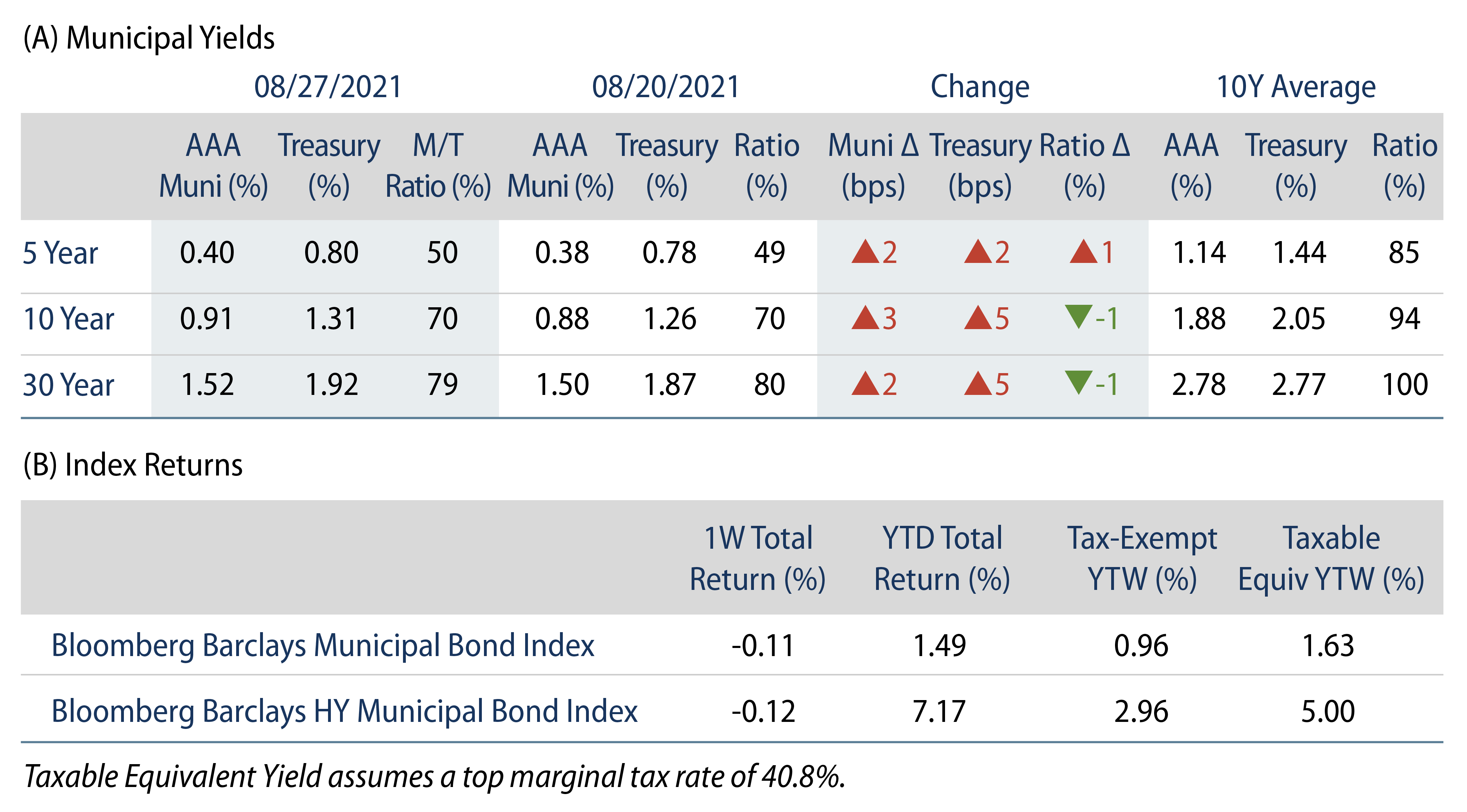

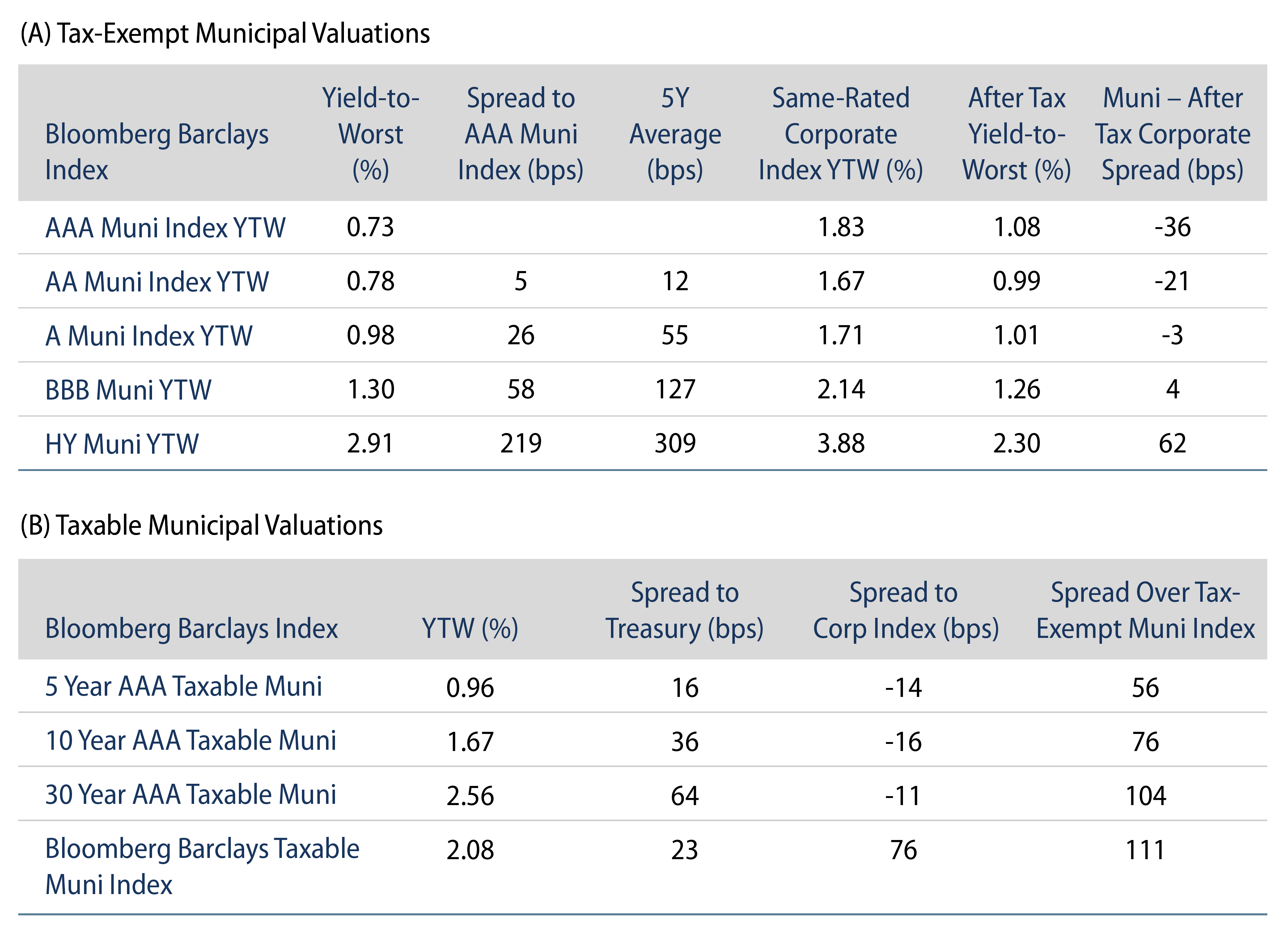

Municipals Posted Negative Returns During the Week

US munis posted negative returns as high-grade yields moved 2-3 bps higher across the curve, trailing Treasuries. Muni outperformance versus Treasuries resulted in 1% lower ratios in intermediate and long maturities. The Bloomberg Municipal Index returned -0.11%, while the HY Muni Index returned -0.12%. Technicals strengthened as fund flows maintained a record pace and supply slowed ahead of the holiday. This week, as we approach Labor Day, we check in on state and local government payrolls.

Municipal Supply and Demand Technicals Remain Strong

Fund Flows: During the week ending August 25, municipal mutual funds recorded $1.9 billion of net inflows. Long-term funds recorded $1.0 billion of inflows, high-yield funds recorded $524 million of inflows and intermediate funds recorded $253 million of inflows. Municipal mutual funds have now recorded inflows 66 of the last 67 weeks, extending the record inflow cycle to $142 billion, with year-to-date (YTD) net inflows also maintaining a record pace of $81 billion.

Supply: The muni market recorded $9.7 billion of new-issue volume during the week, down 22% from the prior week. Total issuance YTD of $301 billion is 8% higher from last year’s levels, with tax-exempt issuance trending 16% higher year-over-year (YoY) and taxable issuance trending 11% lower YoY. This week’s new-issue calendar is expected to decline to $6.3 billion of new issuance. The largest deals include $950 million New York City Transitional Finance Authority and $484 million New Hope Cultural Education Facilities Finance Corporation transactions.

This Week in Munis—Muni Payrolls Climb Ahead of the Labor Day Holiday

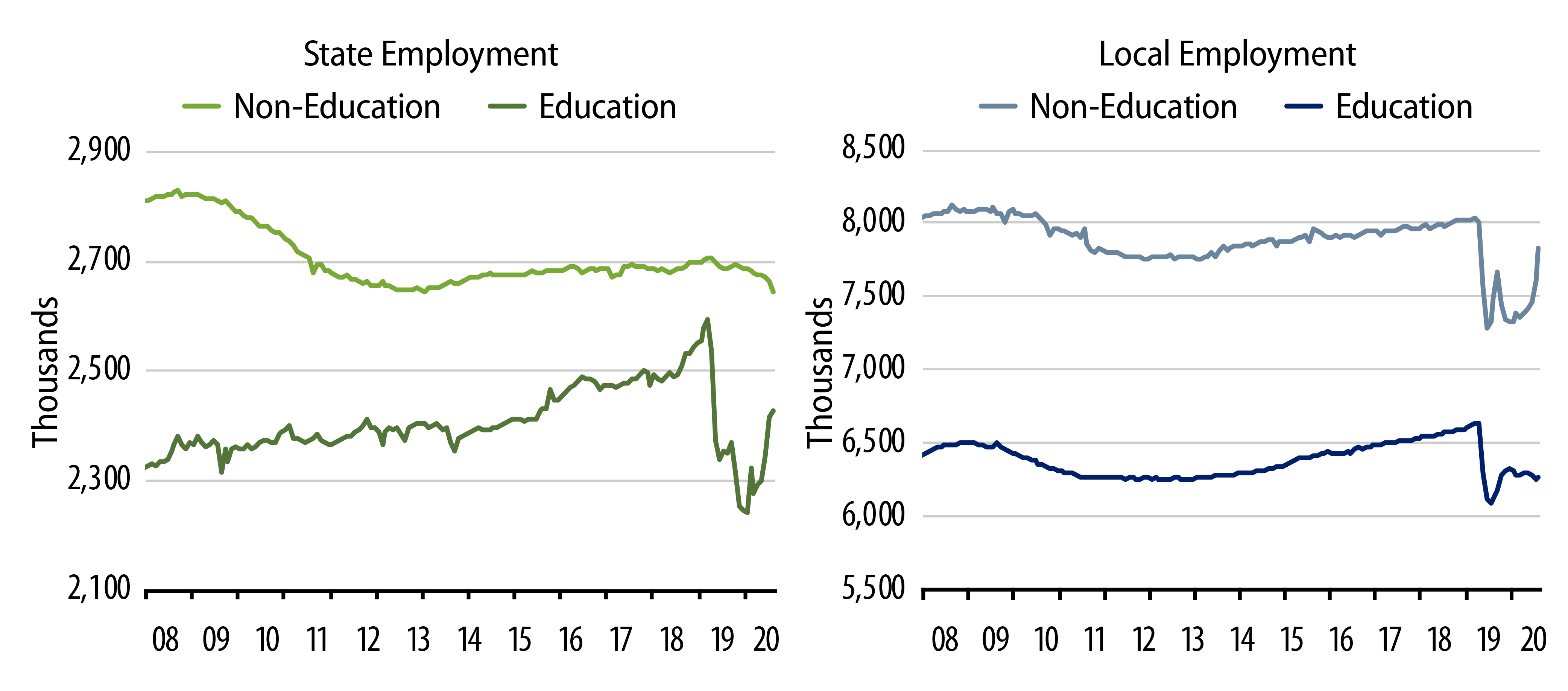

Labor Day and the reopening of schools across the US offer a timely opportunity to check in on the state of state and local government payrolls. As highlighted in a prior blog, the Bureau of Labor Statistics seasonally adjusted payroll data underscores how state and local governments were among the most impacted sectors of the pandemic, laying off approximately 1.5 million workers (-7.7% of the workforce) from the pre-pandemic highs observed in February 2020 to the lows in May 2020. Unsurprisingly, the majority of this decline was driven by education workforce furloughs, as state and local education positions accounted for 1.0 million (-9.5%) of the decline over the three-month period.

In the recovery period following the unprecedented stimulus measures from May 2020 to July 2021, we have observed seasonally adjusted state and local government payrolls regain nearly half of the reported payroll decline, reporting a gain of 728,000 positions (+3.9%), 630,000 of which were education positions. Notably, much of this seasonally adjusted gain is a reflection of the seasonal adjustment calculation of school jobs not declining as much as usual during the summer months, rather than a significant gain of new workers. From July 2020 to July 2021, non-seasonally adjusted state and local payrolls increased just 487,000 (+2.8%).

Still, we anticipate state and local government payrolls to continue to move higher into the fall as more schools reopen. However, we expect non-education governmental positions, including police, fire and social services to remain challenged. Non-education positions comprise 47% of state and local payrolls, and from May 2020 to July 2021 have only recovered 98,000 of the 531,000 positions lost during the pandemic-driven drawdowns. We believe the lagging growth in non-education positions is indicative of our prior assertion that a full state and local government job recovery could take longer than some expect.

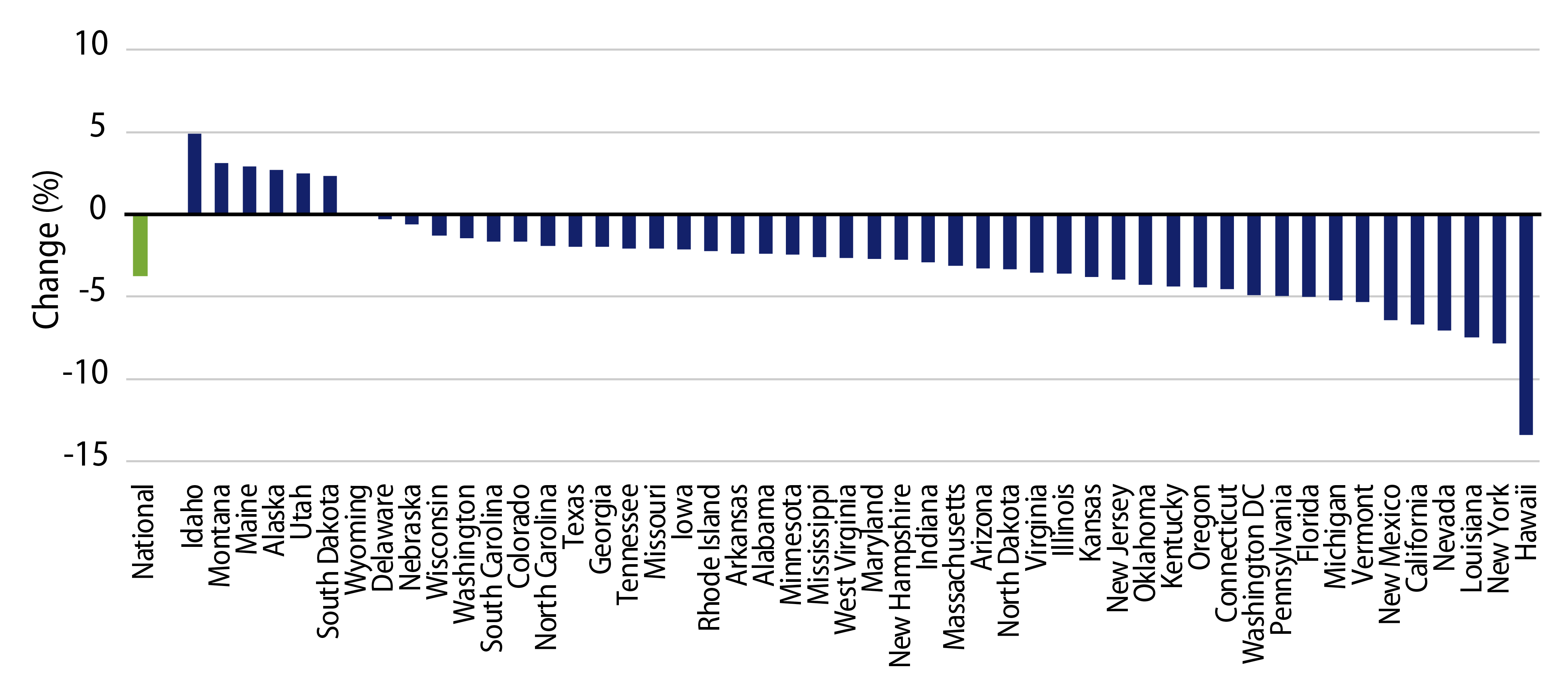

From a geographic standpoint, payrolls in Idaho, Montana and Maine were +4.9%, +3.1%, and +2.9% higher than the pre-pandemic levels observed in February 2020, respectively, exceeding the -3.7% national decline observed over the period and consistent with some of the socioeconomic shifts observed during the pandemic. Conversely, payrolls in Hawaii, New York and Louisiana remain -13.4%, -7.9%, and -7.5%, respectively, below February 2020 pre-pandemic levels, which has been significantly impacted by the decline in tourism.

We will continue to track payroll trends, which provide a timely perspective on the status of government finances and the health of regional economies. We expect relatively lower levels of governmental employment to provide budget relief and be broadly supportive of state and local issuer credit. However, we will continue to monitor regional trends that can be a drag on the credit profile of select municipal issuers, and will utilize the tight spread market environment to reduce structural risks as they emerge.