KEY TAKEAWAYS

- With inflation headed lower, the high real interest rates brought on largely by fiscal stimulus seem unlikely to persist.

- A less resilient consumer and easing labor market point to broad economic softening ahead that will likely necessitate Fed rate cuts in time.

- Between demographic changes, advancing technology and debt constraints, arguments for permanently high real US rates may recede.

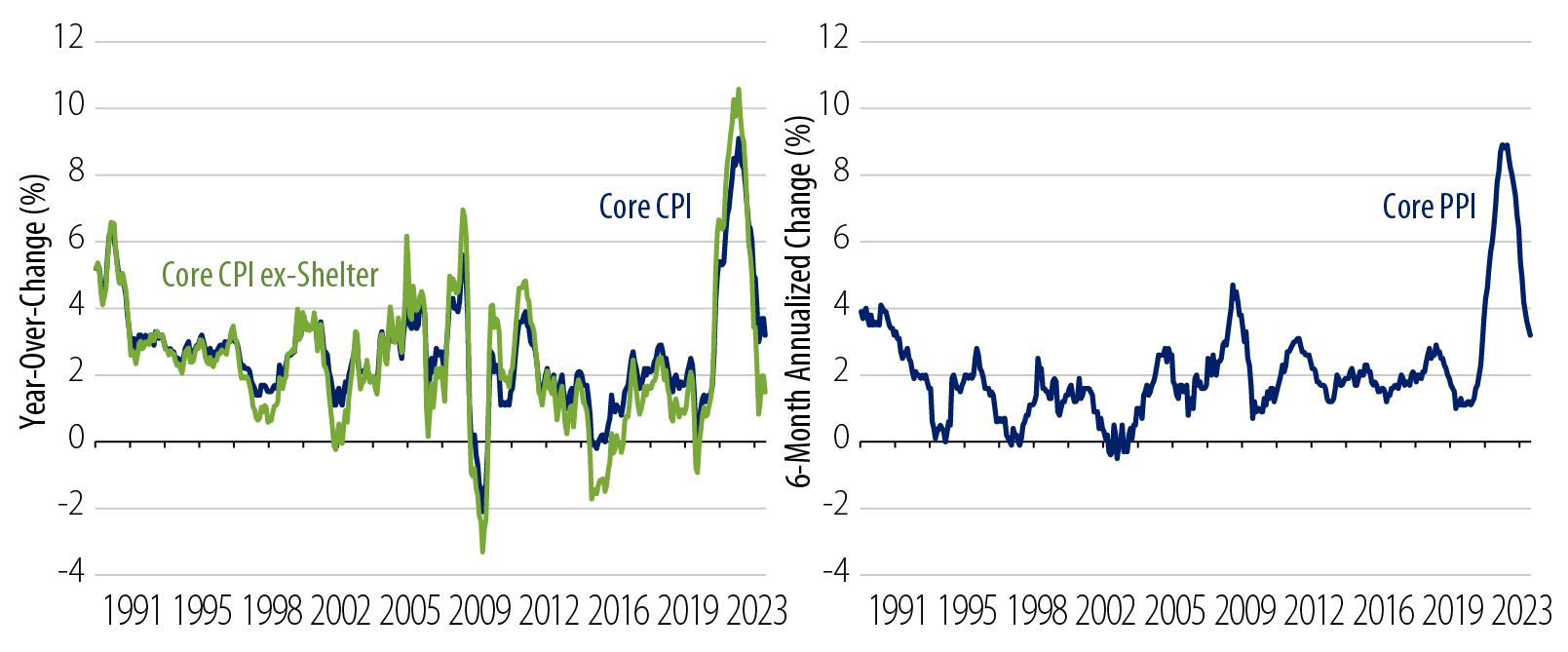

There is an old adage in the investment business that being early and being wrong is a distinction without a difference. It has been a long and brutal tightening campaign by the Federal Reserve (Fed) in its quest to head off accelerating inflation. Finally, it appears highly probable the tightening cycle has come to an end as inflation continues on its uneven but decisively downward path. Exhibit 1 shows the Consumer Price Index (CPI) less shelter and the Producer Price Index (PPI). The most distinguishing feature is the sharp downward trajectory of both. Absent shelter costs, the CPI has been under the Fed’s 2% target for the last six months. The six-month annualized rate of change of the overall Producer Price Index (PPI) is running at 2.2%. Additionally, the PPI now stands at less than 2% above its June 2022 level.

Monetary policy is tight. In addition to the sharp deceleration in price indices, real rates are high across the yield curve. The five-year Treasury Inflation-Protected Securities (TIPS) rate at 2.25% is more than double the 25-year average of just over 1%. The Treasury curve remains inverted. Money supply has contracted year over year and lending standards have tightened sharply over the course of this year.

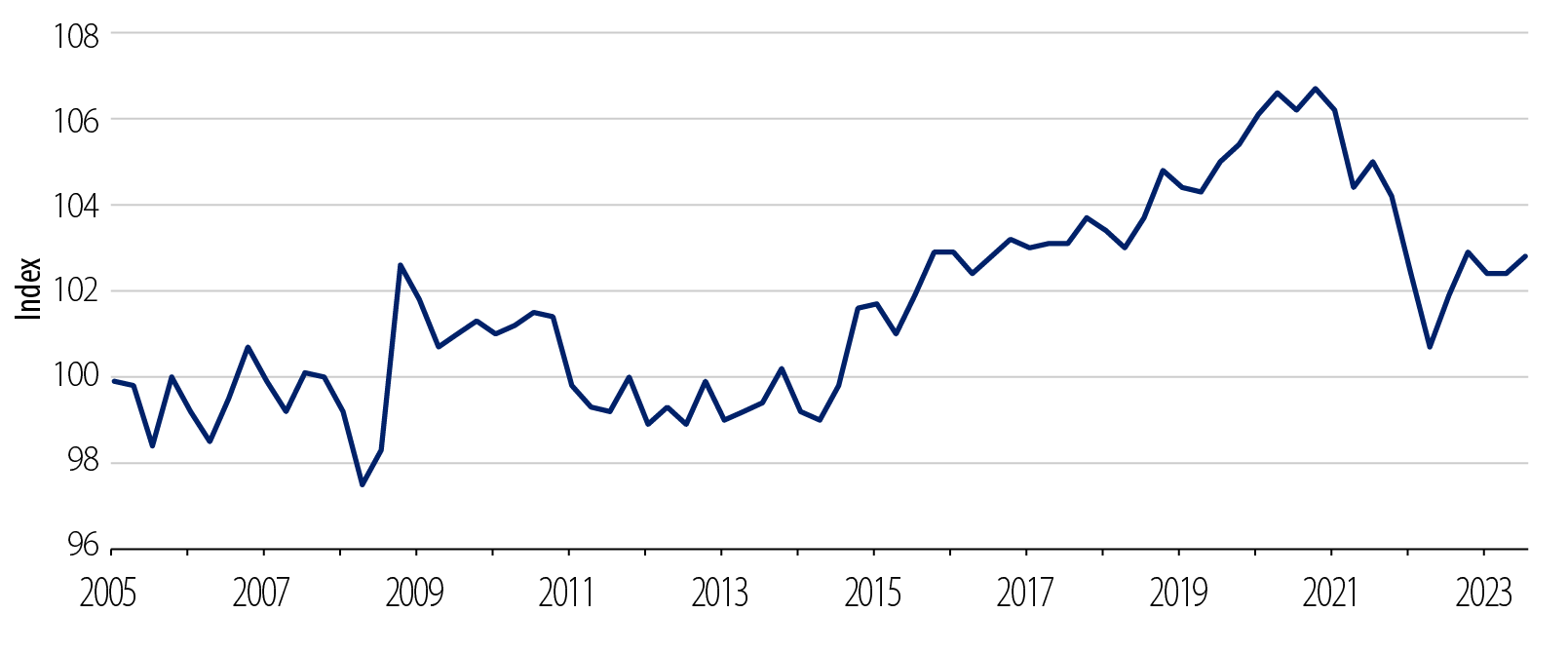

The US economy, though, has held up remarkably well. The consumer has been surprisingly resilient despite historically low savings rates and declining real income (Exhibit 2). The labor market looks to be finally easing, albeit from very tight levels. This has so far kept the bond market from rallying sharply, which is the historical pattern usually seen after the Fed stops a tightening campaign. But our view is that it won’t take much of a waning in economic or consumer resilience to restart the bond rally. Indeed, the last two weeks suggest the bond market might already be engaged in that process.

The Fed has argued forcefully that it will keep rates higher for longer. There is debate not only about economic resilience, but of the “stickiness” of inflation as we approach the Fed’s goal. Additionally, as both the federal deficit and Treasury supply have increased, many have voiced concerns of more permanent high real rates, arguing for containing any upcoming Treasury yield decline. The Fed clearly wishes to defer any rate cuts until it has as high a degree of certainty as it can afford that inflation is down for the count.

The persistence or lack of economic strength will dictate the timing of the Fed’s rate cutting path. But markets are forward looking. Historically, the Fed has waited too long before cutting rates. And if the Fed repeats that pattern, it then would have to cut further than if it started sooner. This is where economic fear may start to build. Our view is that the improvement in inflation trends may give the Fed the flexibility to deliver cuts without undue economic hardship. The risk case, though, remains that the Fed waits too long. In either scenario, an overweight duration is needed.

We might also push back on many of the recent arguments in favor of the permanence in high real rates. We think the economic resilience of the US economy, aided by fiscal stimulus, helps explain the loftiness of US rates. Yes, there are great fiscal challenges facing countries, but there are also countervailing political needs to restrain deficits. The long-term debt-to-GDP headwind is more firmly in place than ever. Despite currently tight labor markets, demographics will remain a growth headwind. Technology, especially with the accelerating use of AI, should remain a powerful disinflationary force. And behind the scenes, longevity will provide an ongoing source of demand for high-quality fixed-income. Ultimately, though, the R-star debate is somewhat of a coffee house issue discussion. The key will ultimately be growth. If growth can reach levels significantly above those of the last 25 years, then the arguments for higher real rates may yet have their day. But if, as most private and public forecasters expect, growth returns to the global 3.5% and US 2% trends to which we have become accustomed, then these arguments may wane. And if anemic growth turns down under the weight of declining inflation and undue Fed tightening, then the old lower-for-longer R-star argument may just get revisited.

Our view continues to be that global and US inflation remain in an ongoing if uneven downtrend. Global growth is slowing. Despite the current US growth resilience, slower growth is coming. Our base case is that the slowdown can be accomplished in a beneficial way for all financial assets as the Fed eases policy to normalize real short rates. If we are wrong, our most likely risk case is that rates will need to fall further faster to contain the slowdown.