Macros, Markets and Munis

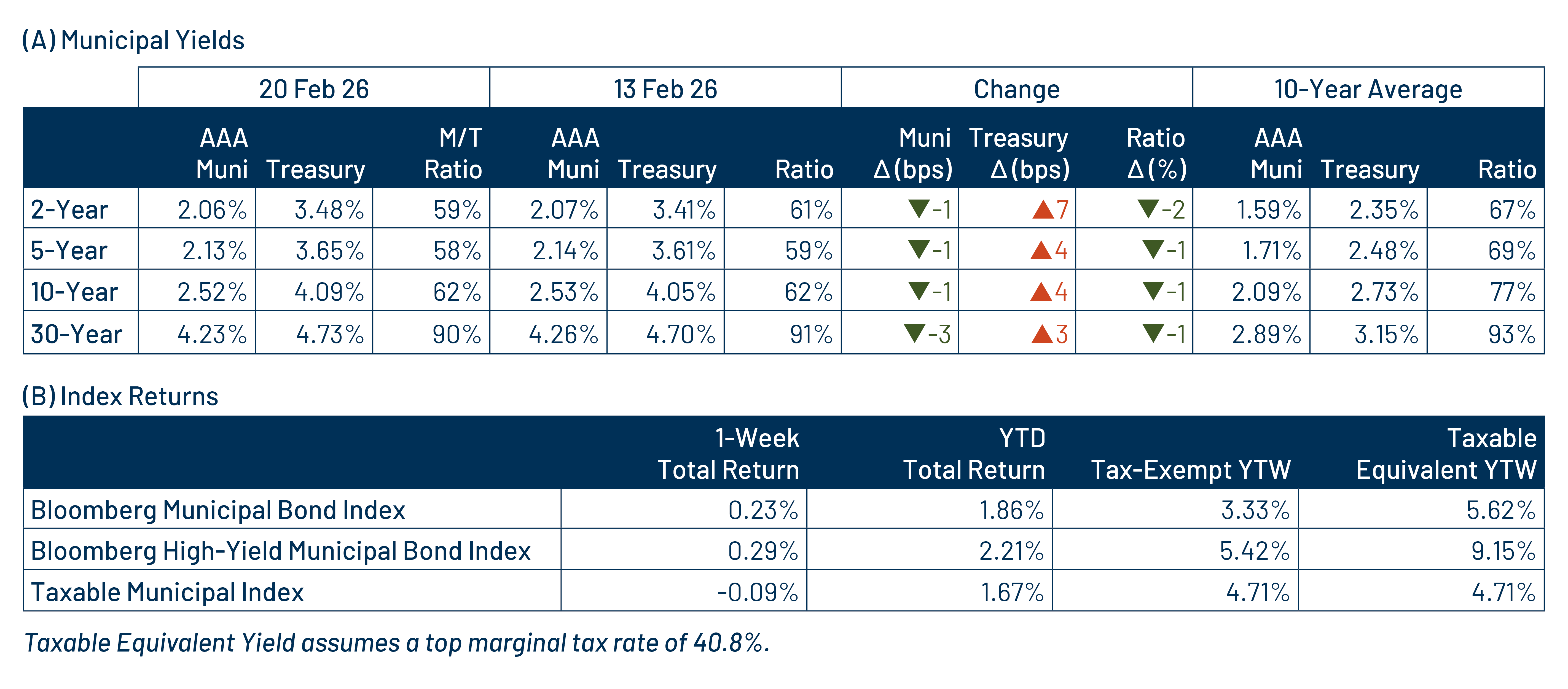

Munis posted positive returns and outperformed taxable fixed-income last week as markets digested favorable economic data. 4Q25 GDP growth showed a 3.6% decline from the prior quarter but was significantly above expectations, while core inflation trended lower to 3.0% year-over-year (YoY), modestly above expectations. The Treasury curve sold off 3-7 basis points (bps) across the curve, while municipals outperformed, with high-grade muni yields moving 1-3 bps higher across the curve. Municipal demand remained robust, underscored by a 13th consecutive week of inflows. This week we touch on budget headlines in New York that garnered attention last week.

Muni Outperformance Was Supported by Strong Fund Flows

Fund Flows ($1.3 billion of net inflows): During the week ending February 18, weekly reporting municipal mutual funds recorded $2.4 billion of net inflows, according to Lipper. Long-term, intermediate and short-term categories recorded $527 million, $550 million and $132 million of inflows, respectively. Last week’s inflows marked the 13th consecutive week of net inflows and led year-to-date (YTD) inflows higher to $17 billion.

Supply (YTD supply of $69 billion; up 16% YoY): The muni market recorded $9 billion of new-issue supply last week, down 36% from the prior week. YTD new-issue supply of $69 billion is 16% higher than the prior year, with tax-exempt issuance up 17% YoY and taxable issuance up 4%, respectively. This week’s calendar is expected to jump to $16 billion. The largest deals include $2.0 billion University of California and $1.1 billion Black Belt Energy transactions.

This Week in Munis: NY Budget Battles

With municipal budget season underway, key policy developments are emerging among large issuers, particularly within the state of New York. Last week, New York City Mayor Mamdani released his preliminary fiscal 2027 budget, presenting two paths to fund his initiatives and close a projected $5 billion gap. His preferred approach involves increasing revenue from imposing higher personal income taxes on those earning over $1 million annually along with increased corporate taxes, each of which require state approval. Should the state not support a tax increase, the mayor proposed a 9.5% across-the-board property tax rate increase alongside drawing from reserves. This has heightened credit concerns associated with potential outmigration and pressured local economic activity, stemming from increased costs for residents and businesses operating in the city.

Despite the headlines, the mayor cannot impose these tax increases unilaterally. City income tax rate increases require state legislature approval, and Governor Hochul already denounced the proposition to increase tax rates. It is unlikely her stance would change in an election year. Meanwhile any property tax increase requires City Council approval, and council leaders have already called the property tax measure a “non-starter,” highlighting risks to affordability and small businesses.

Western Asset anticipates that current political brinksmanship will eventually give way to moderate compromises such as limited tax adjustments, spending restraints or increased state aid. These outcomes, typical of hard-fought budget cycles, should help ease market skepticism regarding the mayor’s agenda. We continue to find New York municipal securities attractive for in-state taxpayers. Historically, New York muni yields traded below national benchmarks due to elevated demand driven by the state's higher tax rates. However, since the pandemic, New York muni yields have generally exceeded national levels. This shift, combined with the potential for even higher future tax rates, strengthens the after-tax value proposition for local investors seeking tax-exempt income within the state of New York.

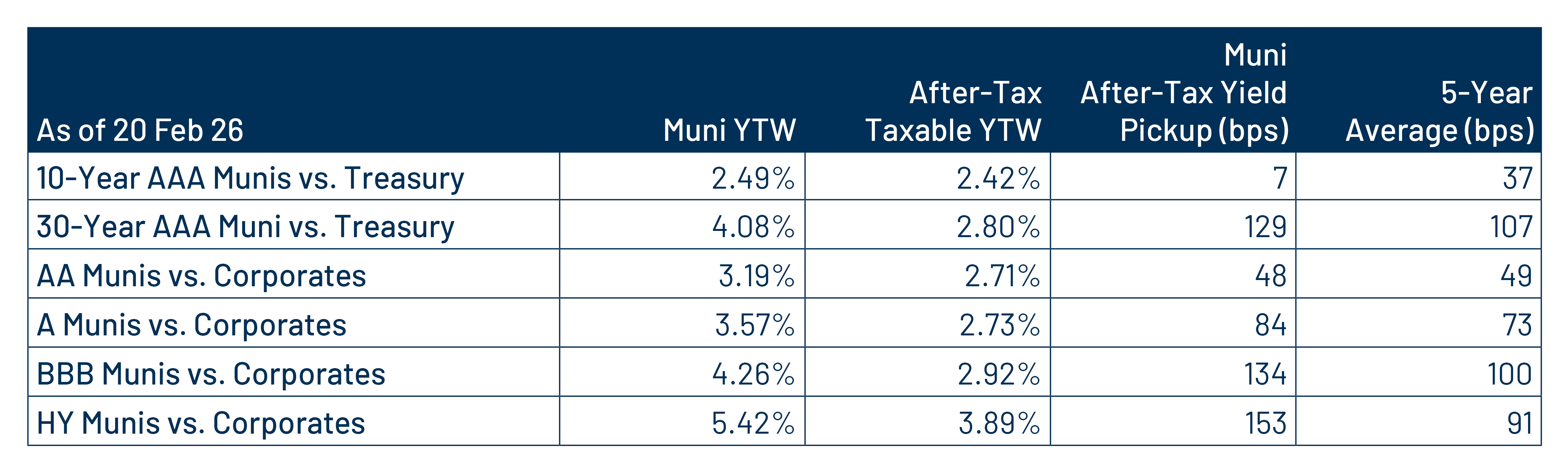

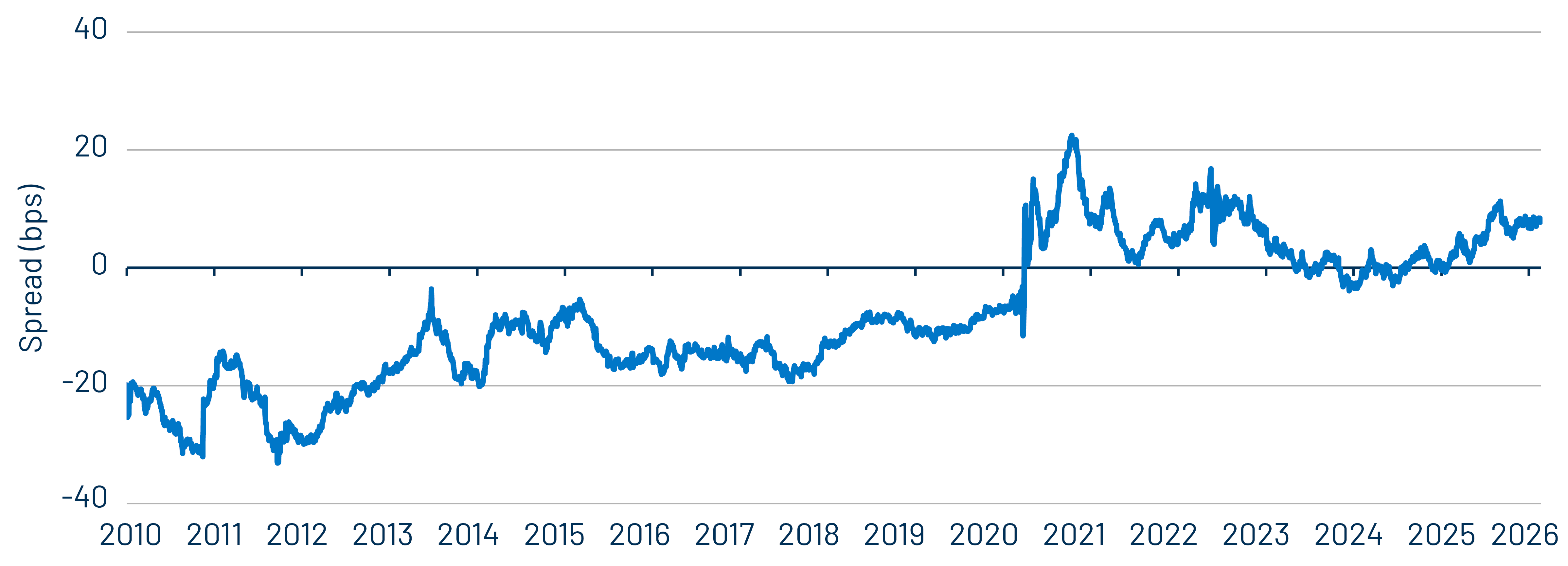

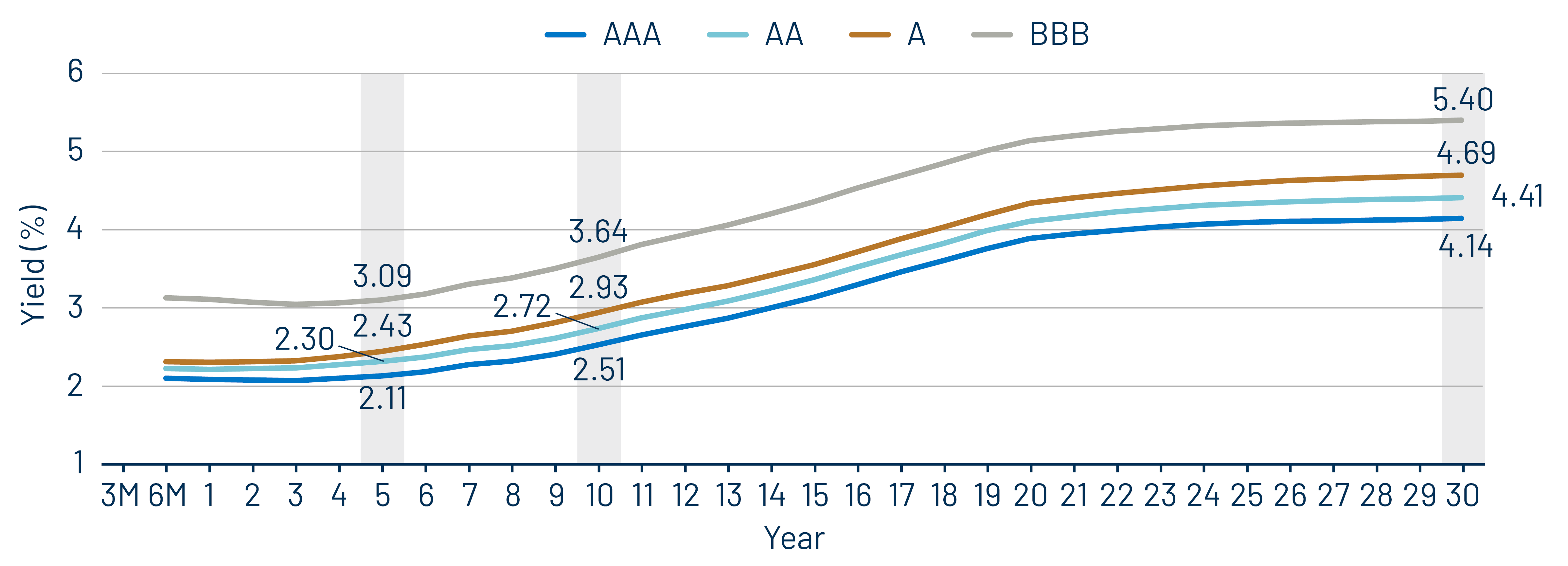

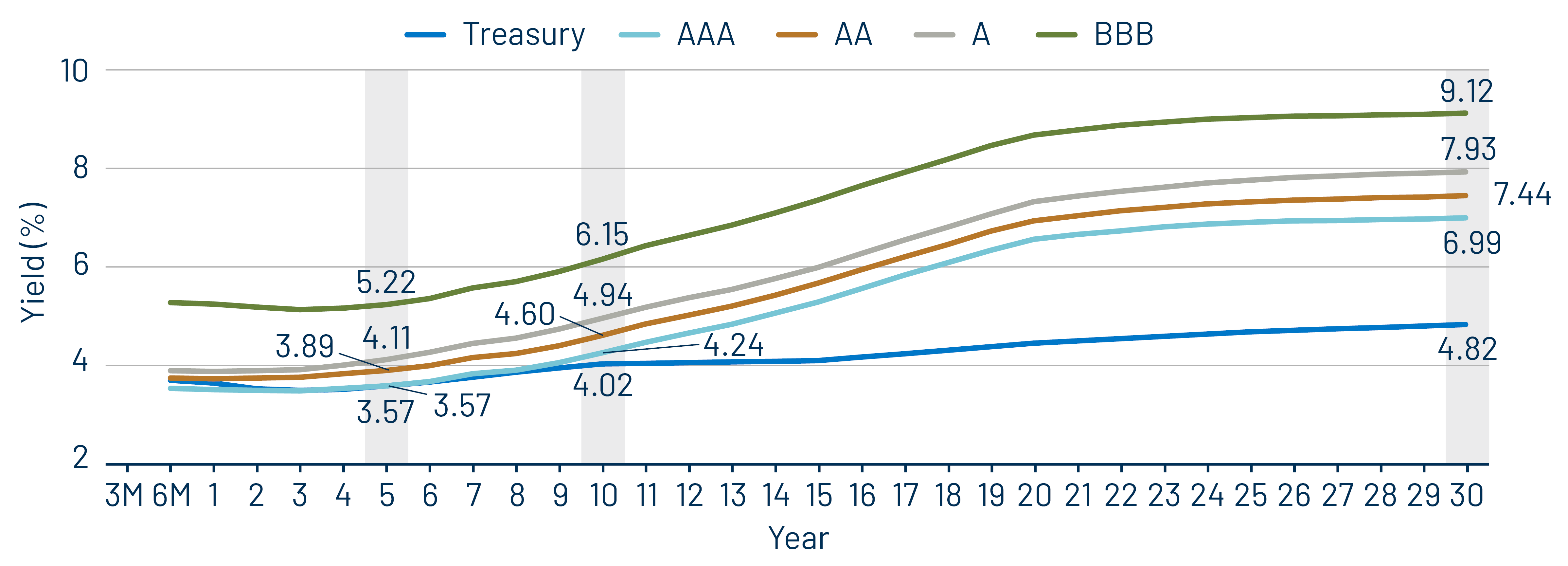

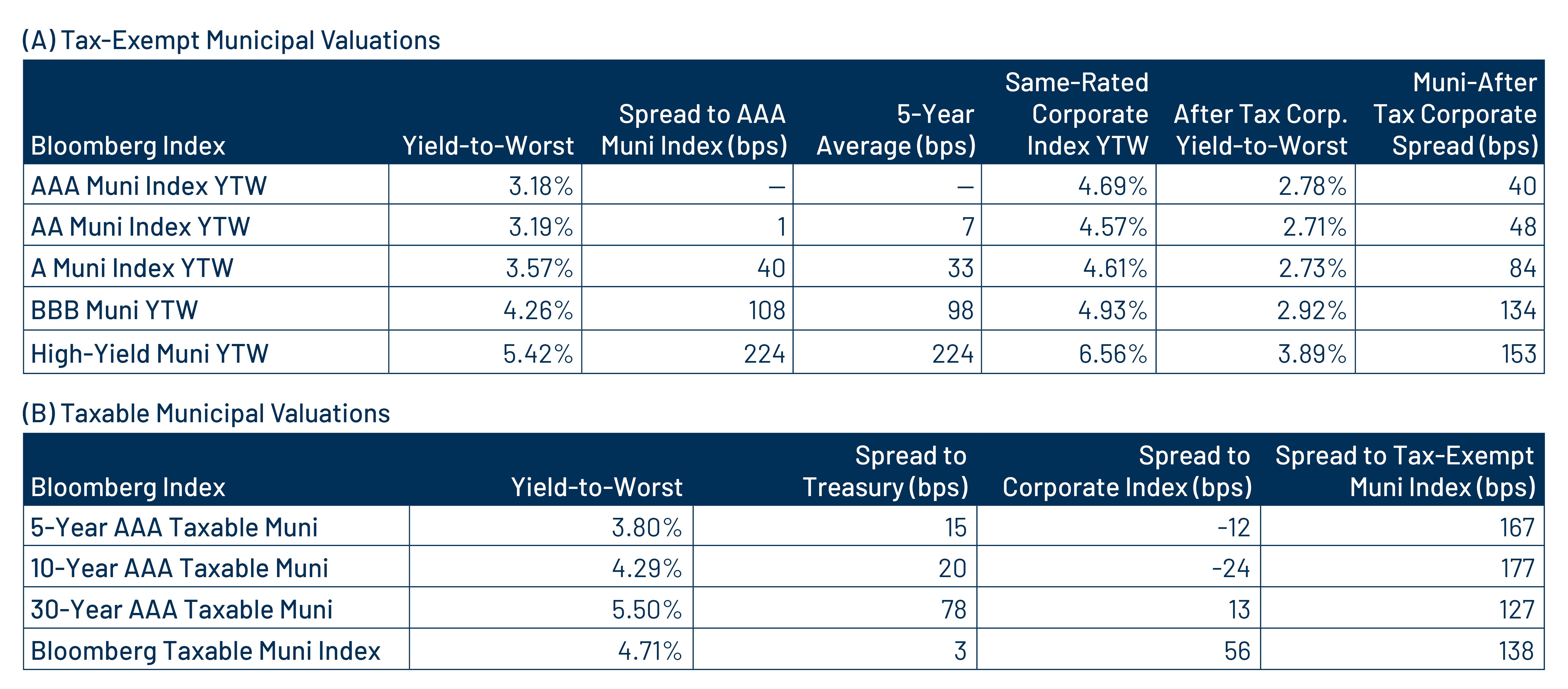

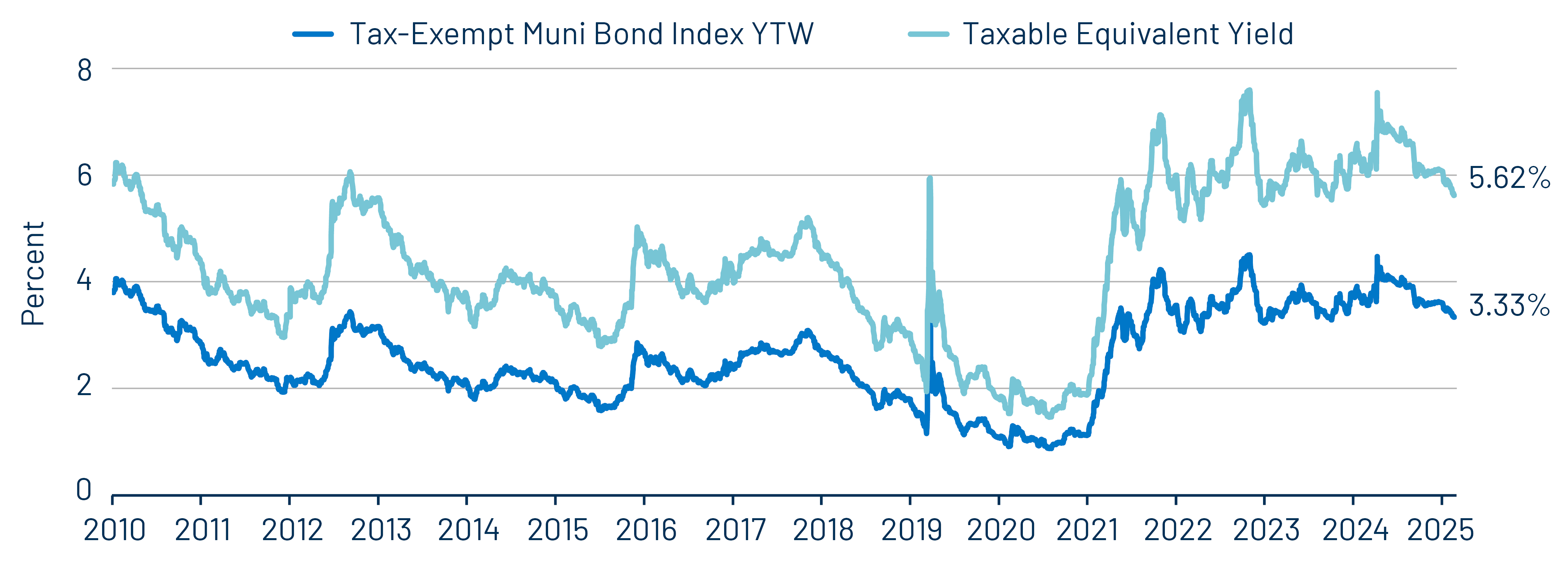

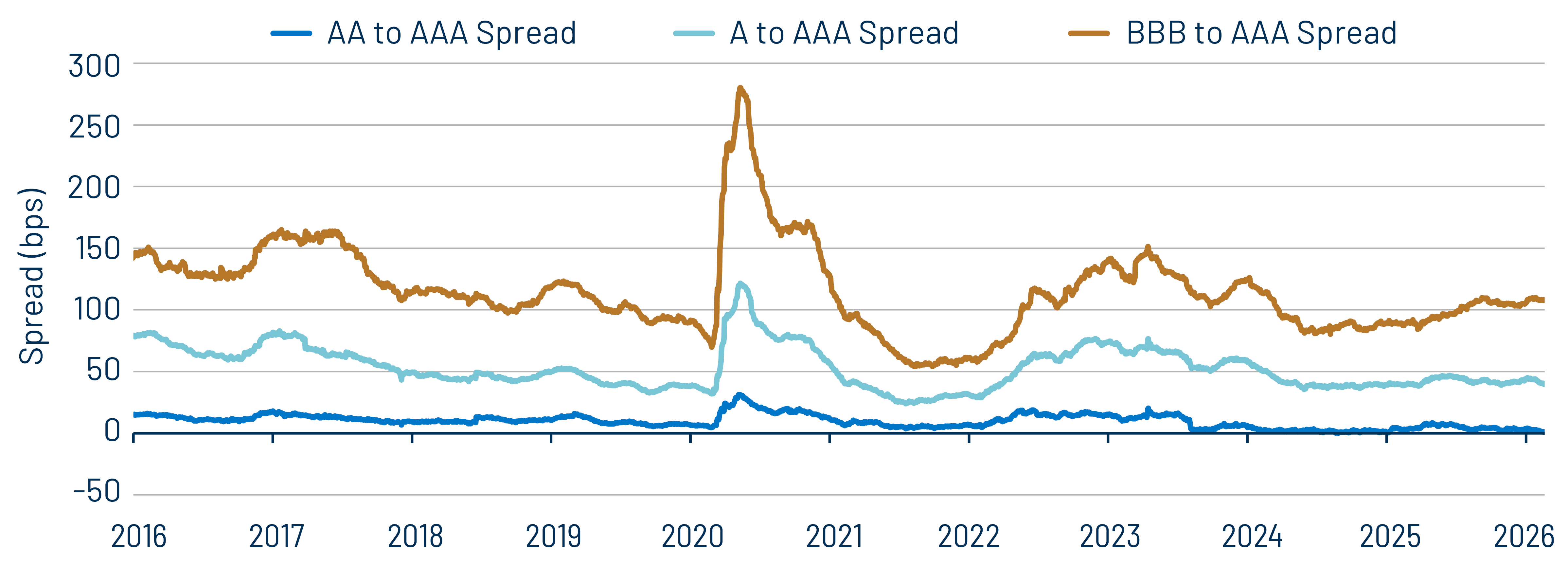

Municipal Credit Curves and Relative Value

Theme 1: Municipal taxable-equivalent yields moved lower in 2025, but remain above historical averages.

Theme 2: Munis offer attractive after-tax yield pickup vs. taxable alternatives

Theme 3: Tight municipal credit spreads warrant disciplined credit selection.