Macros, Markets and Munis

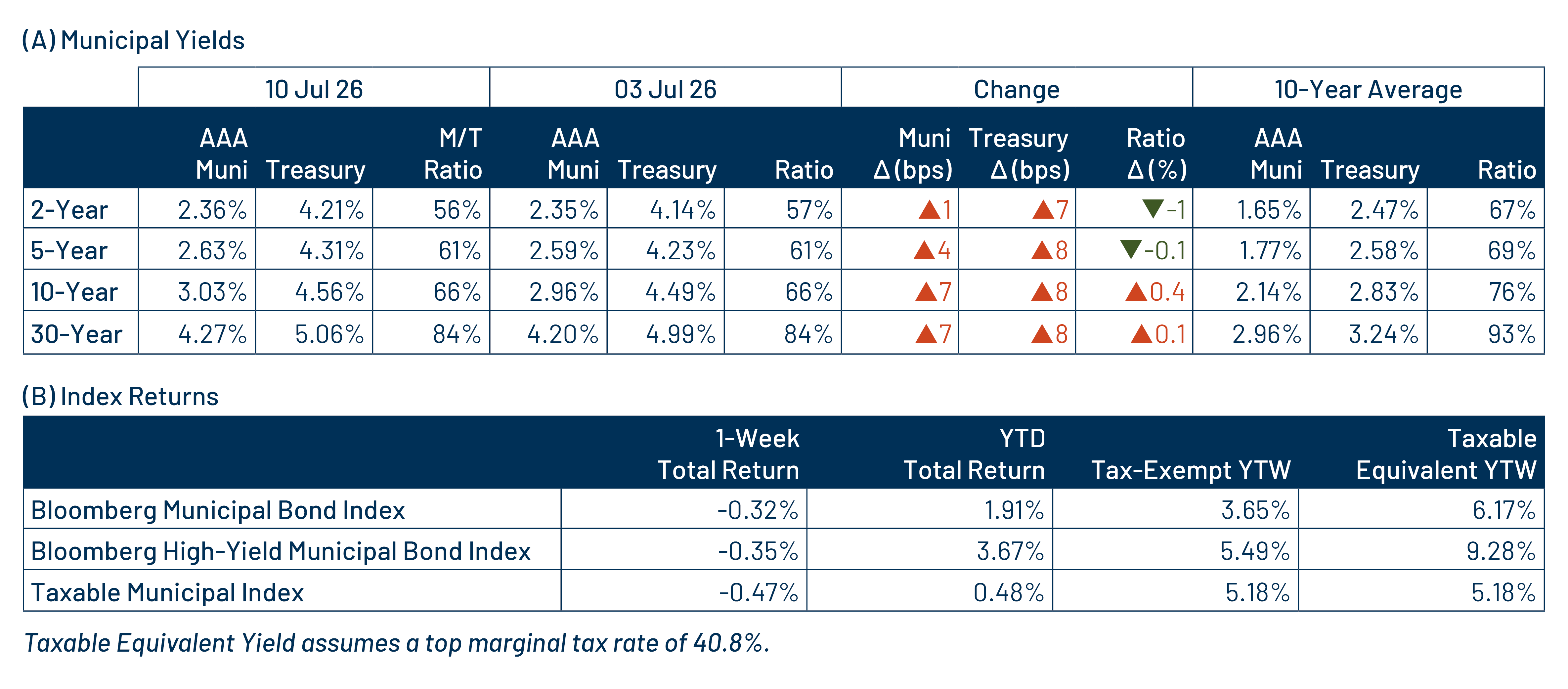

Municipals posted negative returns last week but outperformed taxable fixed-income as market volatility picked up amid an escalation of the US-Iran conflict with renewed military strikes that drove oil prices higher and spurred inflation concerns. Treasury yields rose 7-8 basis points across the curve during the week. Municipals trailed Treasuries higher but outperformed thanks to strong demand. Supply rebounded from the prior week, but demand remained robust. As summer travel season begins, this week we provide an update on the transportation sector.

Supply Rebounded, but Demand Remained Strong

Fund Flows ($1.4 billion of net inflows): During the week ending July 8, weekly reporting municipal mutual funds recorded $1.4 billion of net inflows, marking the 12th consecutive week of inflows, according to Lipper. The intermediate-term category led demand with $523 million of inflows. The long-term category recorded $405 million of inflows and the short-term category reported $326 million of inflows. Last week’s inflows bring year-to-date (YTD) inflows to $57 billion.

Supply (YTD supply of $315 billion; up 12% YoY): The muni market recorded $1 billion of new-issue supply last week, rebounding from the prior holiday-shortened week. YTD new-issue supply of $315 billion is 12% higher than the prior record-issuance year, with tax-exempt issuance up 13% year-over-year (YoY) and taxable issuance up 6%. This week’s calendar is expected to increase to $12 billion. Largest deals include $2.5 billion New York State Thruway and $2.4 billion Aquarion CT Water Authority transactions.

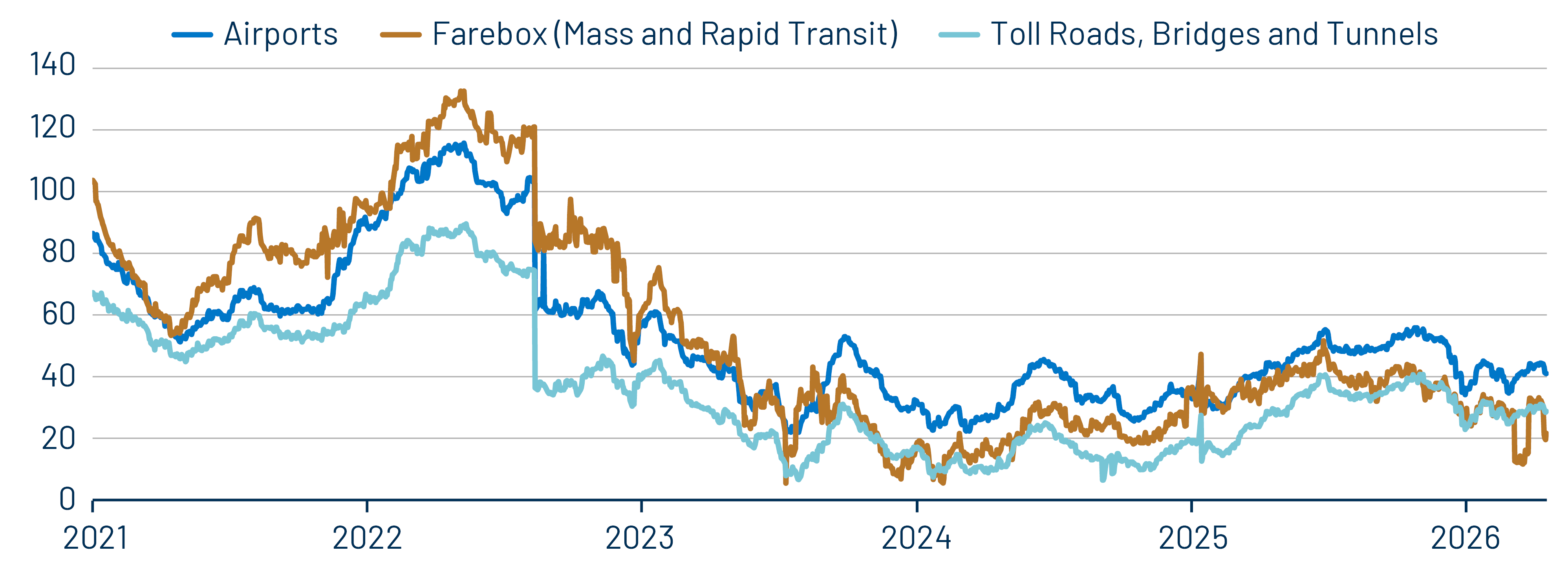

This Week in Munis: Summer Travel

With geopolitical conflict contributing to oil price volatility, fuel prices are back on the shortlist of issues worth watching in the municipal transportation sector. Not because every move at the pump changes credit quality overnight, but because fuel costs expose important differences in the credit profiles of toll roads, airports and mass transit systems. From a credit perspective, the key question is not simply whether fuel prices move higher or lower, but which issuers have the demand stability, pricing power and financial flexibility to absorb that volatility.

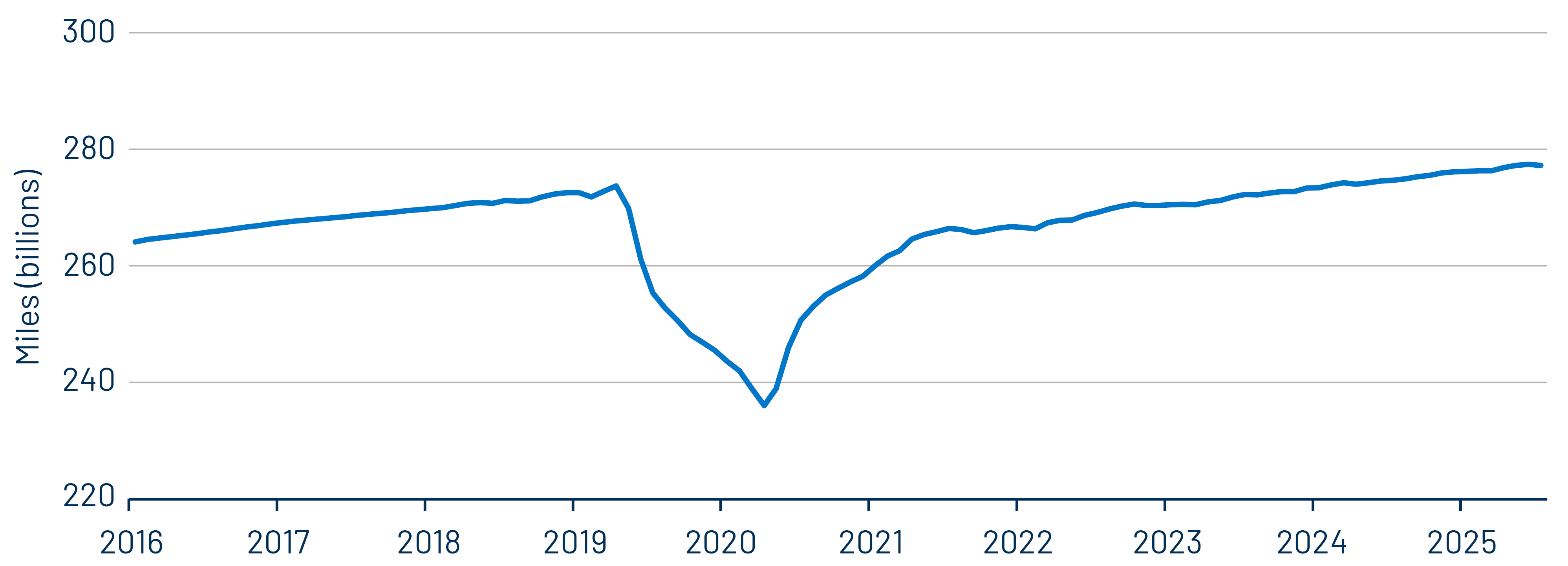

Toll roads remain a strong credit story within the transportation sector, as vehicle miles traveled continue to exceed pre-pandemic levels. While higher gasoline prices can reduce discretionary driving, the effect on mature toll systems has historically been modest. Short-run gasoline demand elasticity is generally estimated at roughly -0.02 to -0.04, implying that even a 25% increase in fuel prices would likely reduce driving demand by only about 0.5% to 1.0%. Established commuter corridors and urban expressways typically maintain stable traffic volumes because drivers often lack practical alternatives. Many issuers also benefit from annual toll escalators of 3% to 5% or CPI-linked pricing frameworks that allow revenue growth to outpace traffic growth. Combined with senior-lien debt service coverage ratios that often exceed 2.0x, the sector’s overall credit outlook remains stable to positive.

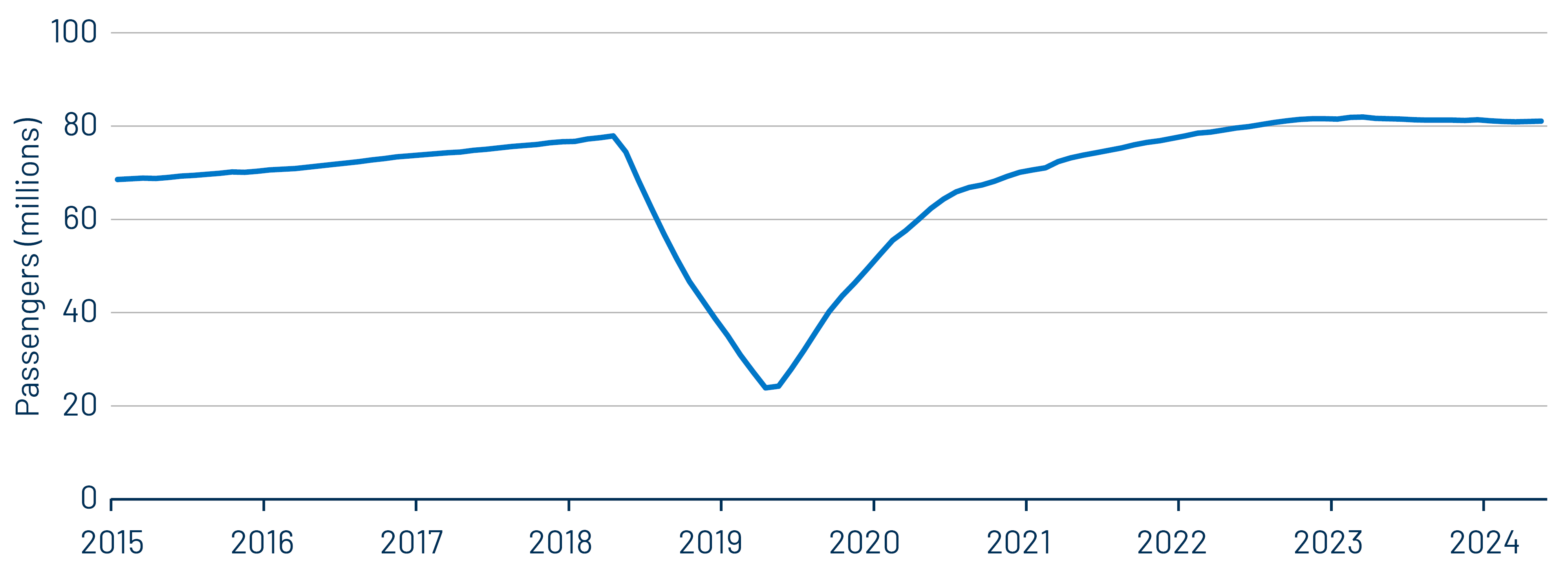

Airports face a different challenge because fuel prices affect credit quality indirectly through the airlines. Jet fuel can account for roughly one-quarter of airline operating expenses, so rising fuel costs often lead carriers to increase fares, reduce capacity or concentrate service at their most profitable hubs. Air travel demand is generally more price-sensitive than automobile travel, with route-level fare elasticity commonly estimated near -1.4. As a result, a 10% increase in airfares could reduce passenger demand by approximately 14%, particularly across leisure and short-haul markets. Although TSA checkpoint screenings remained above 900 million in 2025, passenger growth has begun to normalize. At the same time, US airports face an estimated $174 billion of infrastructure needs over the next five years, increasing pressure on future borrowing requirements and cost-per-enplanement metrics. As a result, credit differentiation is likely to widen between large, diversified hub airports and smaller facilities with greater dependence on a limited number of airline partners.

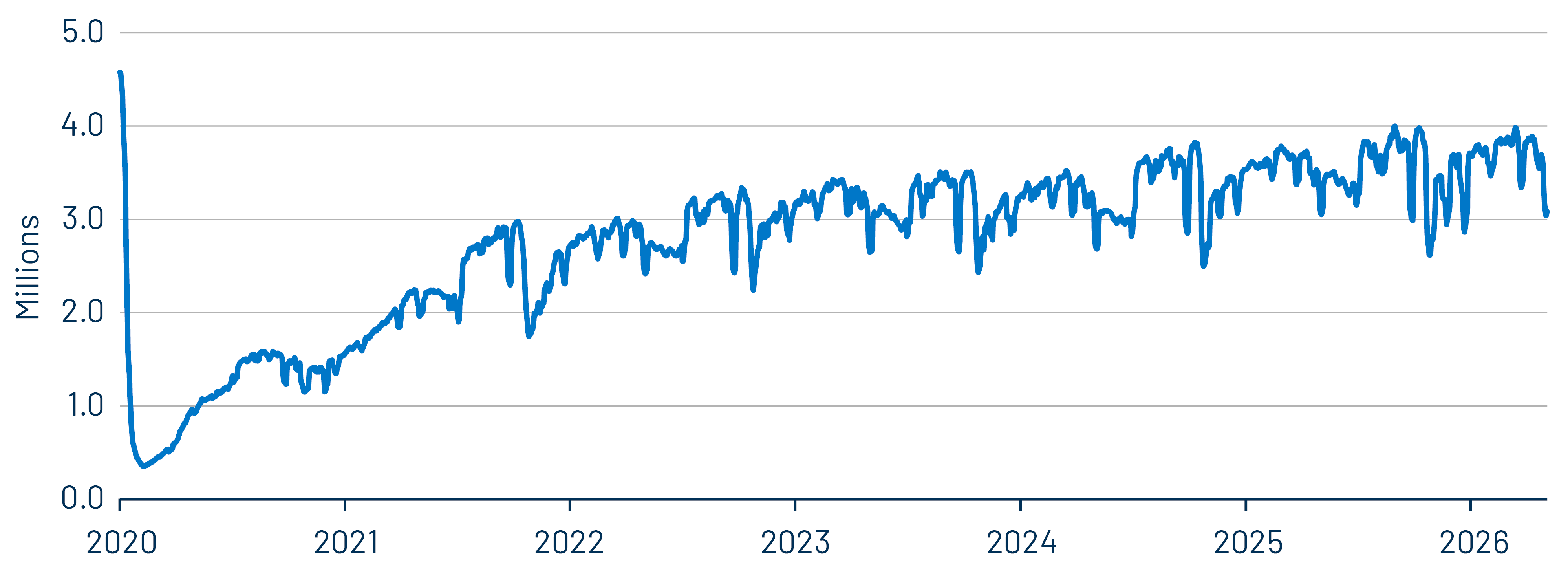

Mass transit presents the most challenging credit profile within the transportation sector. National ridership has recovered to roughly 8.1 billion annual trips, but many agencies continue to contend with weak farebox recovery. For example, the New York MTA’s maximum daily ridership remains approximately 17% below pre-pandemic highs. In addition, mass transit systems are challenged by labor-intensive operating budgets and an estimated $140 billion state-of-good-repair backlog. Historically, a 10% increase in gasoline prices has produced only about a 0.6% short-term increase in transit ridership, highlighting the relatively limited demand response to higher fuel costs. While higher fuel prices may provide a modest boost to ridership, they also increase diesel, electricity and other operating costs. Consequently, the primary credit challenge for most transit systems remains the sustainability of recurring operating support rather than ridership growth alone.

From a valuation perspective, we believe the transportation sector continues to offer attractive income opportunities for municipal investors. However, following broad fundamental improvement across the municipal market and tighter spreads across fixed-income, relative value between transportation subsectors has become increasingly compressed. As a result, issuer selection has become more important than broad sector allocation. We believe active managers’ ability to evaluate the downstream effects of geopolitical developments, fuel price volatility and issuer-specific operating fundamentals can enhance security selection and ultimately improve risk-adjusted investment outcomes.

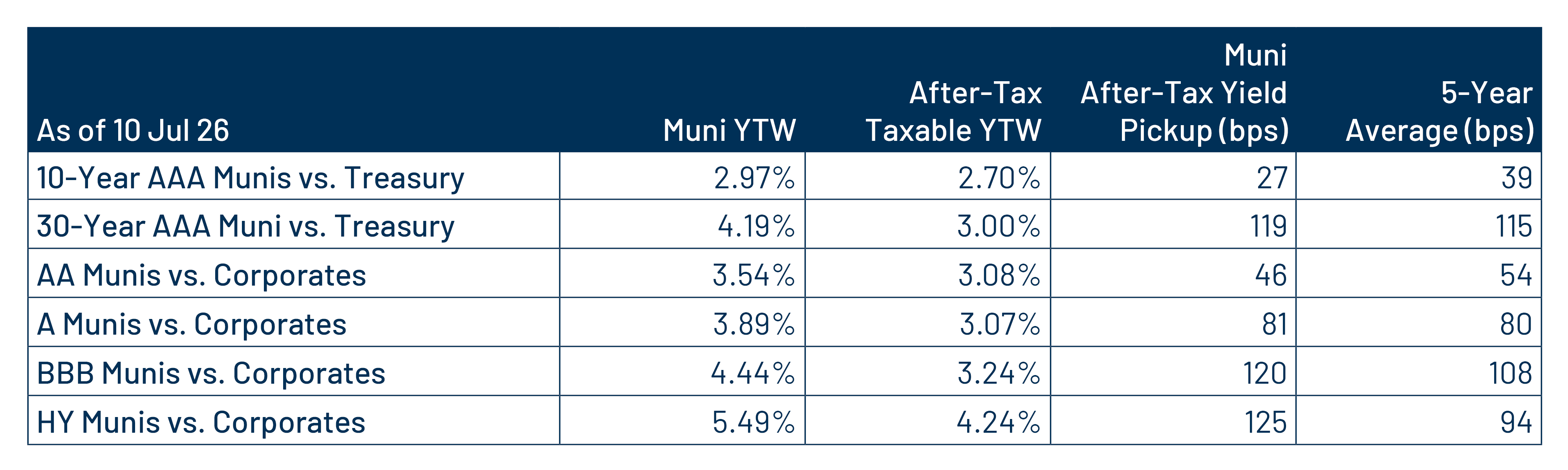

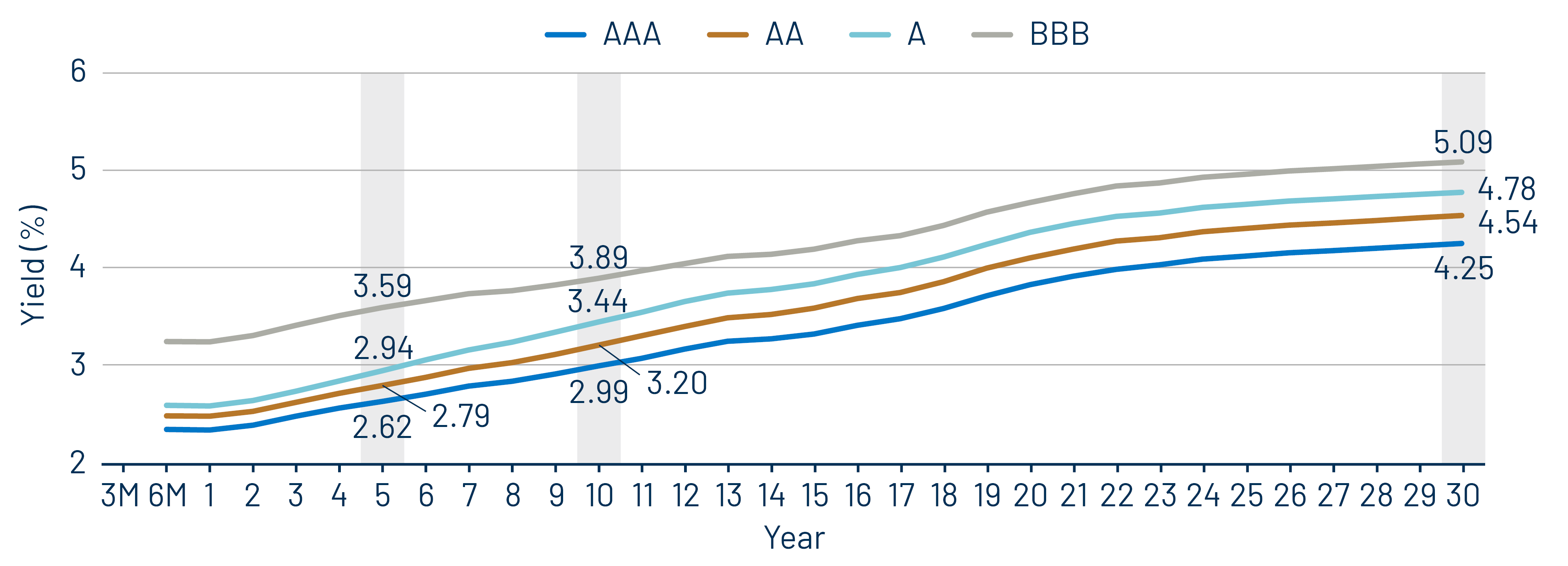

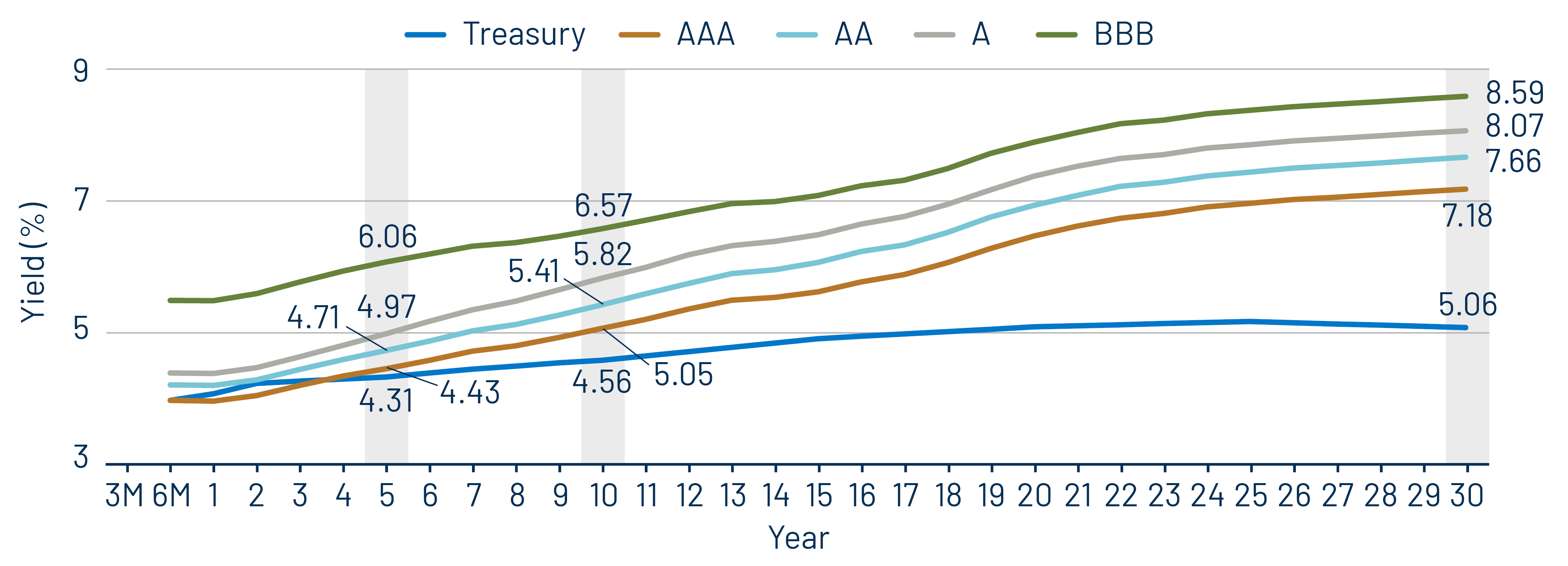

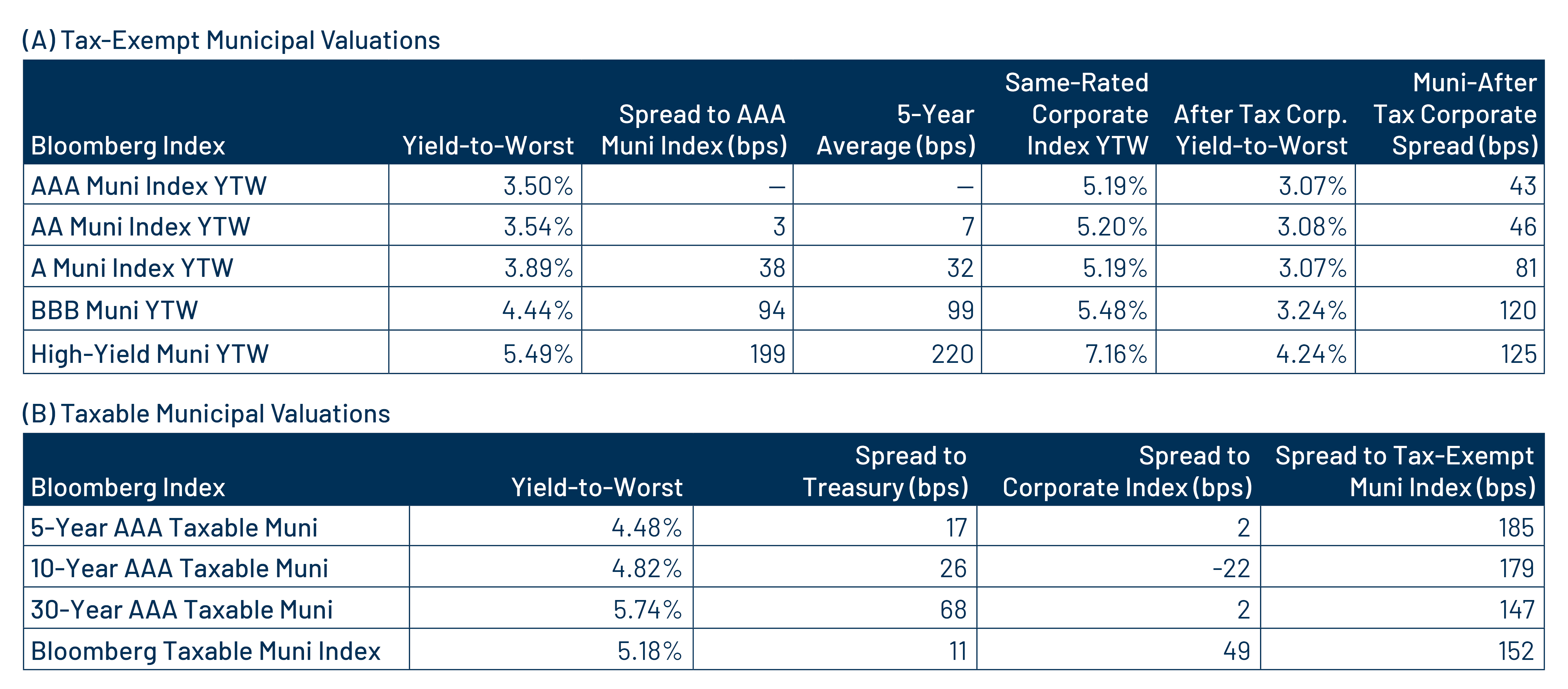

Municipal Credit Curves and Relative Value

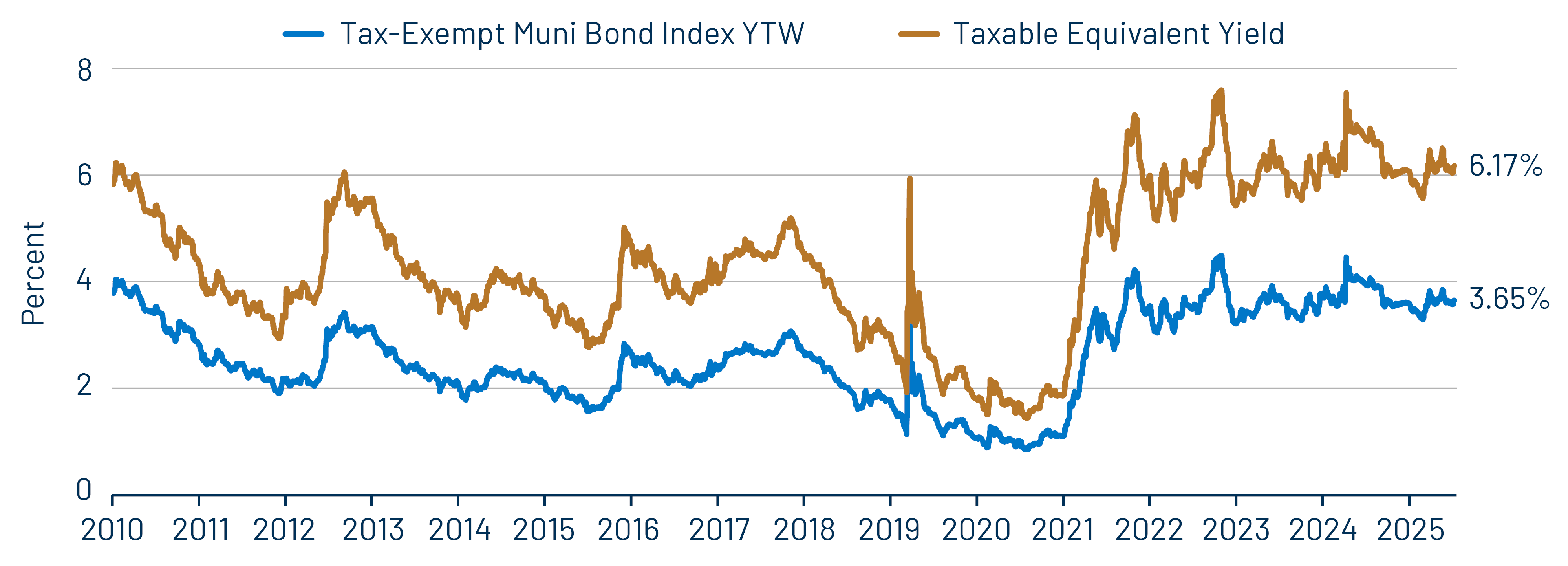

Theme 1: Municipal taxable-equivalent yields remain elevated relative to historical averages.

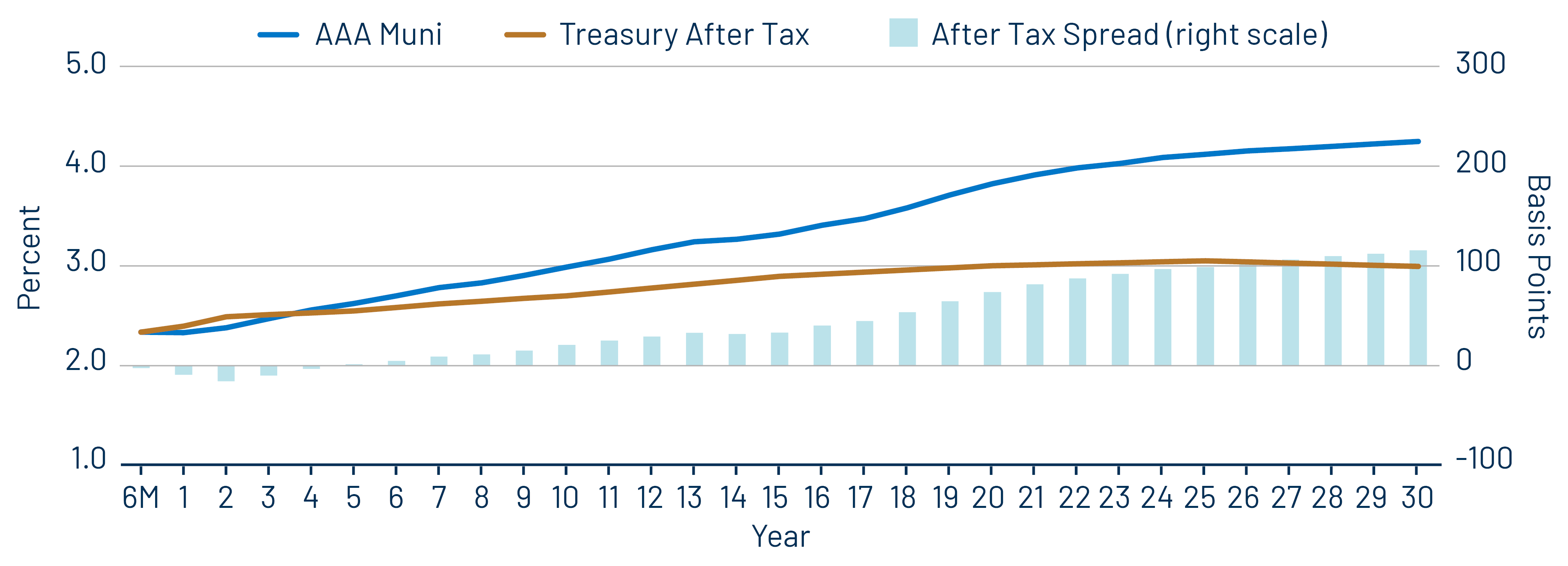

Theme 2: Munis offer attractive after-tax yield pickup vs. longer-duration or lower-quality taxable alternatives.

Theme 3: The muni curve remains steep and offers relative value in longer maturities.