Macros, Markets and Munis

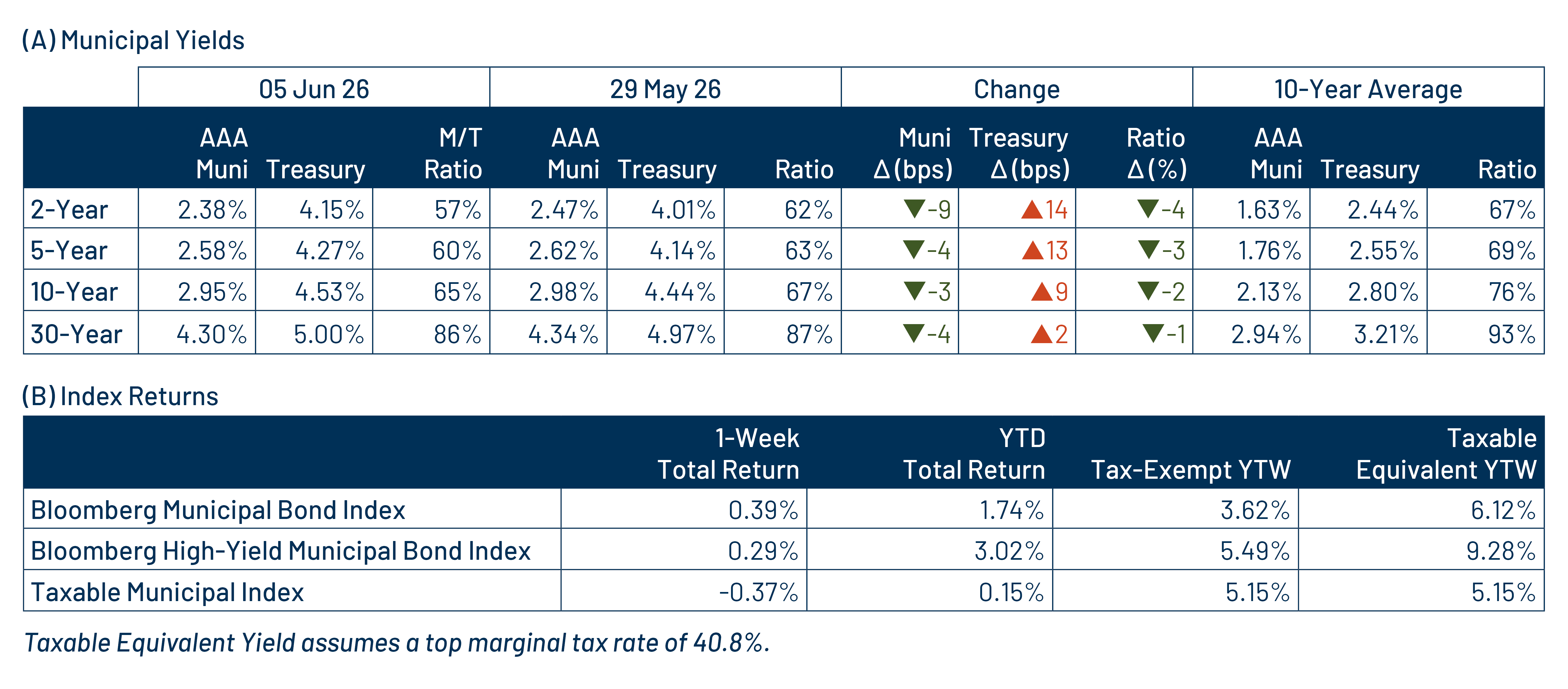

Municipals rallied last week, shrugging off Treasury weakness as the fixed-income market sold off, largely driven by strong economic data. ISM manufacturing and durable goods readings both increased from the prior month and exceeded expectations ahead of Friday’s jobs report, which indicated that employers added 172,000 jobs in May and revised March and April payrolls upward by a combined 93,000. Treasuries sold off broadly, with yields rising 2-14 basis points (bps). Treasury markets are now pricing in a Federal Reserve (Fed) rate hike by the end of the year. Meanwhile, municipals outperformed, with yields falling 4-9 bps across the curve, as robust muni demand absorbed an elevated supply calendar. Following the strong jobs report on Friday, this week we touch on the favorable muni employment gains in May.

Demand Remained Strong Amid Elevated Supply Levels

Fund Flows ($1.4 billion of net inflows): During the week ending June 3, weekly reporting municipal mutual funds recorded $1.4 billion of net inflows, according to Lipper. The long-term category represented the majority of flows, recording $1.3 billion of inflows, followed by the intermediate category that reported $14 million of inflows and the short category that recorded $43 million of inflows. Last week’s inflows bring year-to-date (YTD) inflows to $42 billion.

Supply (YTD supply of $257 billion; up 17% YoY): The muni market recorded $20 billion of new-issue supply last week, the highest level of the year. YTD new-issue supply of $257 billion is 17% higher than the prior record-issuance year, with tax-exempt issuance up 19% year-over-year (YoY) and taxable issuance up 2%. This week’s calendar is expected to remain elevated at $16 billion. Largest deals include $1.2 billion Black Belt Energy and $983 million Commonwealth of Massachusetts transactions.

This Week in Munis: Strong State and Local Hiring

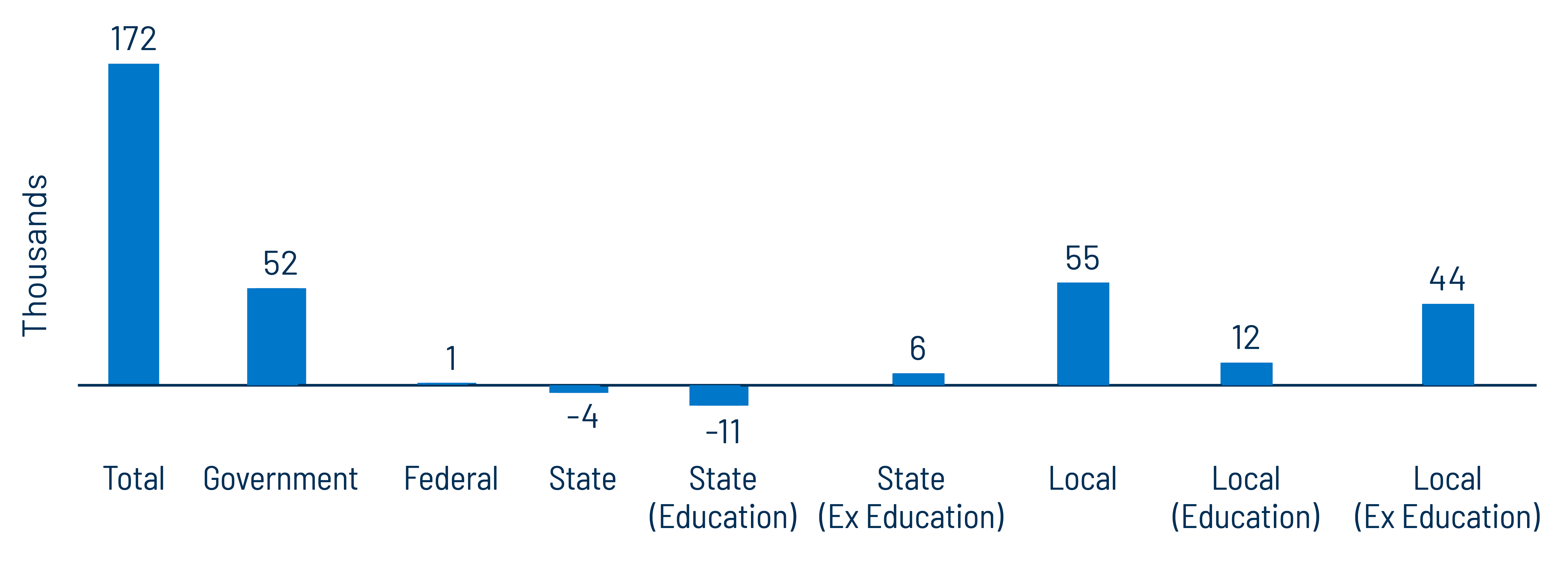

On Friday, the Bureau of Labor Statistics (BLS) reported that US employers added 172,000 jobs in May, well above consensus expectations of 85,000, while March and April payrolls were revised upward by a combined 93,000. Municipal employment was a notable contributor to the May gain in payrolls, led by local government hiring, which added 55,000 jobs. Within the local job growth, local non-education employment contributed 44,000 jobs, while local education added 12,000 jobs.

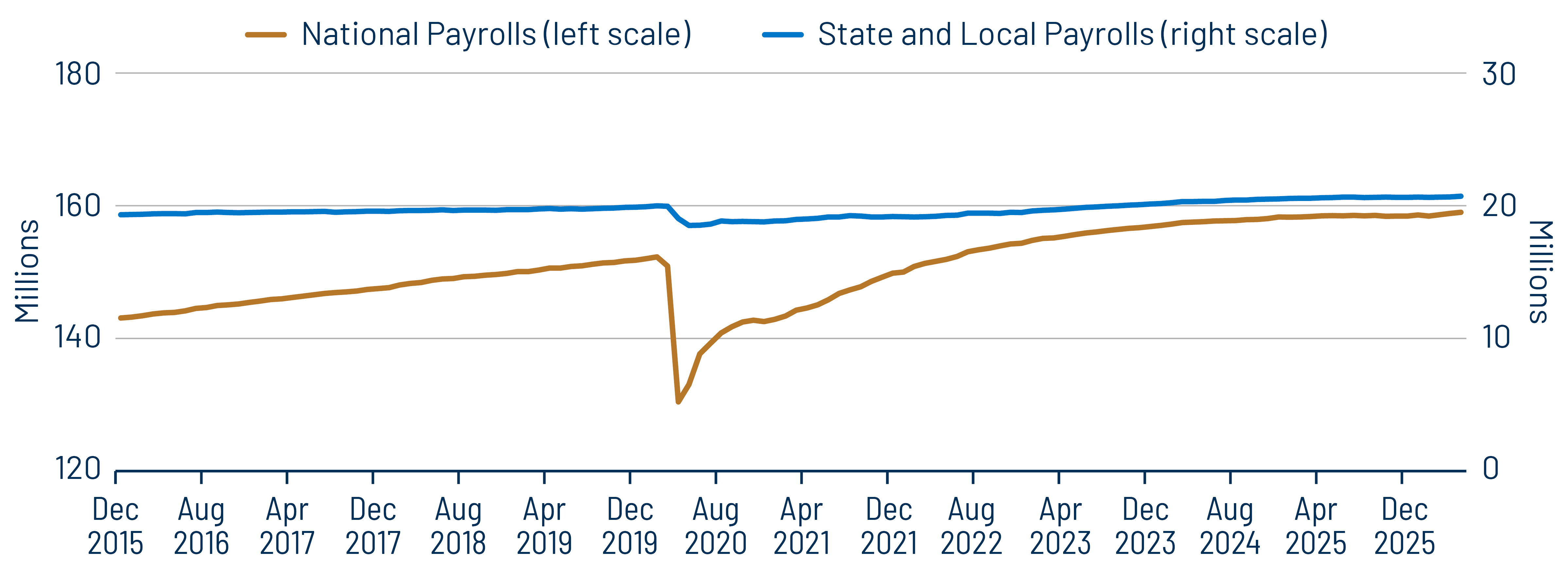

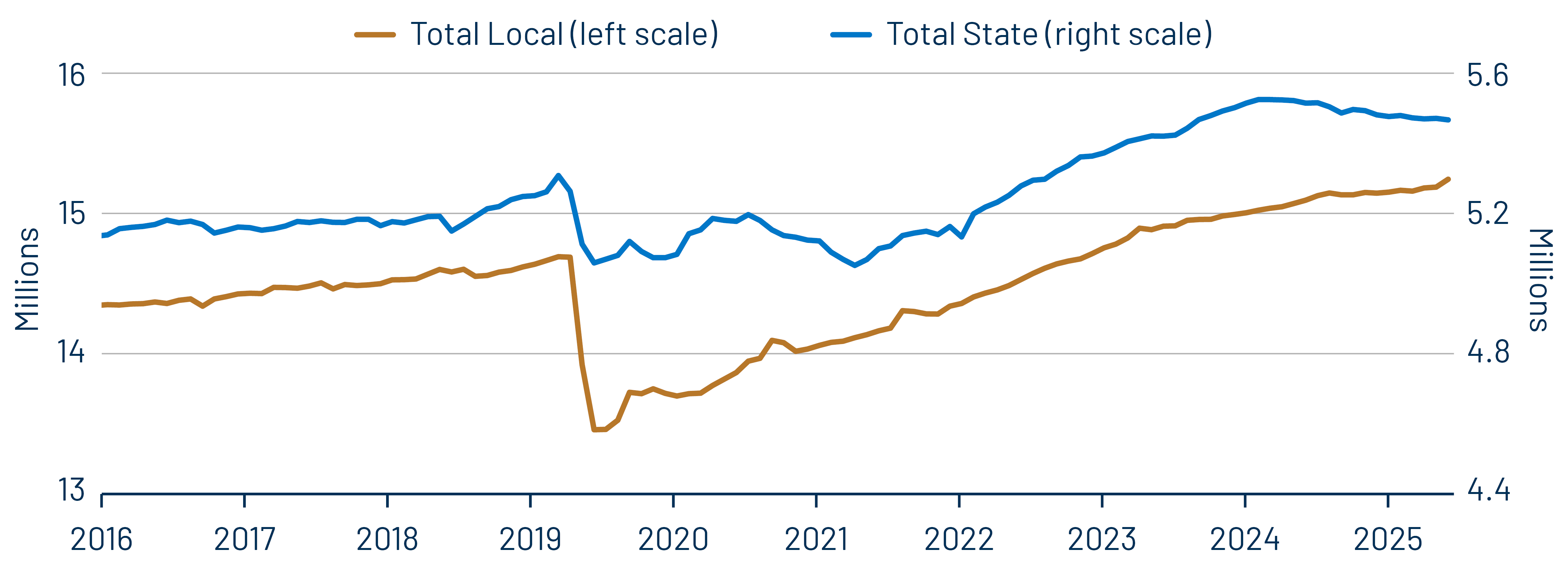

State and local employment was less affected by the pandemic compared with national employment trends, with peak employment drawdowns of 7% versus a 14% drop in total employment in 2020. Since the peak drawdowns, state and local government employment recovered more gradually, rising 9% from its lows to 20.7 million jobs, compared with a 22% rebound in total employment. State and local payrolls now stand 3.6% above pre-pandemic highs, versus 4.4% for national employment. Notably, while local employment has continued to rise throughout the recovery, including last week’s strong jobs report, state employment has steadily declined since 2024, largely driven by declines in state education.

We expect strong US employment to support municipal tax collections and credit conditions. While local government job growth in May stands out, the longer-term trend in state and local employment has been more gradual and has lagged the broader national recovery. If the Fed were to reverse course on its recent rate-cutting cycle in response to stronger economic data, a higher-for-longer rate environment could support longer-term returns while potential episodic volatility could create opportunities for active managers to deliver attractive after-tax outcomes.

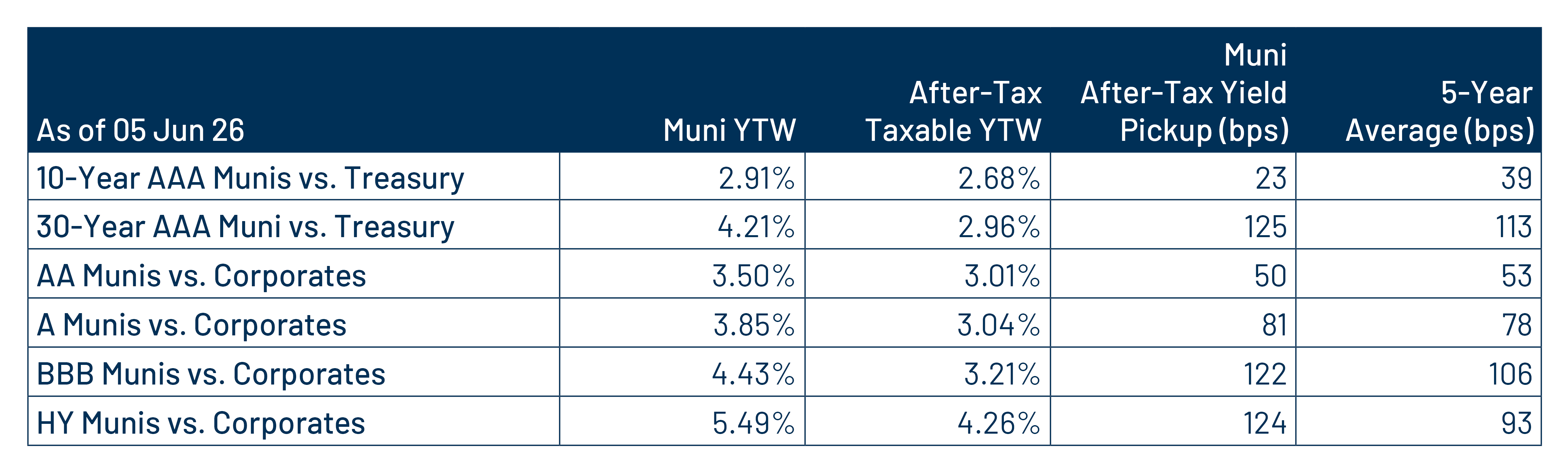

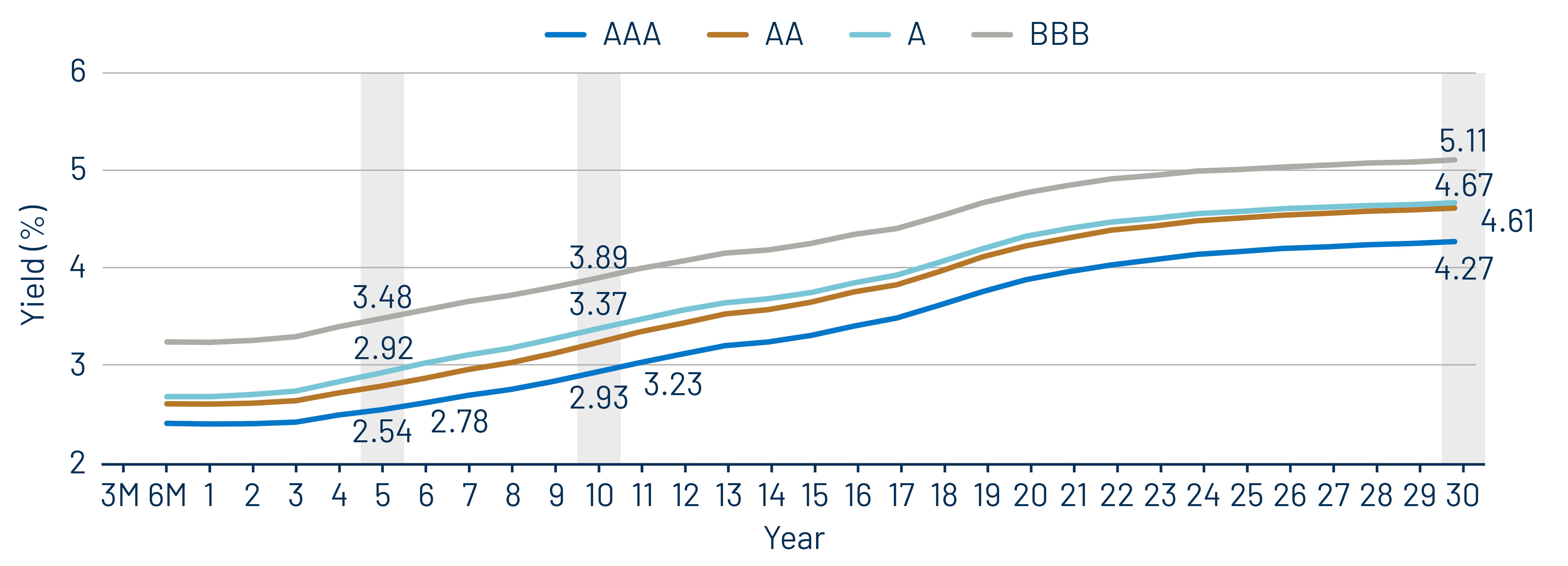

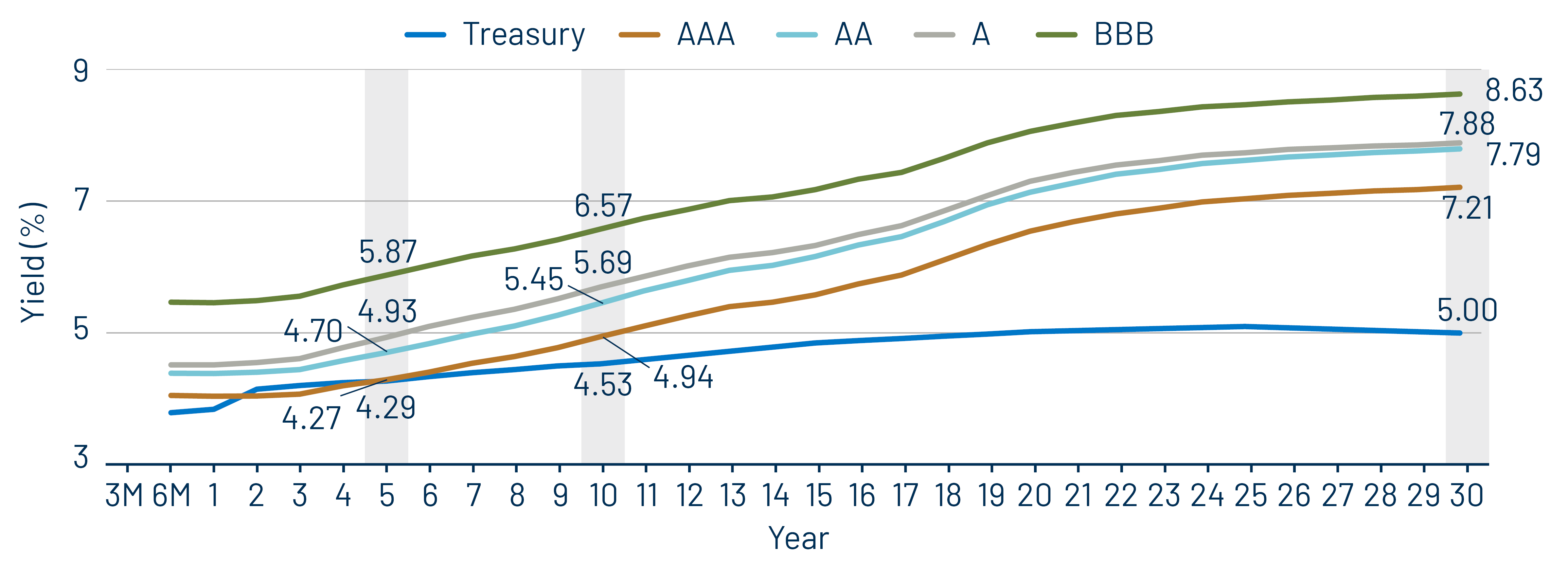

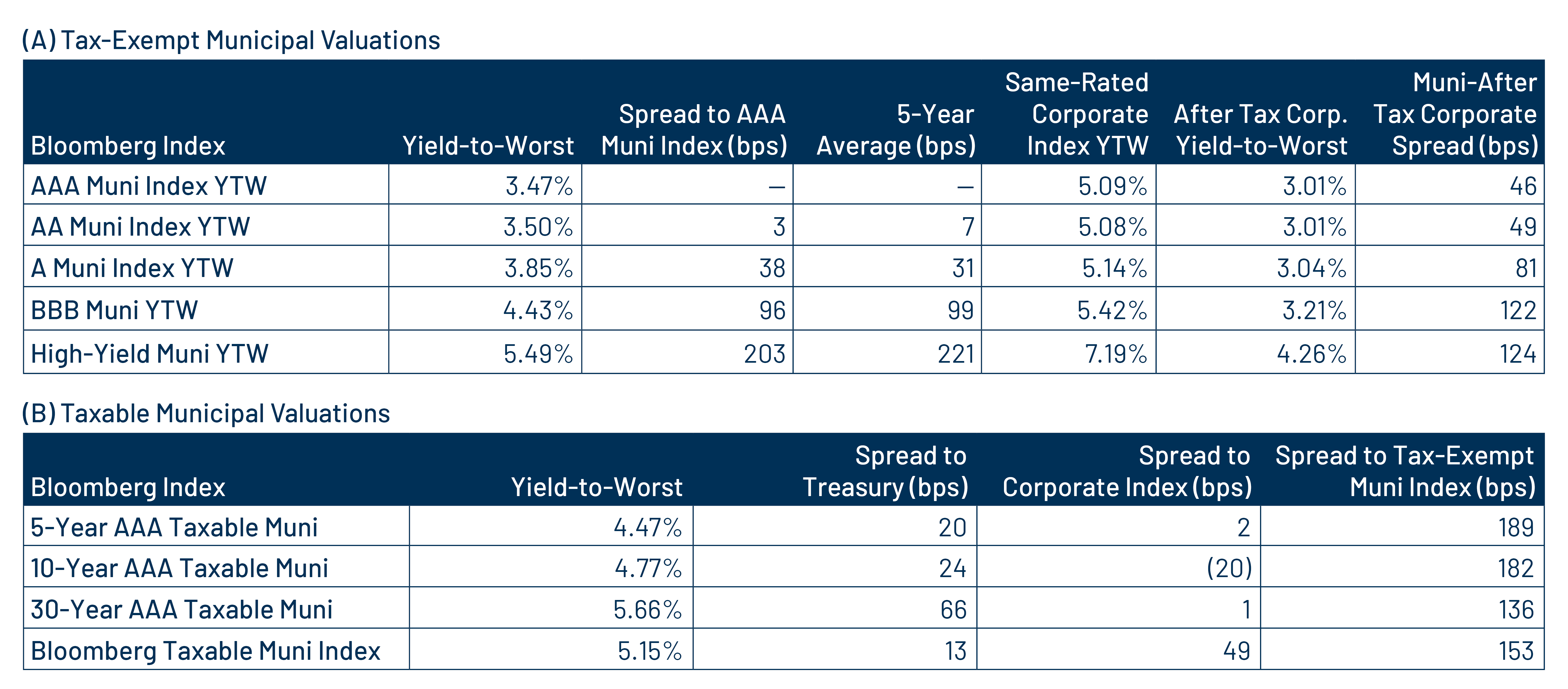

Municipal Credit Curves and Relative Value

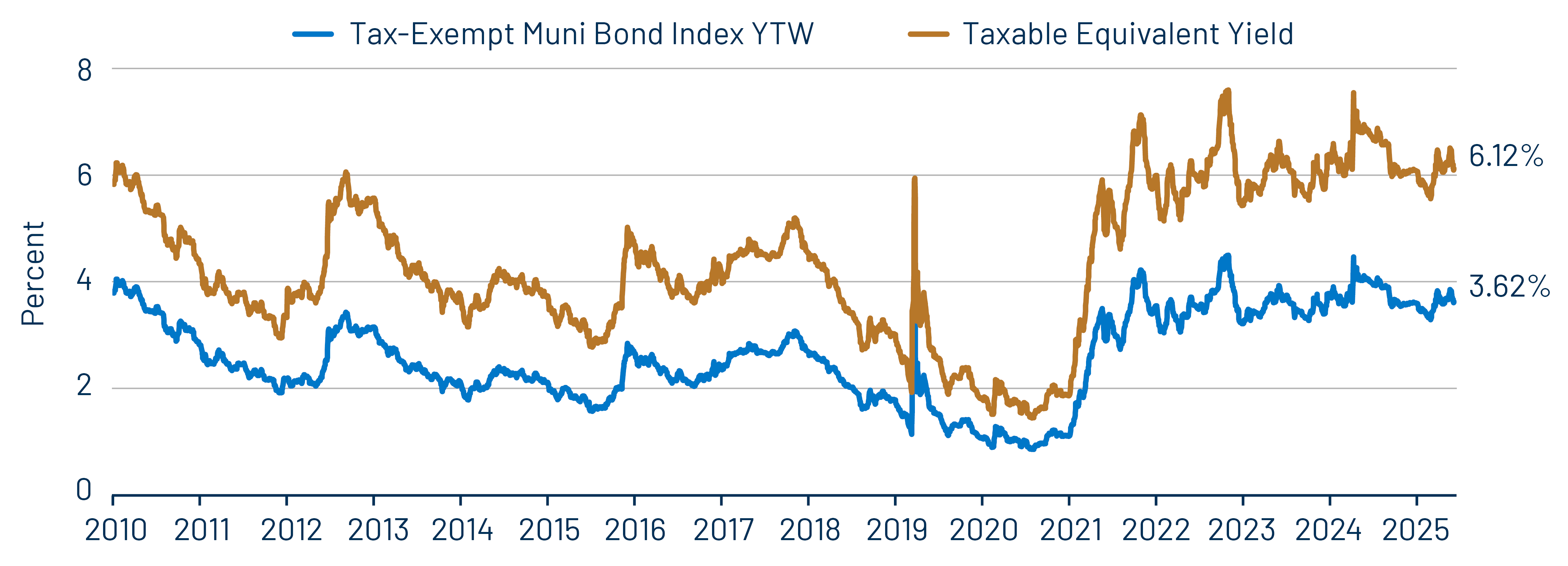

Theme 1: Municipal taxable-equivalent yields moved lower from recent highs, but remain above historical averages.

Theme 2: Munis offer attractive after-tax yield pickup vs. longer-duration and lower-quality taxable alternatives.

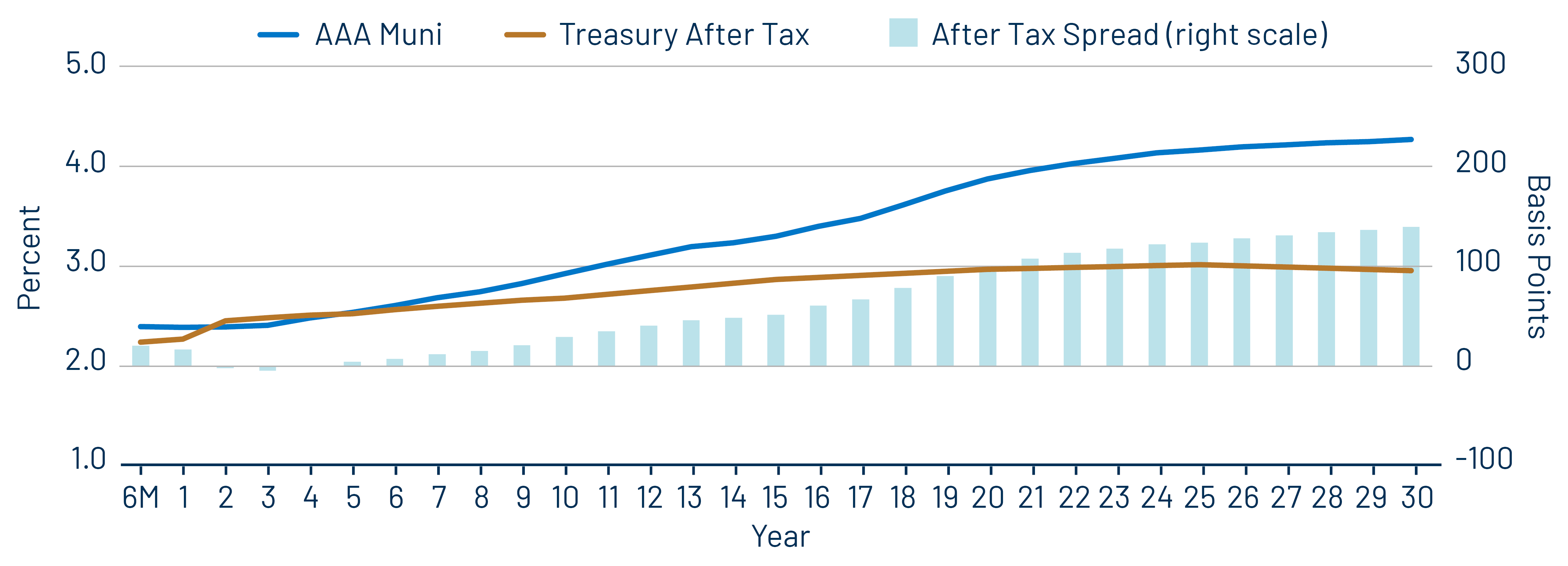

Theme 3: The muni curve remains steep and offers relative value in longer maturities.