Market Commentary

The only investors who shouldn’t diversify are those who are right 100% of the time. ~John Templeton

Executive Summary

- In the last two years, market sentiment has swung from pessimistic “secular stagnation” to today’s “reflation trade” enthusiasm.

- As optimists, we have focused on investing in the higher-yielding spread sectors that benefit from improving economic fundamentals, and we believe EM debt continues to provide the greatest opportunity.

- Our core theme has been that the process of inflation and interest-rate normalization would be very slow to develop, which is counter to the current market consensus expectation of higher inflation.

- Despite market optimism about accelerating growth, the need to protect against unpleasant surprises remains a crucial portfolio priority.

- If our outlook proves broadly correct, spread sectors and EM particularly should do well; if there are any setbacks, Treasury bond gains should help provide a cushion.

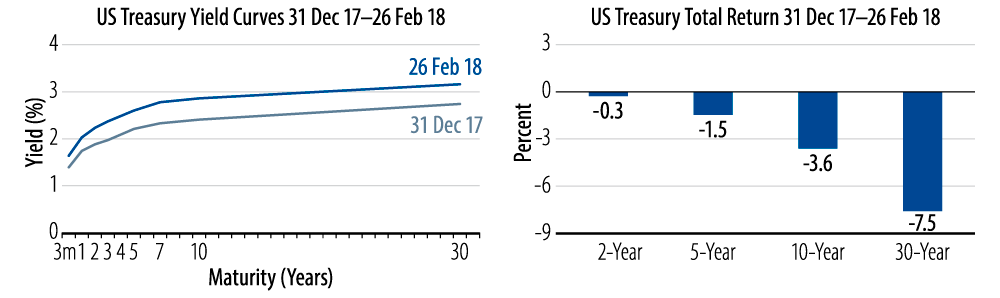

A little under two years ago the market and academic financial commentary were focusing on “secular stagnation.” This was the idea that global growth and inflation were so constrained by secular forces that policymakers and investors should focus on the need to protect against the persistence of downside risks to growth. Today, the ebullient market is celebrating the “reflation trade”—a synchronized global recovery buttressed with super-charged US fiscal policy that must mean risks to growth and inflation are only to the upside.

As optimists about the global and US recoveries over the course of the expansion, we have focused on investing in the higher-yielding spread sectors that benefit from improving economic fundamentals. This year the challenge to such an approach is that yield spreads are narrower than at any other time previously in this expansion. That reduces the margin for error and our overweights in developed country spread sectors have been substantively reduced. The area of greatest opportunity, in our view, is emerging market (EM) debt, particularly local-currency-denominated debt. Here, yield spreads are historically attractive at a time when global growth fundamentals have reversed from the headwinds of prior years into a powerful tailwind.

Both the good and bad news about portfolios utilizing diversified strategies is that some can be winning while others can be losing. That is the hallmark of our diversified strategy philosophy—not all of our risks are aligned or pointing in the same direction. The key to success is not only hopefully to have more winners than losers, but also to set the proportions such that the money won on the winners is more than the money lost on the losers. As if establishing a majority of strategies on the plus side isn’t hard enough, trying to gauge the aforementioned proportions is every bit as difficult. Relative volatilities change dramatically in different market environments. What might have seemed a modest-sized position can turn into a meaningful winner or loser if the volatility erupts dramatically.

This year is a particularly good one for an example of this kind. Volatility across all asset classes was subdued for almost all of last year, only to jump sharply in February. Now, most everyone appreciated that volatility was historically, perhaps unnaturally, low. So in building portfolios, not only was your assessment of the economic and financial environment central to your sizing decision, using more normal volatilities as the basis for your decision was also important.

Exhibit 1 displays the performance of a wide variety of spread sectors relative to Treasury or sovereign bonds (excess returns). Our concentration in spread sectors proved favorable as virtually all sectors performed positively. Most notably, the performance of local currency EM was truly outsized, providing at least an early-year validation of our positioning.

Spread Sectors Excess Returns (Year-to-Date Ending 26 Feb 18)

A little under two years ago the market and academic financial commentary were focusing on “secular stagnation.” This was the idea that global growth and inflation were so constrained by secular forces that policymakers and investors should focus on the need to protect against the persistence of downside risks to growth. Today, the ebullient market is celebrating the “reflation trade”—a synchronized global recovery buttressed with super-charged US fiscal policy that must mean risks to growth and inflation are only to the upside.

As optimists about the global and US recoveries over the course of the expansion, we have focused on investing in the higher-yielding spread sectors that benefit from improving economic fundamentals. This year the challenge to such an approach is that yield spreads are narrower than at any other time previously in this expansion. That reduces the margin for error and our overweights in developed country spread sectors have been substantively reduced. The area of greatest opportunity, in our view, is emerging market (EM) debt, particularly local-currency-denominated debt. Here, yield spreads are historically attractive at a time when global growth fundamentals have reversed from the headwinds of prior years into a powerful tailwind.

Both the good and bad news about portfolios utilizing diversified strategies is that some can be winning while others can be losing. That is the hallmark of our diversified strategy philosophy—not all of our risks are aligned or pointing in the same direction. The key to success is not only hopefully to have more winners than losers, but also to set the proportions such that the money won on the winners is more than the money lost on the losers. As if establishing a majority of strategies on the plus side isn’t hard enough, trying to gauge the aforementioned proportions is every bit as difficult. Relative volatilities change dramatically in different market environments. What might have seemed a modest-sized position can turn into a meaningful winner or loser if the volatility erupts dramatically.

This year is a particularly good one for an example of this kind. Volatility across all asset classes was subdued for almost all of last year, only to jump sharply in February. Now, most everyone appreciated that volatility was historically, perhaps unnaturally, low. So in building portfolios, not only was your assessment of the economic and financial environment central to your sizing decision, using more normal volatilities as the basis for your decision was also important.

Exhibit 1 displays the performance of a wide variety of spread sectors relative to Treasury or sovereign bonds (excess returns). Our concentration in spread sectors proved favorable as virtually all sectors performed positively. Most notably, the performance of local currency EM was truly outsized, providing at least an early-year validation of our positioning.

A little under two years ago the market and academic financial commentary were focusing on “secular stagnation.” This was the idea that global growth and inflation were so constrained by secular forces that policymakers and investors should focus on the need to protect against the persistence of downside risks to growth. Today, the ebullient market is celebrating the “reflation trade”—a synchronized global recovery buttressed with super-charged US fiscal policy that must mean risks to growth and inflation are only to the upside.

As optimists about the global and US recoveries over the course of the expansion, we have focused on investing in the higher-yielding spread sectors that benefit from improving economic fundamentals. This year the challenge to such an approach is that yield spreads are narrower than at any other time previously in this expansion. That reduces the margin for error and our overweights in developed country spread sectors have been substantively reduced. The area of greatest opportunity, in our view, is emerging market (EM) debt, particularly local-currency-denominated debt. Here, yield spreads are historically attractive at a time when global growth fundamentals have reversed from the headwinds of prior years into a powerful tailwind.

Both the good and bad news about portfolios utilizing diversified strategies is that some can be winning while others can be losing. That is the hallmark of our diversified strategy philosophy—not all of our risks are aligned or pointing in the same direction. The key to success is not only hopefully to have more winners than losers, but also to set the proportions such that the money won on the winners is more than the money lost on the losers. As if establishing a majority of strategies on the plus side isn’t hard enough, trying to gauge the aforementioned proportions is every bit as difficult. Relative volatilities change dramatically in different market environments. What might have seemed a modest-sized position can turn into a meaningful winner or loser if the volatility erupts dramatically.

This year is a particularly good one for an example of this kind. Volatility across all asset classes was subdued for almost all of last year, only to jump sharply in February. Now, most everyone appreciated that volatility was historically, perhaps unnaturally, low. So in building portfolios, not only was your assessment of the economic and financial environment central to your sizing decision, using more normal volatilities as the basis for your decision was also important.

Exhibit 1 displays the performance of a wide variety of spread sectors relative to Treasury or sovereign bonds (excess returns). Our concentration in spread sectors proved favorable as virtually all sectors performed positively. Most notably, the performance of local currency EM was truly outsized, providing at least an early-year validation of our positioning.

Q: “And, more broadly, what have you left undone?”

Yellen: “What’s on my ‘undone’ list, you ask? We have a 2% symmetric inflation objective, and, for a number of years now, inflation has been running under 2%...”

“...but I have tried to be straightforward in saying that this could end up being something that is more ingrained and turns out to be permanent.”

A little under two years ago the market and academic financial commentary were focusing on “secular stagnation.” This was the idea that global growth and inflation were so constrained by secular forces that policymakers and investors should focus on the need to protect against the persistence of downside risks to growth. Today, the ebullient market is celebrating the “reflation trade”—a synchronized global recovery buttressed with super-charged US fiscal policy that must mean risks to growth and inflation are only to the upside.

As optimists about the global and US recoveries over the course of the expansion, we have focused on investing in the higher-yielding spread sectors that benefit from improving economic fundamentals. This year the challenge to such an approach is that yield spreads are narrower than at any other time previously in this expansion. That reduces the margin for error and our overweights in developed country spread sectors have been substantively reduced. The area of greatest opportunity, in our view, is emerging market (EM) debt, particularly local-currency-denominated debt. Here, yield spreads are historically attractive at a time when global growth fundamentals have reversed from the headwinds of prior years into a powerful tailwind.

Both the good and bad news about portfolios utilizing diversified strategies is that some can be winning while others can be losing. That is the hallmark of our diversified strategy philosophy—not all of our risks are aligned or pointing in the same direction. The key to success is not only hopefully to have more winners than losers, but also to set the proportions such that the money won on the winners is more than the money lost on the losers. As if establishing a majority of strategies on the plus side isn’t hard enough, trying to gauge the aforementioned proportions is every bit as difficult. Relative volatilities change dramatically in different market environments. What might have seemed a modest-sized position can turn into a meaningful winner or loser if the volatility erupts dramatically.

This year is a particularly good one for an example of this kind. Volatility across all asset classes was subdued for almost all of last year, only to jump sharply in February. Now, most everyone appreciated that volatility was historically, perhaps unnaturally, low. So in building portfolios, not only was your assessment of the economic and financial environment central to your sizing decision, using more normal volatilities as the basis for your decision was also important.

Exhibit 1 displays the performance of a wide variety of spread sectors relative to Treasury or sovereign bonds (excess returns). Our concentration in spread sectors proved favorable as virtually all sectors performed positively. Most notably, the performance of local currency EM was truly outsized, providing at least an early-year validation of our positioning.

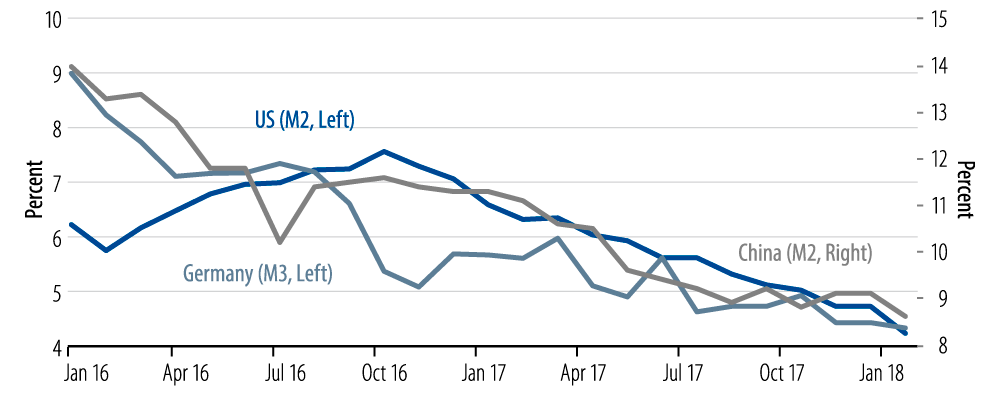

Money Supply Growth Decelerating

A little under two years ago the market and academic financial commentary were focusing on “secular stagnation.” This was the idea that global growth and inflation were so constrained by secular forces that policymakers and investors should focus on the need to protect against the persistence of downside risks to growth. Today, the ebullient market is celebrating the “reflation trade”—a synchronized global recovery buttressed with super-charged US fiscal policy that must mean risks to growth and inflation are only to the upside.

As optimists about the global and US recoveries over the course of the expansion, we have focused on investing in the higher-yielding spread sectors that benefit from improving economic fundamentals. This year the challenge to such an approach is that yield spreads are narrower than at any other time previously in this expansion. That reduces the margin for error and our overweights in developed country spread sectors have been substantively reduced. The area of greatest opportunity, in our view, is emerging market (EM) debt, particularly local-currency-denominated debt. Here, yield spreads are historically attractive at a time when global growth fundamentals have reversed from the headwinds of prior years into a powerful tailwind.

Both the good and bad news about portfolios utilizing diversified strategies is that some can be winning while others can be losing. That is the hallmark of our diversified strategy philosophy—not all of our risks are aligned or pointing in the same direction. The key to success is not only hopefully to have more winners than losers, but also to set the proportions such that the money won on the winners is more than the money lost on the losers. As if establishing a majority of strategies on the plus side isn’t hard enough, trying to gauge the aforementioned proportions is every bit as difficult. Relative volatilities change dramatically in different market environments. What might have seemed a modest-sized position can turn into a meaningful winner or loser if the volatility erupts dramatically.

This year is a particularly good one for an example of this kind. Volatility across all asset classes was subdued for almost all of last year, only to jump sharply in February. Now, most everyone appreciated that volatility was historically, perhaps unnaturally, low. So in building portfolios, not only was your assessment of the economic and financial environment central to your sizing decision, using more normal volatilities as the basis for your decision was also important.

Exhibit 1 displays the performance of a wide variety of spread sectors relative to Treasury or sovereign bonds (excess returns). Our concentration in spread sectors proved favorable as virtually all sectors performed positively. Most notably, the performance of local currency EM was truly outsized, providing at least an early-year validation of our positioning.