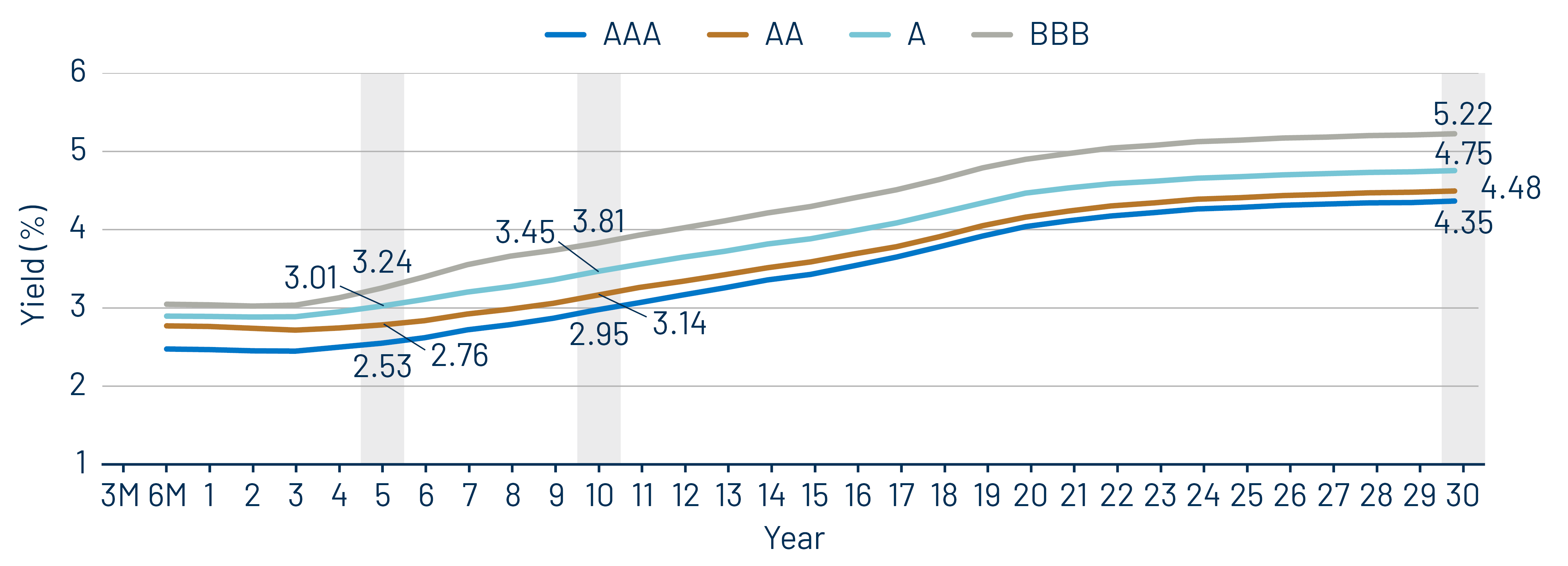

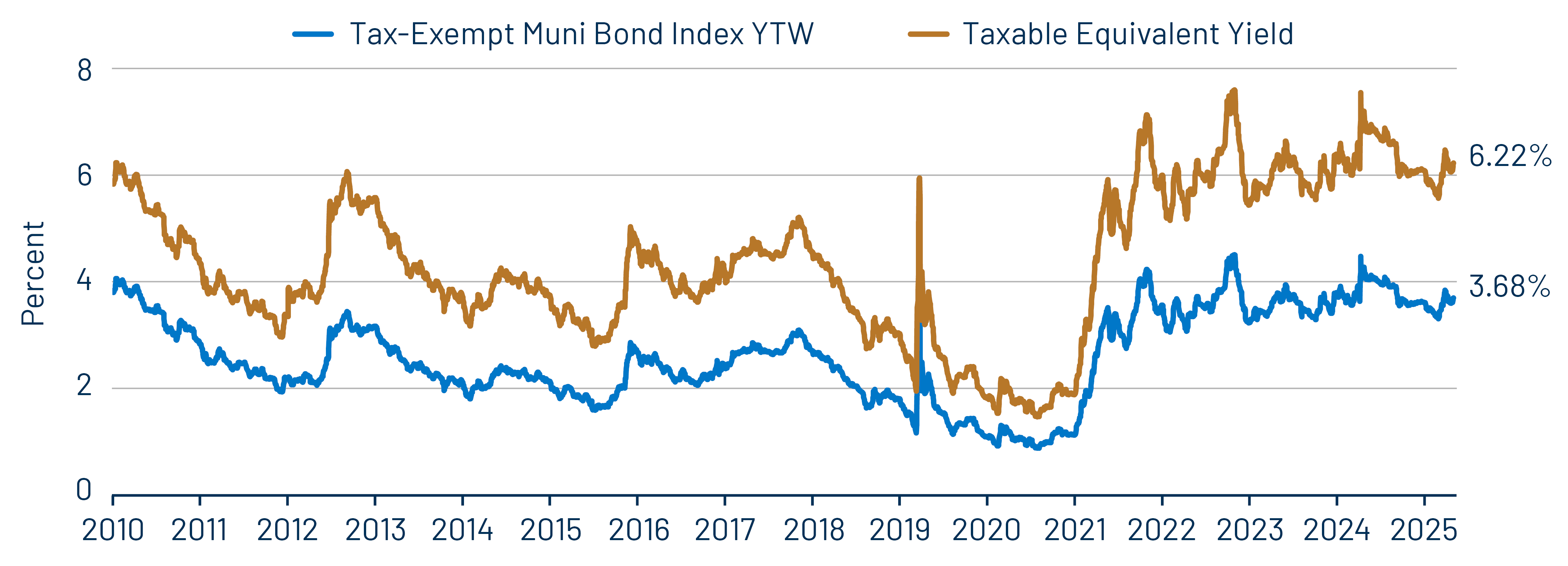

Despite recent outperformance, Western Asset believes the municipal market continues to offer attractive after-tax income opportunities. The Bloomberg Municipal Bond Index yield-to-worst stands at 3.68%, or 6.22% on a taxable-equivalent basis for top federal taxpayers, above historical averages and competitive with lower-rated taxable fixed-income sectors. Income opportunities have improved across much of the curve, with 10-year high-grade yields rising more than 20 bps YTD to approximately 3.0%, and longer maturities increasing by 17 bps to around 4.3%. As seasonal technical headwinds fade, these levels could present an attractive opportunity for muni investors to reposition income and risk exposures in line with overall objectives.

Municipal Credit Curves and Relative Value

Theme 1: Municipal taxable-equivalent yields moved lower from recent highs, but remain above historical averages.

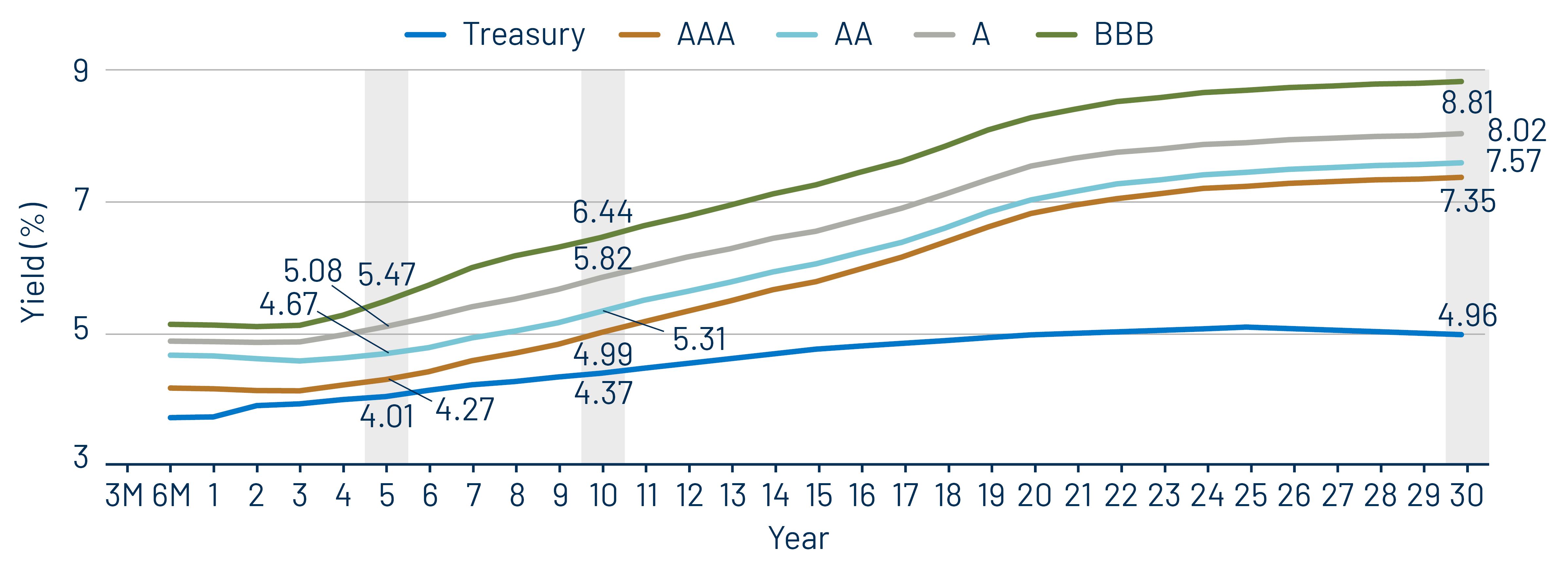

Theme 2: Munis offer attractive after-tax yield pickup vs. longer-duration and lower-quality taxable alternatives.

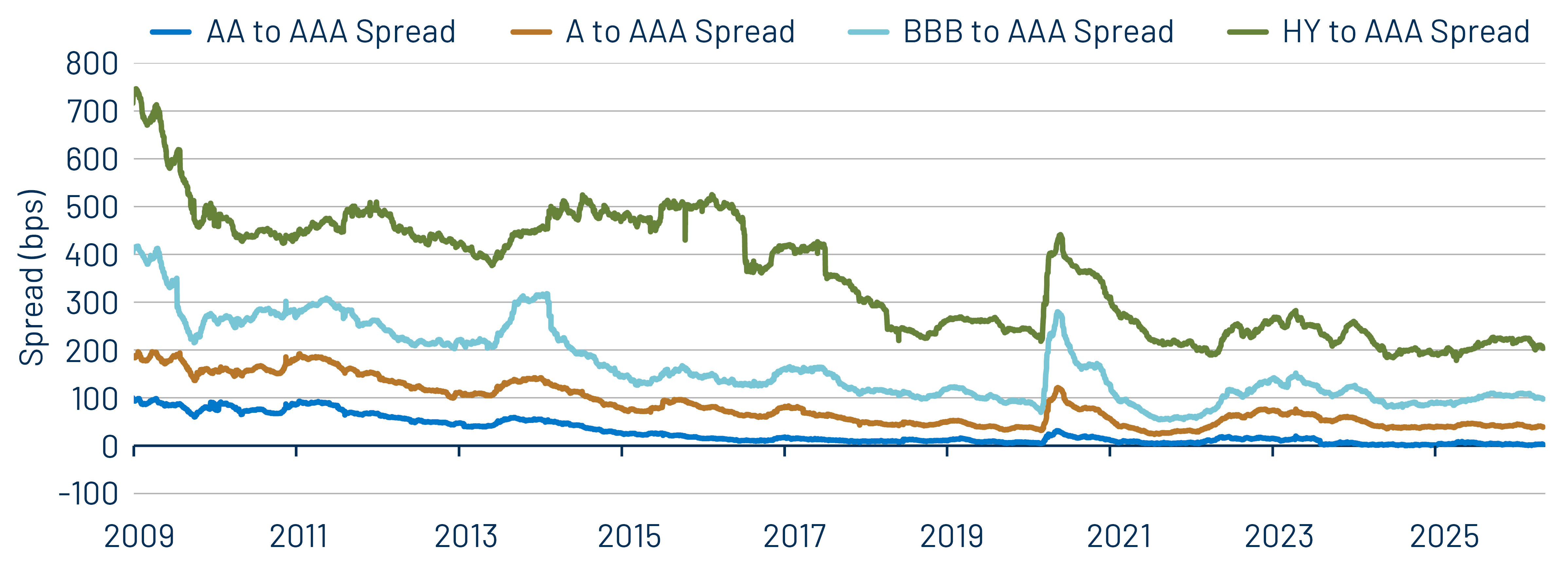

Theme 3: Historically tight municipal credit spreads underscore the importance of credit selection.