Where We Are Now

It was previously announced that all forms of LIBOR would cease to exist at the stroke of midnight on New Year's Eve 2021. However, like many well-intentioned plans in the past 18 months, COVID-19 has now pushed this target date back for some tenors of USD LIBOR to acknowledge that institutions have had their energies distracted by the pandemic. As of this writing, the current dates the various forms of LIBOR will cease publication are as follows:

- EUR, CHF, JPY and GBP LIBOR for all tenors: 12/31/21

- 1-week and 2-month USD LIBOR: 12/31/21

- Overnight, 1-, 3-, 6- and 12-month USD LIBOR: 6/30/23

Looking Back Over the First Half of the Year

Although the transition of some tenors of LIBOR have been kicked down the road, that doesn't mean that considerable progress has not been made by the various entities tasked with the transition planning or by the overall market. Some of the significant milestones reached this year have included:

February 2021

- With a maturity of 10 years, the World Bank issued the longest bond with a coupon linked to SOFR. The $600 million issue was oversubscribed from a variety of investors. The World Bank is now the only issuer among its supranational, sovereign and agency (SSA) peers who can present a liquid SOFR curve from 2 years to 10 years.1

- The Canadian energy firm Enbridge became the world's first non-financial, non-SSA company to issue a SOFR-linked bond, thus expanding the universe of issuer industries. The $500 million, 2-year floating rate bond deal was six times oversubscribed.2

- The trading volume and open interest of SOFR futures reached an all-time high—underscoring the significant growth of SOFR-related derivatives.3

March 2021

- After an RFP process spanning several months by the Alternative Reference Rates Committee (ARRC), the global financial data provider Refinitiv was announced as the official publisher of SOFR spread adjustments. Refinitiv will provide the recommended fixed spreads and spread-adjusted rates for cash products, including floating-rate bonds, that transition away from USD LIBOR to SOFR, as stated in prospectus fallback provisions.4

- The ARRC published guidance on using SOFR in new asset-backed security (ABS) issues including consumer ABS, mortgage-backed securities (MBS), and commercial mortgage-backed securities (CMBS). The model describes how new issuance of ABS products could use historic 30-day average SOFR rates, with a monthly reset, determined in advance of the interest accrual period.5

April 2021

- New York State Governor Andrew Cuomo signed legislation into state law that addressed the issue of tough legacy LIBOR contracts maturing after mid-2023 that do not have effective fallback language. The legislation will be crucial in minimizing legal uncertainty and adverse economic impacts associated with the transition.6

- Although a provider has yet to be chosen for a forward-looking SOFR term rate with the conclusion of an RFP issued by the ARRC, they did publish some very broad principles to help define the rate's broad objectives. The maturities of such a rate would likely match those of the retiring LIBOR (i.e., 1-, 3-, 6-, and 12-month tenors) and its publication is crucial in building liquidity in the SOFR derivatives market.7

Looking Forward

Despite the small additional competition within the money markets from the Bloomberg Short Term Bank Yield Index (BSBY), the overall issuance of SOFR-linked short-term instruments continued to rise. Between January and May 2021, a total of $26.6 billion of debt was issued with maturities under 12 months which is sizable when compared to the $15.1 billion issued during the whole of 2020.

Similarly, the overall debt market for SOFR-linked bonds of any maturity also saw considerable growth. In the first five months of 2021, the total par amount of issuance outstanding grew by 16.3% to end May 31, 2021 at $1.0 trillion. These upward trends are expected to continue throughout the rest of the year as we approach the first cessation date at year-end.8

For the bank loan and CLO market, newer issuance now includes robust fallback language. For the older securities that have no fallback language, the expectation is that they will be called. There are limited concerns for any of the LIBOR-linked securities reaching the LIBOR end date without some type of switch to an acceptable alternative rate. Borrowers in this market are unlikely to transition until a deadline is imminent and ARRC will be instrumental in messaging to the market and borrowers about which SOFR benchmark to utilize.

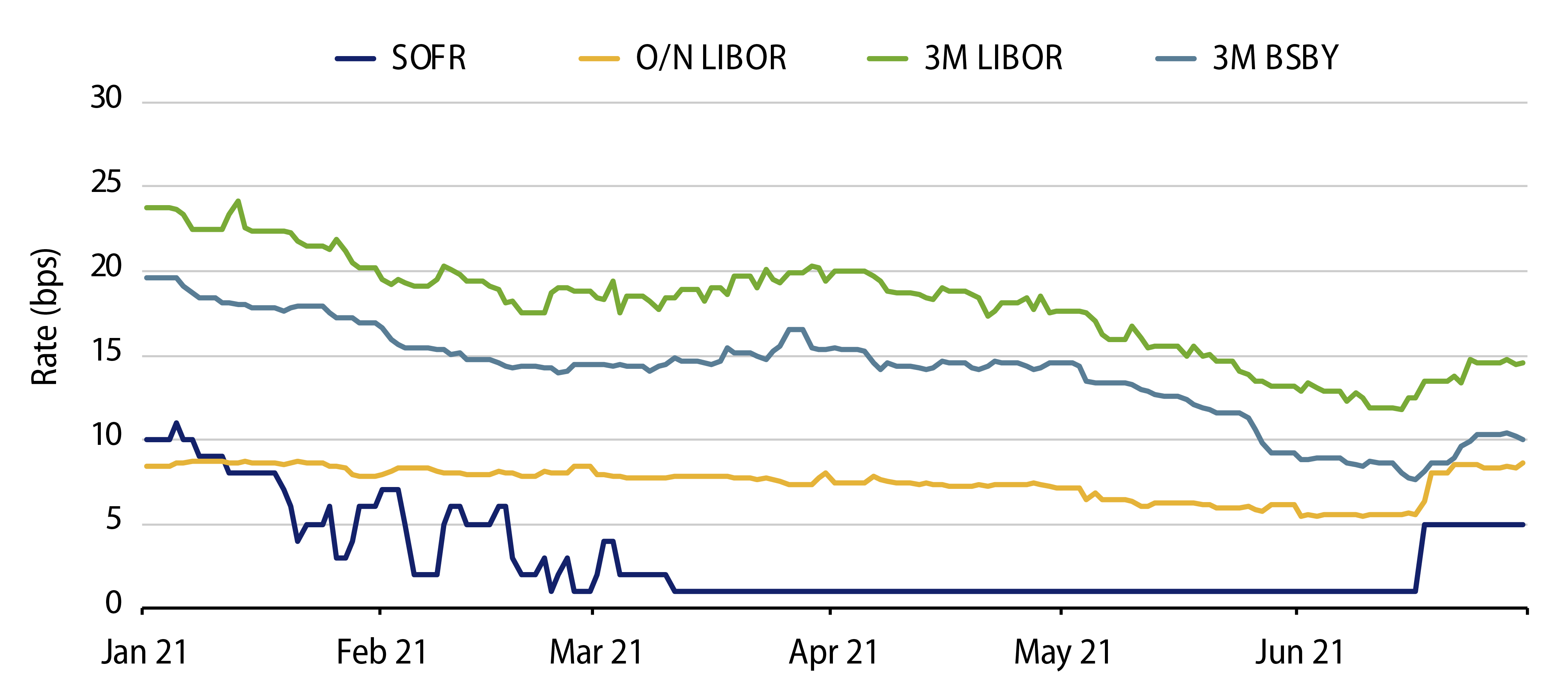

Regarding LIBOR swaps, trading volume has continued to be high but is expected to decrease in the coming months. The Market Risk Advisory Committee of the Commodity Futures Trading Commission (CFTC) is directing inter-broker dealers to stop their current behavior of quoting and trading SOFR as a spread to LIBOR and instead trade LIBOR swaps as a spread to SOFR. This reversal of market convention has been called SOFR First with the intention of making SOFR the primary rate quoted by dealers. If successful, SOFR will become the primary base rate for LIBOR swaps. This should lead to an increase in SOFR liquidity and a corresponding decrease in LIBOR liquidity.

Our Approach

At Western Asset, we continue to believe that regulators, market makers, issuers and benchmark providers are in the best position to implement the market's conversion to new reference rates. Our LIBOR Transition Working Group is actively engaged with counterparties and industry groups to understand and participate in market-wide efforts to address the transition. For impacted securities currently held in our clients' portfolios, we have additionally leveraged an external data source to review the fallback language data to supplement this effort, including key data points such as fallback triggers, fallback types, designated parties and alternate benchmarks.

Operationally, as a fixed-income asset manager, Western Asset is already accustomed to dealing with many different interest rate sources, so the movement away from LIBOR does not pose a challenge to our key systems. We have essentially completed our arrangements to support any new reference indices and we are not actively reducing our LIBOR exposures at this time.

ENDNOTES

1 https://www.worldbank.org/en/news/press-release/2021/02/04/in-milestone-for-sofr-market-world-bank-prices-longest-floating-rate-benchmark

2 https://www.sec.gov/Archives/edgar/data/880285/000110465921024859/tm216594d1_424b2.htm

3 https://www.cmegroup.com/media-room/press-releases/2021/2/26/cme_group_announcesrecordsofrfuturestradingvolumeandopeninterest.html

4 https://www.newyorkfed.org/medialibrary/Microsites/arrc/files/2021/20210317-press-release-Spread-Adjustment-Vendor-Refinitiv.pdf

5 https://www.newyorkfed.org/medialibrary/Microsites/arrc/files/2021/20210326-arrc-press-release-sofr-in-new-abs-products

6 https://www.newyorkfed.org/medialibrary/Microsites/arrc/files/2021/20210407-arrc-press-release-nys-legislation

7 https://www.newyorkfed.org/medialibrary/Microsites/arrc/files/2021/20210420-arrc-press-release-term-rate

8 https://www.cmegroup.com/trading/interest-rates/secured-overnight-financing-rate-futures.html