KEY TAKEAWAYS

- Current high interest rates of over 5% are too restrictive, and a moderation in consumer spending will likely lead to the Fed cutting rates, though markets may move faster.

- Global inflation continues on a bumpy descent, providing flexibility for appropriate central bank policy easing amid slowing growth.

- Fundamentals and default risk support investment-grade credit quality, though valuations are somewhat tight historically outside of the post-GFC period.

- We continue to be constructive on the short and intermediate areas of both investment-grade and higher quality high-yield.

- Our base case remains that this continuation of widespread improvement in almost all fixed-income sectors since October should continue.

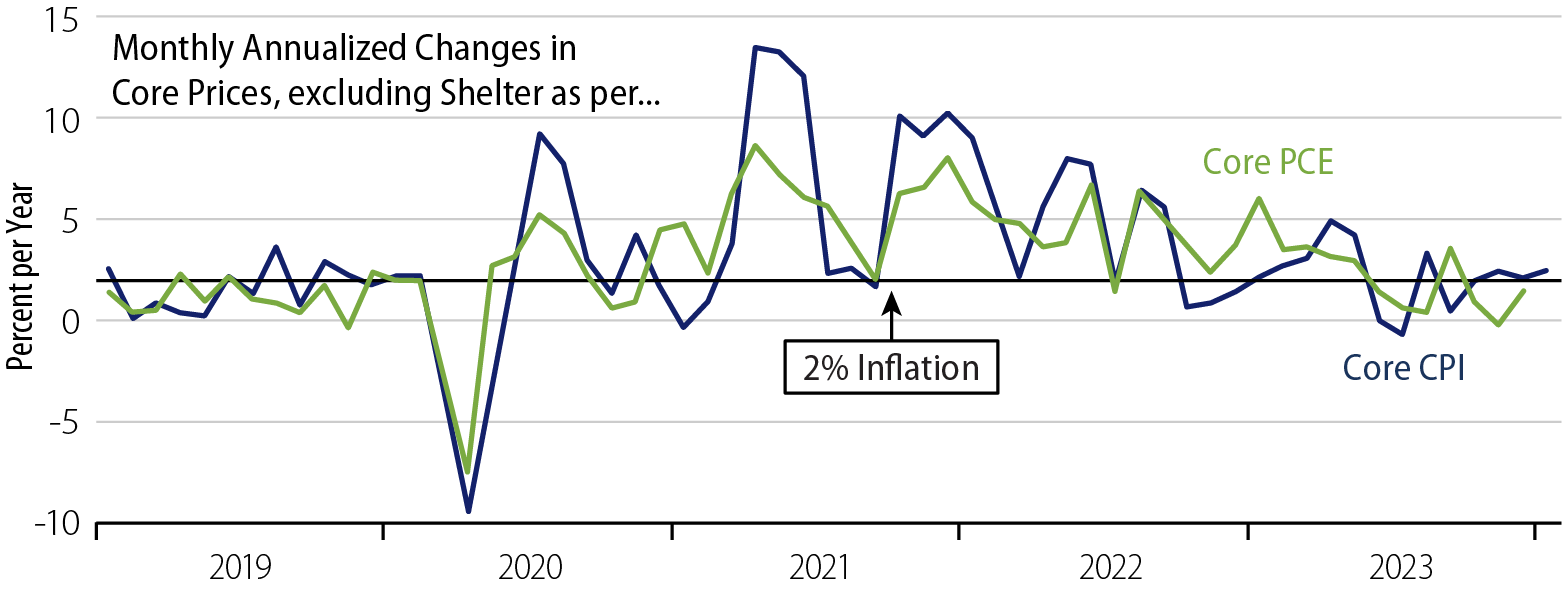

It hasn’t taken the bond market long to re-embrace the “inflation is sticky” theme, as Treasury bonds have sold off from their year-end prices. The spectacular 4Q23 Treasury rally was the largest on record. Treasury bonds rebounded as the then-prevailing narrative of perpetually higher-than-target (sticky) inflation and permanently elevated real rates changed swiftly. The inflation rate has since moved sharply lower to the 2% level on a six- and, by some measures, a nine-month basis. Federal Reserve (Fed) Chair Jerome Powell and other Federal Open Market Committee (FOMC) members have now voiced that the path to cutting interest rates from currently restrictive levels will depend only on more “confirming” evidence (Exhibit 1).

Our view has been that the inflation rate would recede to Fed target levels without the necessity of inducing a recession. We continue to maintain that the path and timing of Fed rate cuts will depend primarily on the strength of the US economy, as the Fed is desirous to wait as long as possible. Recent economic resiliency has caused market reassessment of the timing of rate cuts. But the more important point, we believe, is that short rates of 5% or more are simply too high. Fortunately, the economy has been able to hold up, but we strongly suspect that restrictive rates, tighter credit conditions and, most importantly, a retrenchment from elevated consumer spending will bring a moderation in US growth. This will set the stage for the Fed to cut rates. The bond market may or may not wait for that eventuality. The current elevated level of interest rates suggests that investors should be willing to capture today’s longer-term Treasury yields. This is the reason the Treasury yield curve continues its multi-year period of being inverted.

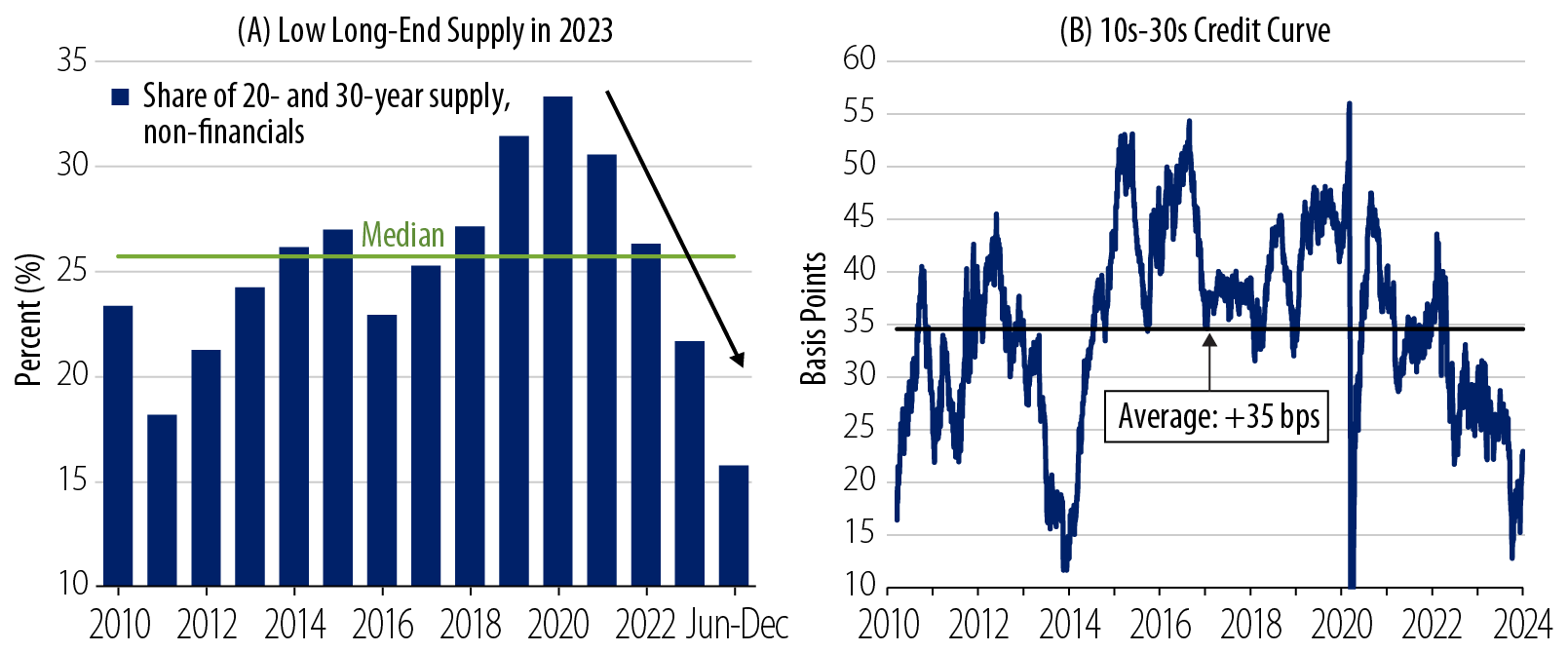

The long investment-grade sector stands out as one where investors have been more than willing to lock in today’s elevated yields at the same time issuers have pulled back from borrowing. This relative dearth of supply amid ongoing investor demand has made this one of the best-performing bond sectors over the last year (Exhibit 2).

One of the anomalies of this market has been the avalanche of interest in private credit, even as most surveys show investor caution about public credit valuations. The backdrop for all credit is one of cash flow fundamentals and pricing relative to default risk. For investment-grade issuers, default risk has been historically very low. Current cash flow and debt metrics remain supportive. Margins have contracted, but from historic all-time highs. Which brings us to valuations. Currently they are tight by the standards of the post-GFC period. But we would point to the uniquely strong fundamentals, “locked-in” lower interest rates of investment-grade company balance sheets and the perspective of longer historical time frames (that weren’t subject to the deflationary risks of the dozen years before Covid), which all suggest today’s yield spreads are fair.

We have become cautious on long credit, specifically, as it has outraced so many other credit sectors. But we remain constructive on the short and intermediate areas of both investment-grade and higher quality high-yield. Investors are struggling to find yields exceeding the Fed’s 5%+ overnight rate. Given the prospect of only grudging interest-rate declines, this is a key consideration. Current economic resiliency is supportive, and over time, the Fed has the ability to provide interest-rate relief should the economy struggle. Still, in a sharper economic slowdown, maintaining credit exposure in shorter rather than longer duration spread product should prove relatively beneficial. And in such an environment, long Treasury duration would prove very helpful.

On the global front, we are constructive on many emerging markets (EM), both in USD-denominated and local currency. On the latter, this year has the potential to be a watershed. EM countries have been ahead of developed market (DM) countries in terms of their policy-tightening the last two years. They are now in the position to be able to cut rates. This should be combined with reasonably stable currencies, and in that event, total returns could be significant.

While there is much talk of de-globalization (the withdraw of DM countries’ manufacturing processes from EM countries), we think a reconfiguration is a better description. Supply chains are being rerouted to countries that are seen as very unlikely to be geopolitical adversaries. India, for example, has benefited versus China. Closer to home, Mexico has been perhaps the primary beneficiary, and we believe this trend will continue.

Global growth has shifted down, and global inflation continues to recede. Indeed, China is actually in deflation. The challenge for central bankers will be adjusting interest rates downward in an appropriately timely manner. Currently, US growth is the best in the field, giving the Fed leeway to wait. But as the trends of declining inflation (as uneven as it is) and moderating growth become more pronounced, the Fed is likely to respond. Our base case remains that this continuation of widespread improvement in almost all fixed-income sectors since October should continue.