Macros, Markets and Munis

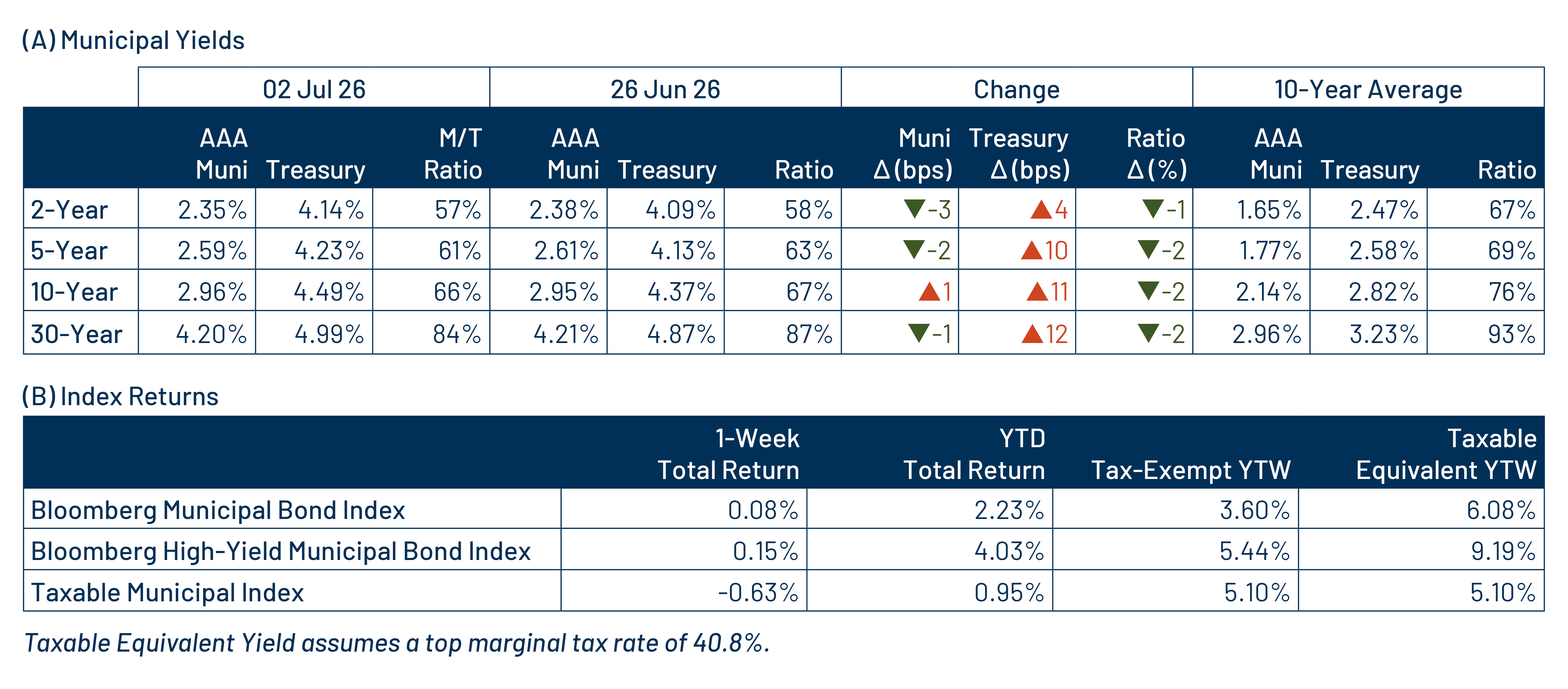

Municipals posted positive returns last week and outperformed taxable fixed-income as markets focused on labor data that showed JOLTS job openings were unchanged but came in above expectations. On Thursday, July 2, the June employment report indicated that nonfarm payrolls increased by a below-expected 57,000, with downward revisions to April and May data. The unemployment rate edged down to 4.2% from 4.3% amid a decline in labor force participation. Meanwhile, new Federal Reserve Chair Kevin Warsh noted that inflation risks have eased. Treasury yields rose 4 to 12 basis points across the curve; municipals outperformed, moving modestly lower in most maturities amid heavy demand and light supply. This week we provide a midyear muni market update.

Technicals Improved on Stronger Demand and Lighter Supply

Fund Flows ($1.7 billion of net inflows): During the week ending July 1, weekly reporting municipal mutual funds recorded $1.7 billion of net inflows, marking an 11th consecutive week of inflows, according to Lipper. The long-term category led demand with $1.1 billion of inflows, the short-term category recorded $219 million of inflows and the intermediate category reported $292 million of inflows. Inflows last week bring year-to-date (YTD) inflows to $53 billion.

Supply (YTD supply of $304 billion; up 10% YoY): The muni market recorded $5 billion of new-issue supply last week, down 65% from the prior week’s level due to the July 4 holiday. YTD new-issue supply of $304 billion is 10% higher than the prior record-issuance year, with tax-exempt issuance up 10% year-over-year (YoY) and taxable issuance up 7%, respectively. This week’s calendar is expected to rebound to $16 billion. Largest deals include $2.4 billion Aquarion CT Water Authority and $1.8 billion California State University transactions.

This Week in Munis: Midyear Update

Performance

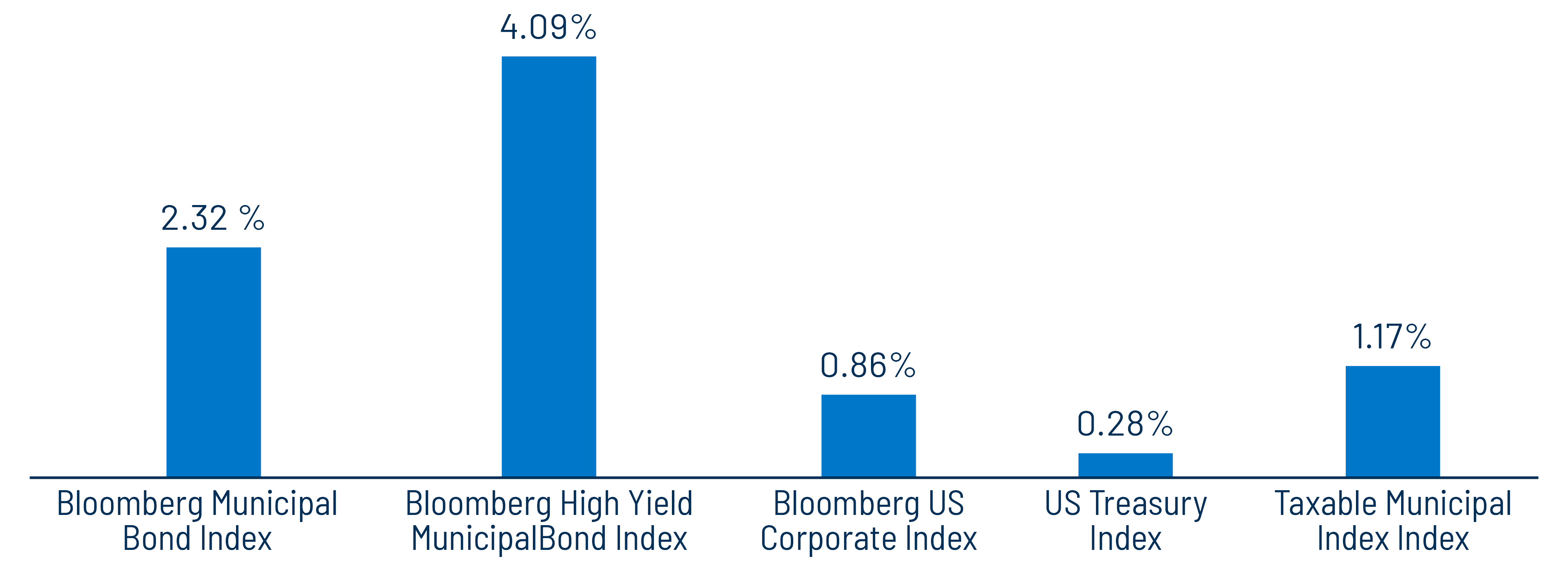

The municipal market posted strong returns during the first half of the year despite geopolitical tensions and ongoing inflation uncertainty. Rate expectations shifted meaningfully over the period, moving from anticipated 2026 rate cuts at the start of the year toward renewed concerns about higher-for-longer policy and potential rate hikes by midyear. Treasury yields rose across the curve, while the municipal yield curve generally flattened, with intermediate municipal yields increasing and longer maturities declining. Against this backdrop, the Bloomberg Municipal Bond Index returned 2.32%, outperforming both the Bloomberg Treasury Index, which returned 0.28%, and the Bloomberg Corporate Index, which returned 0.86%. Strong demand, particularly from longer-duration vehicles, helped absorb elevated new issuance and supported municipal outperformance during the period.

Supply/Demand

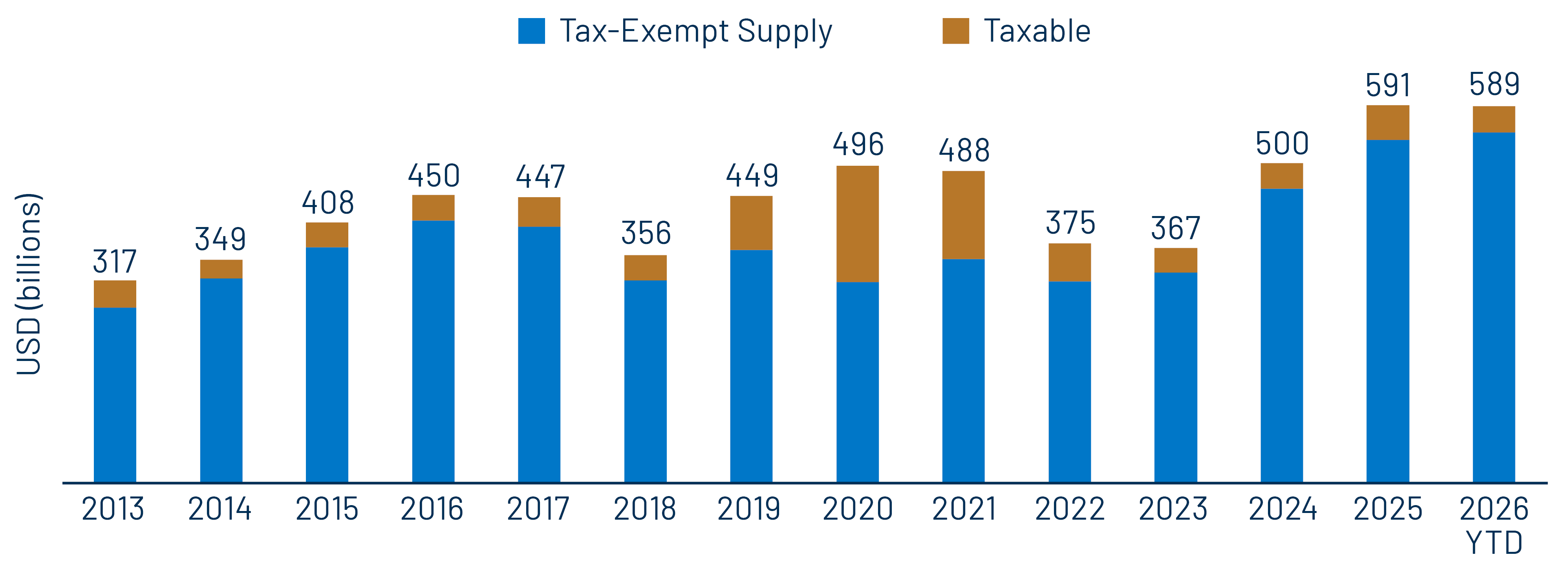

Supply: New issuance reached $295 billion in the first half of 2026, according to Bloomberg, up 7% from 1H25 and maintaining a record pace. Tax-exempt municipal issuance totaled $274 billion, up 6% YoY, while taxable supply of $21 billion was 20% below prior-year levels. A key driver of higher issuance was continued growth in prepaid gas issuance, which totaled $24 billion, more than double the prior-year level. The sector has continued to diversify the broader municipal market, expanding issuance beyond traditional governmental borrowers into corporate-backed issuance, with Google-parent Alphabet participating in its first-of-kind $1.2 billion tax-exempt structure this year.

Demand: Municipal mutual funds recorded approximately $58 billion of net inflows in the first half of the year, according to ICI, well above the $19 billion recorded through the first half of 2025. Municipal mutual funds have now attracted $161 billion of cumulative net inflows since January 2023, complementing persistent SMA demand in the marketplace. YTD flows have been concentrated largely in longer-duration strategies, according to Lipper, supporting the outperformance of longer-maturity municipals.

Fundamentals

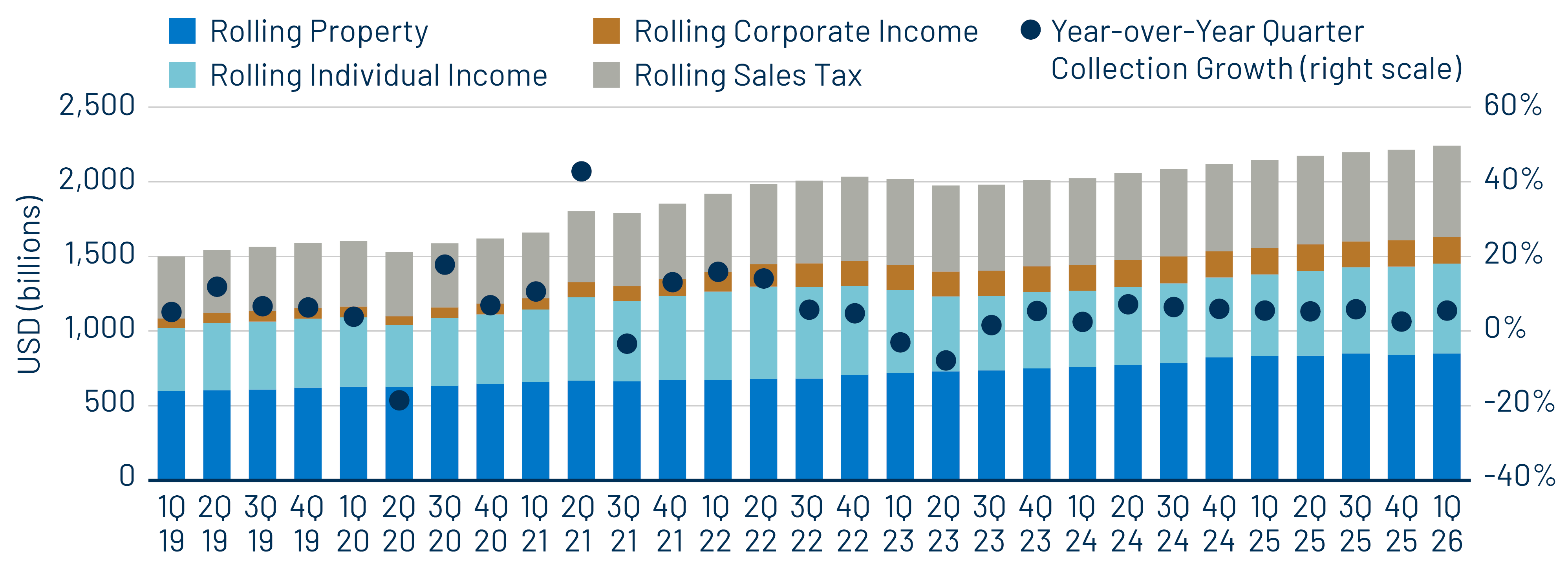

The municipal market navigated a budget season marked by reduced federal support and ongoing cost pressures. However, resilient economic growth and a healthy labor market continued to support record tax collections and broadly stable municipal credit fundamentals. The US Census Bureau’s 1Q26 state and local tax collection estimates showed total collections rising 5.5% YoY on a trailing 12-month basis to a record $2.22 trillion. Individual income taxes were the primary growth driver, increasing 10.0% YoY. Sales tax collections rose 3.8%, property tax collections increased 2.1% and corporate income tax collections grew more modestly, rising 0.8%.

While credit fundamentals remain strong across most of the municipal market, rating actions have begun to reflect moderate growth expectations and persistent cost pressures. As a result, the pace of rating improvement slowed in 1H26. According to Bloomberg data through June 18, upgrades from the three major rating agencies (Moody’s, S&P and Fitch) continued to outnumber downgrades by issuer count, with 540 upgrades versus 509 downgrades. However, downgrades exceeded upgrades by par value, with $101 billion downgraded versus $88 billion upgraded. Meanwhile, first-time payment defaults totaled $692 million, below the $1 billion recorded during the prior-year period.

Valuations

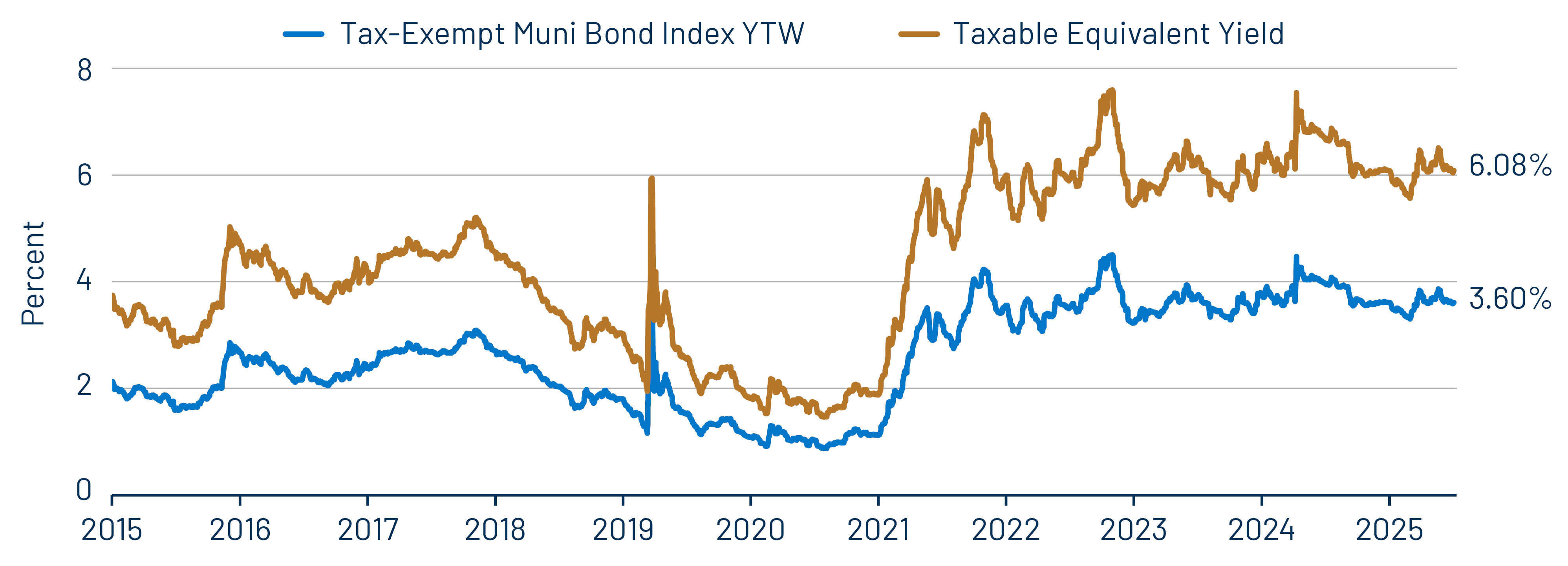

Despite strong nominal and relative returns so far this year, Western Asset believes value persists in the municipal market. The average yield-to-worst of the Bloomberg Municipal Bond Index ended June at 3.6%, roughly in line with the start of the year and equivalent to a tax-equivalent yield of approximately 6.0%, assuming a top marginal tax rate of 40.8%. Relative after-tax income opportunities remain favorable out the yield curve and across lower investment-grade to high-yield credit. We believe these opportunities remain compelling in an environment where equity valuations appear elevated and corporate credit spreads remain tight. However, recent outperformance has narrowed broad relative value, underscoring the importance of security selection within the market.

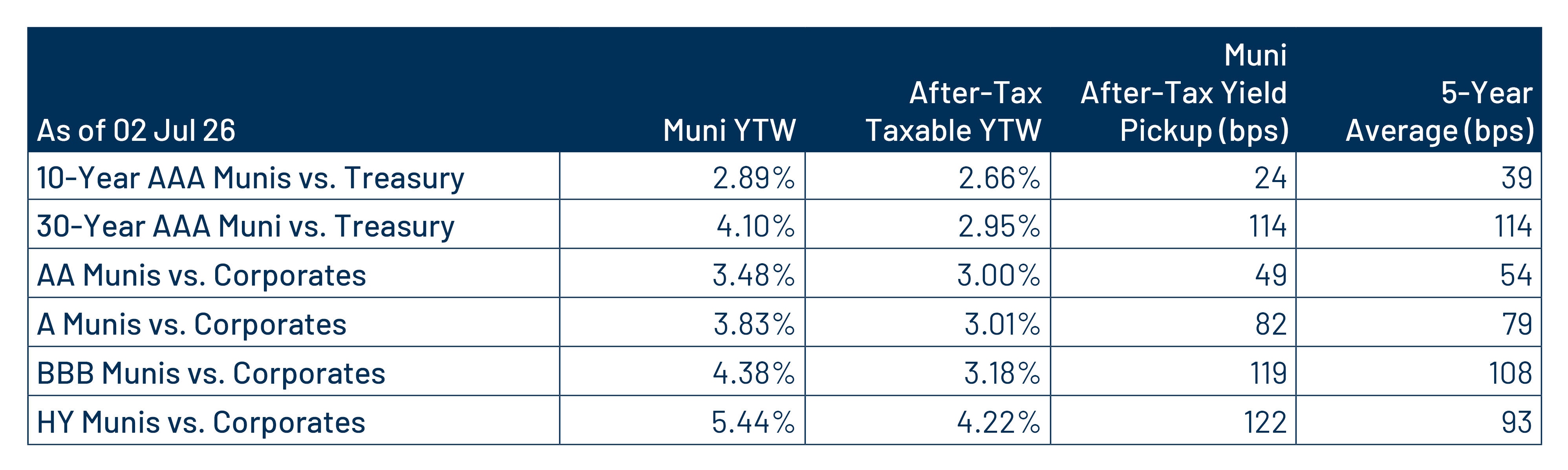

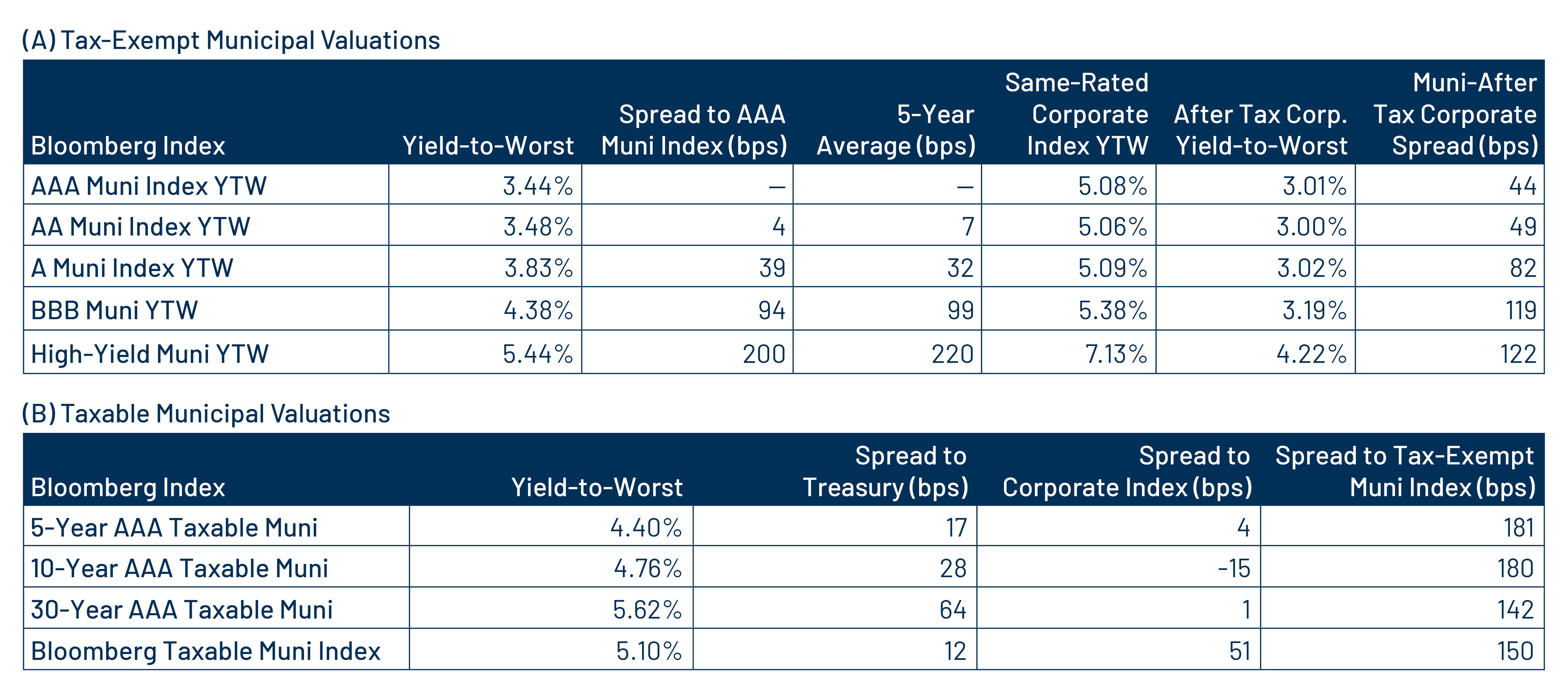

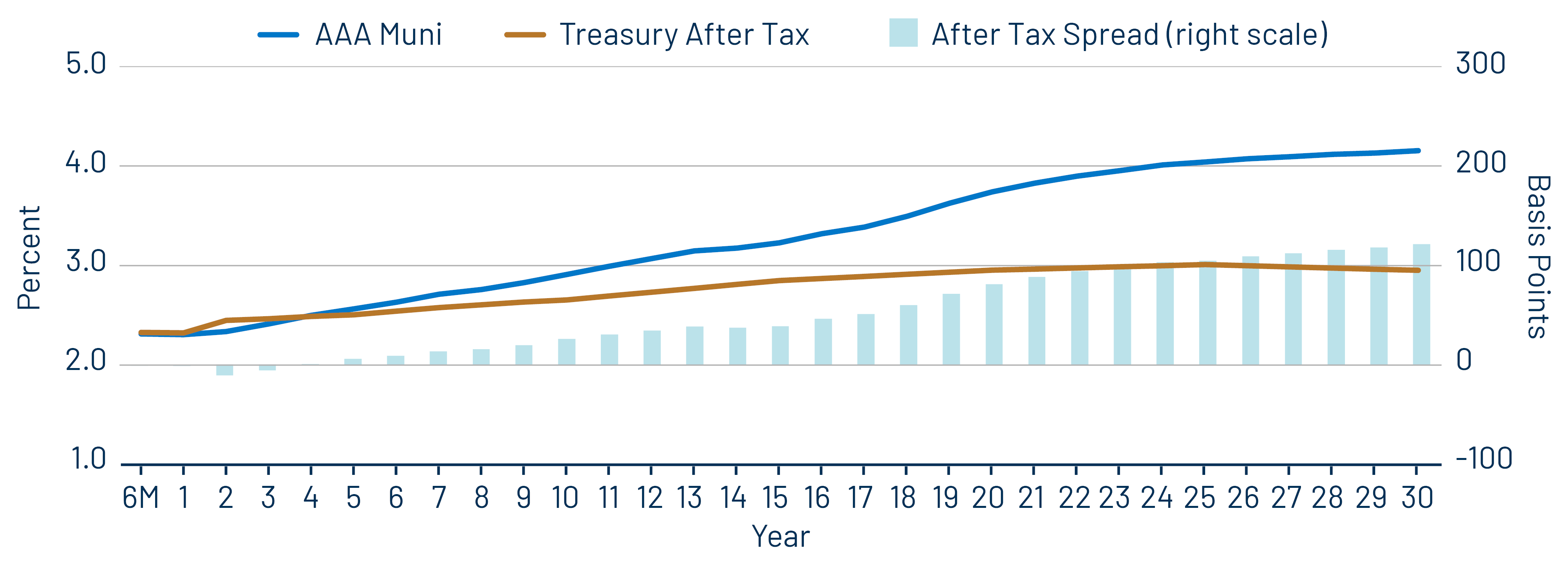

Municipal Credit Curves and Relative Value

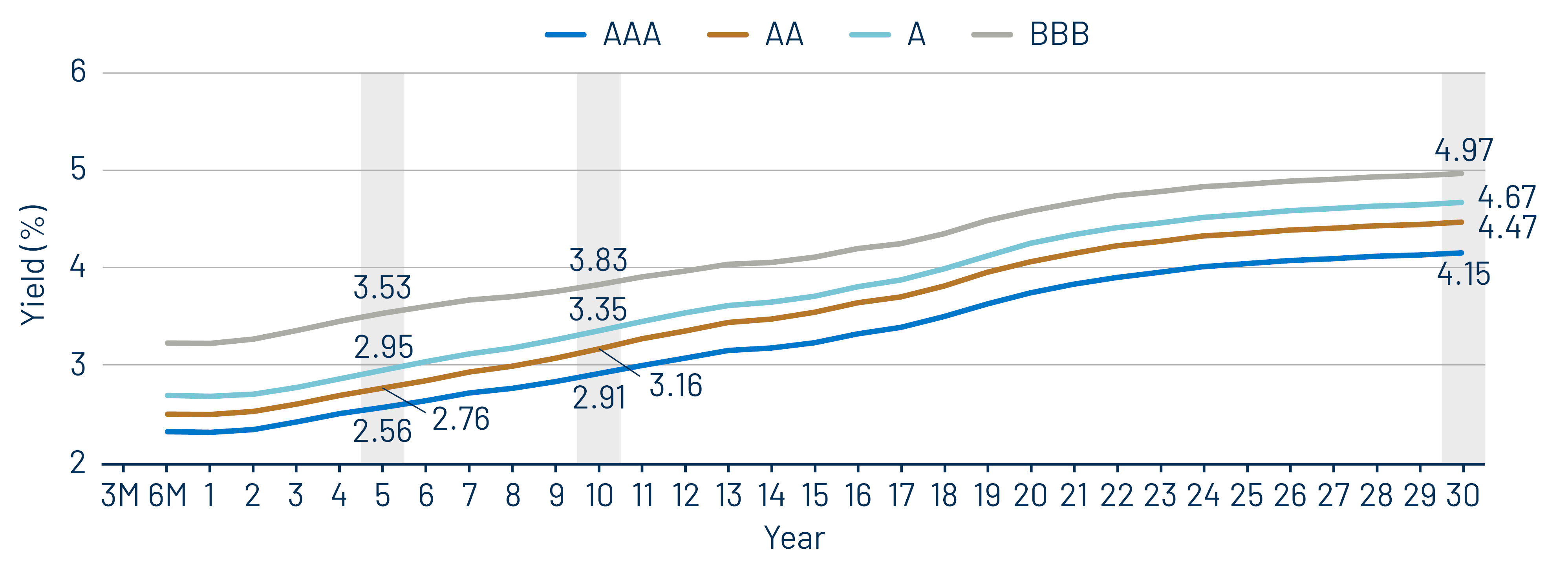

Theme 1: Municipal taxable-equivalent yields remain elevated relative to historical averages.

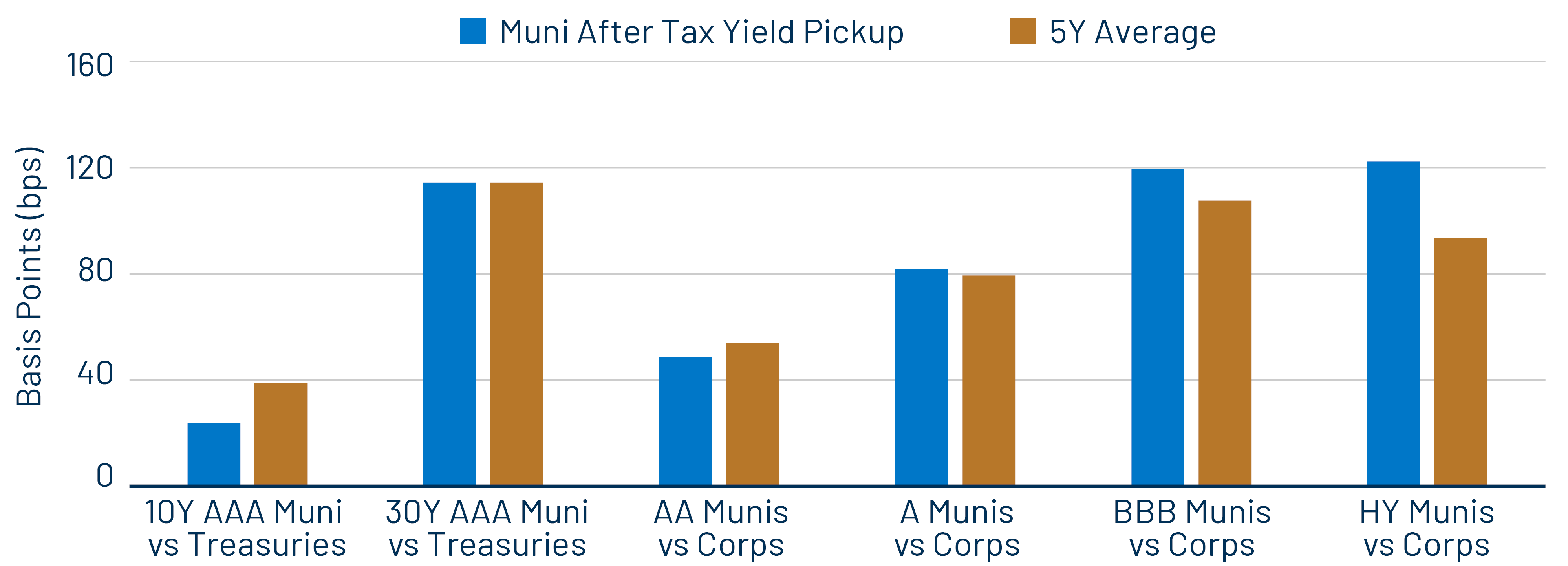

Theme 2: Munis offer attractive after-tax yield pickup vs. longer-duration or lower-quality taxable alternatives.

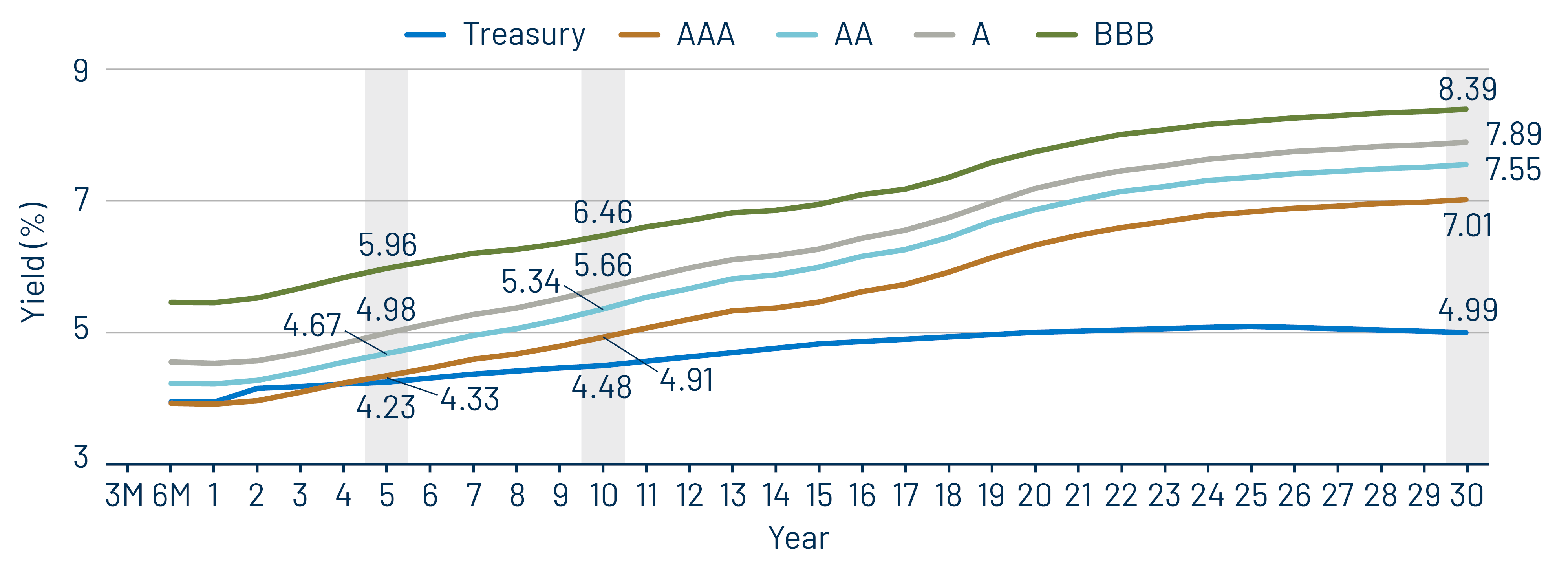

Theme 3: The muni curve remains steep and offers relative value in longer maturities.