Macros, Markets and Munis

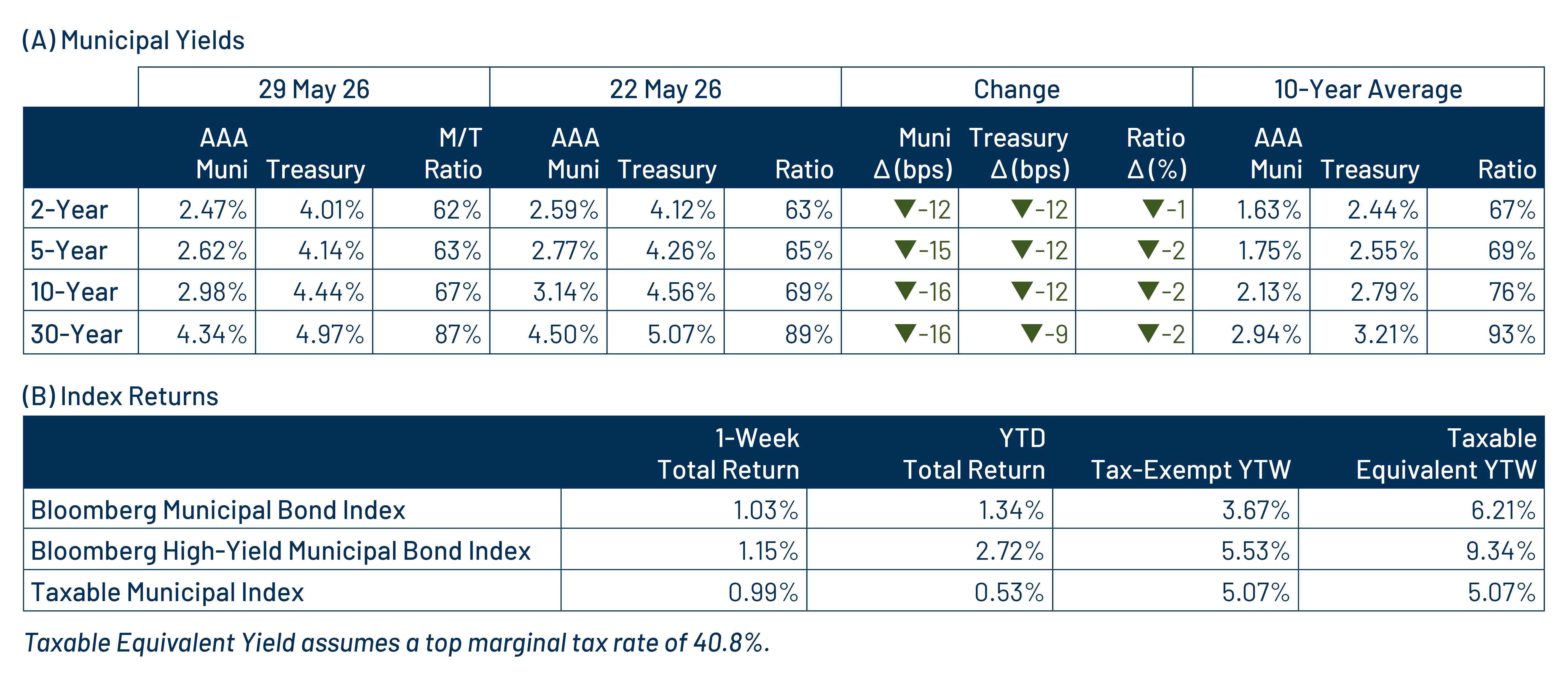

Municipals rallied across the yield curve last week and outperformed Treasuries as muni demand remained strong against lighter supply conditions during the holiday-shortened week. Markets turned constructive on prospects of a de-escalation in the US-Iran conflict and tempered inflation trends, as April core Personal Consumption Expenditures (PCE) came in softer than expected at +0.2% month-over-month (MoM) versus the +0.3% consensus. Treasury yields fell 9 to 12 basis points (bps) across the curve, while muni yields fell 12 to 16 bps. This week we provide a muni market update for the month of May.

Demand Reached Near-Record Levels Amid Lighter Supply Conditions

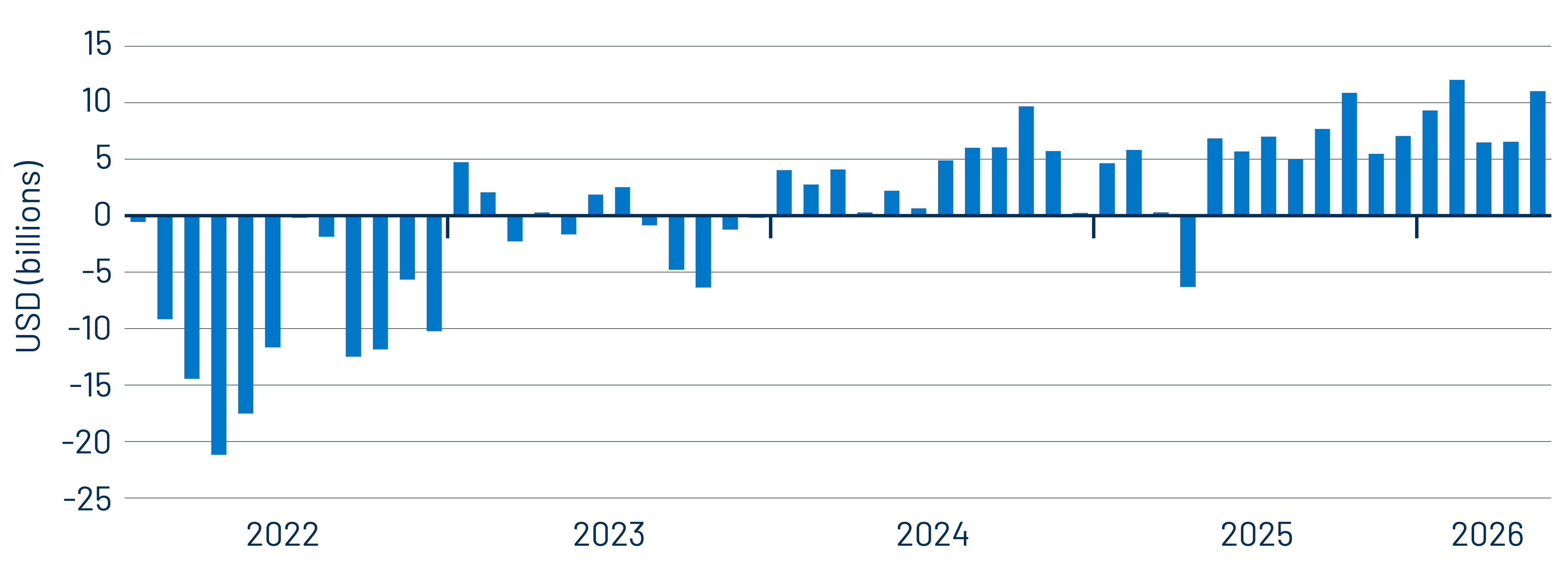

Fund Flows ($2.3 billion of net inflows): During the week ending May 27, weekly reporting municipal mutual funds recorded $2.3 billion of net inflows, according to Lipper, representing the second highest week on record. The long-term category recorded $1.6 billion of inflows, the intermediate category reported $551 million of inflows and the short-term category recorded $116 million of inflows. Last week’s inflows bring year-to-date (YTD) inflows to $40 billion.

Supply (YTD supply of $238 billion; up 14% YoY): The muni market recorded $10 billion of new-issue supply last week, down 40% from the prior week due to the holiday. YTD new-issue supply of $238 billion is 14% higher than the prior year, with tax-exempt issuance up 14% year-over-year (YoY) and taxable issuance up 7%, respectively. This week’s calendar is expected to pick up to an elevated $19 billion. Largest deals include $1.8 billion University of California and $823 million Harris County Hospital transactions.

This Week in Munis: May Monthly Review

Performance

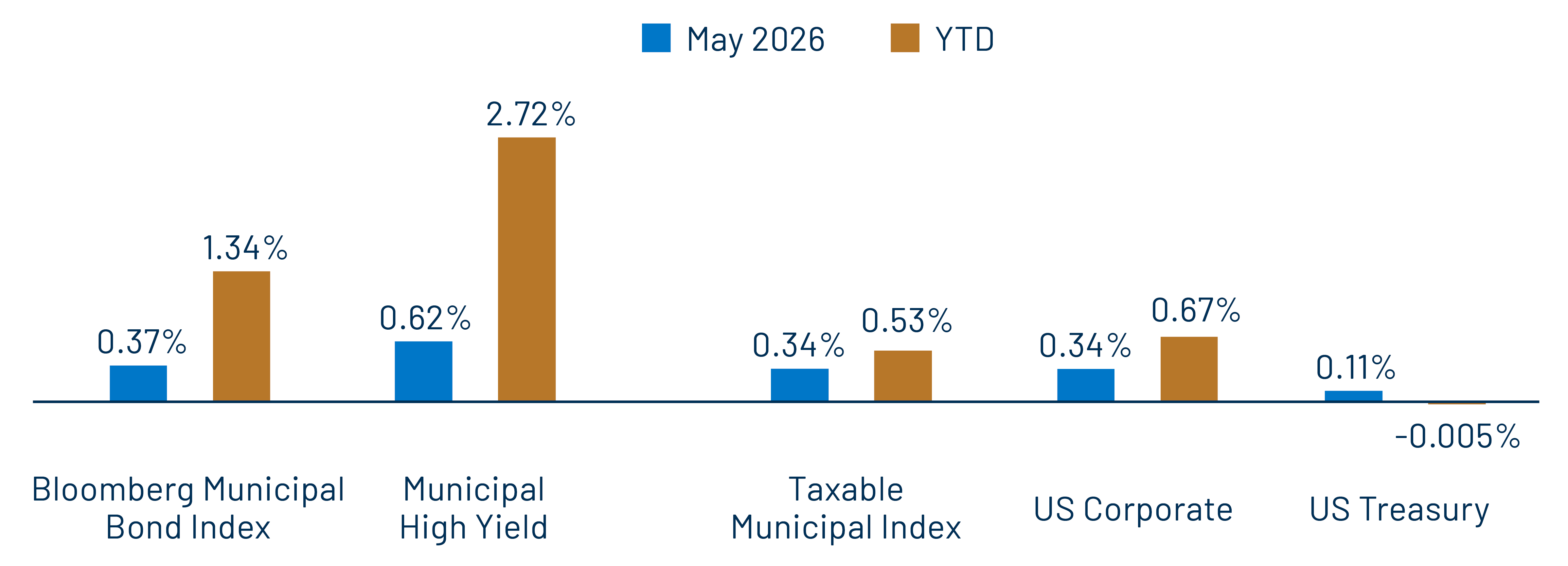

Fixed-income markets posted positive returns during a volatile May. Yields moved higher through most of the month as investors contended with persistent inflation uncertainty. Markets rebounded into month-end amid increased optimism for the end of the US-Iran conflict and as core PCE surprised to the downside. All told, the Treasury curve flattened over the month, with yields rising by up to 16 bps in shorter maturities, as markets repriced policy expectations to reflect a greater probability of hikes rather than cuts. The municipal curve also flattened, though high-grade municipal yields moved lower by up to 6 bps in longer maturities, contributing to outperformance in longer-duration municipals during the month.

Technicals

Municipal technicals remained characterized by elevated supply and demand. May total new issuance was elevated at $52 billion, slightly above prior-month levels. Notably tax-exempt municipal supply of $49 billion represented 95% of total issuance and increased 10% from the prior-month levels. Demand remained firm, with municipal mutual funds recording approximately $10 billion of net inflows during the month, according to Lipper as of May 27, rebounding from the recent tax season softness. Long-term funds and ETFs garnered the majority of net inflows during the month and led total YTD inflows higher to $40 billion.

Fundamentals

Municipal credit fundamentals remain strong, supported by robust revenue collections and healthy cash balances. However, municipalities continue to navigate a post-pandemic environment marked by reduced federal aid and inflationary pressures, which have contributed to more prolonged budgetary processes. This dynamic has been evident in the State of New York, which typically leads the municipal budget calendar. Despite a delay of nearly two months, the state ultimately passed its budget without including increases in income taxes at the state or city level. This was followed by New York City moderating spending expectations as its budget process continues. Western Asset believes these types of compromises are characteristic of typical budget cycles and underscore the flexibility of municipal issuers to manage through a late-cycle economic environment.

Valuations/Outlook

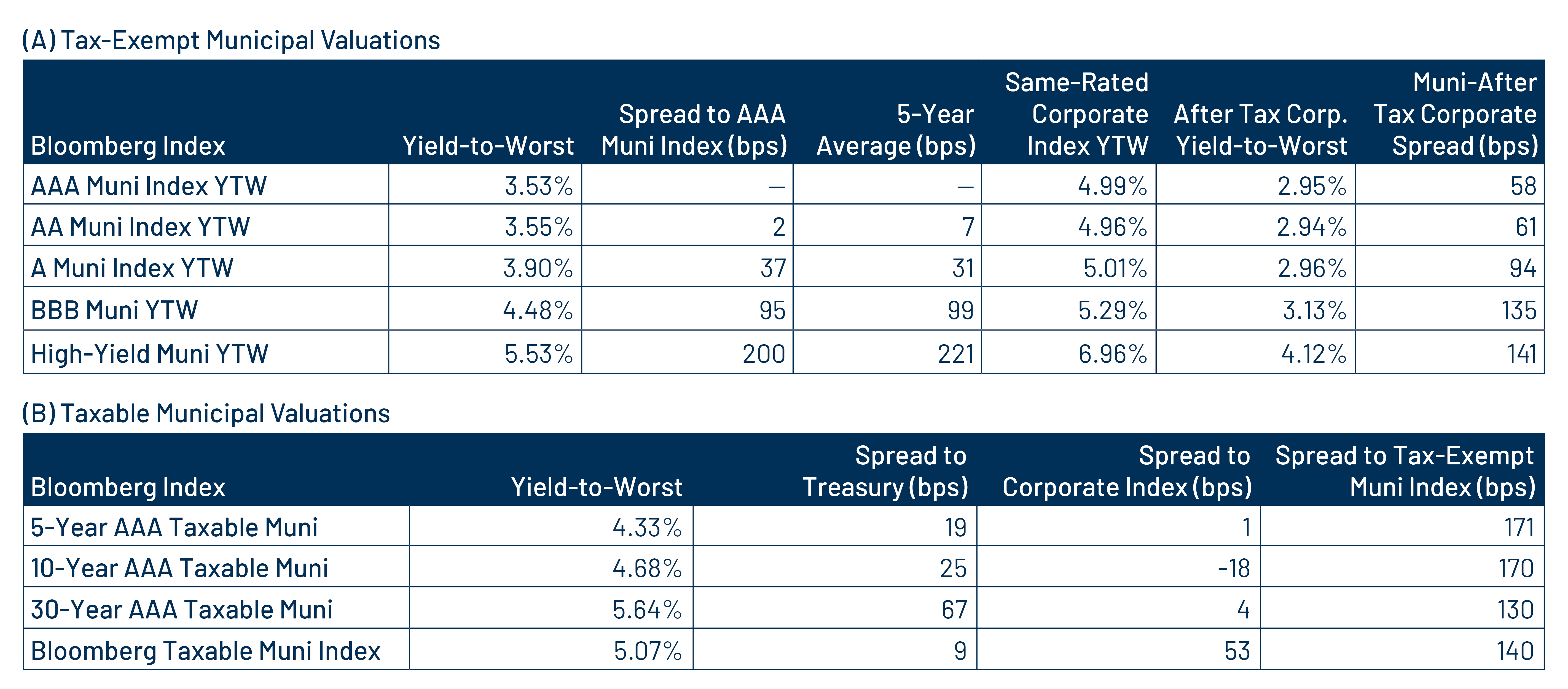

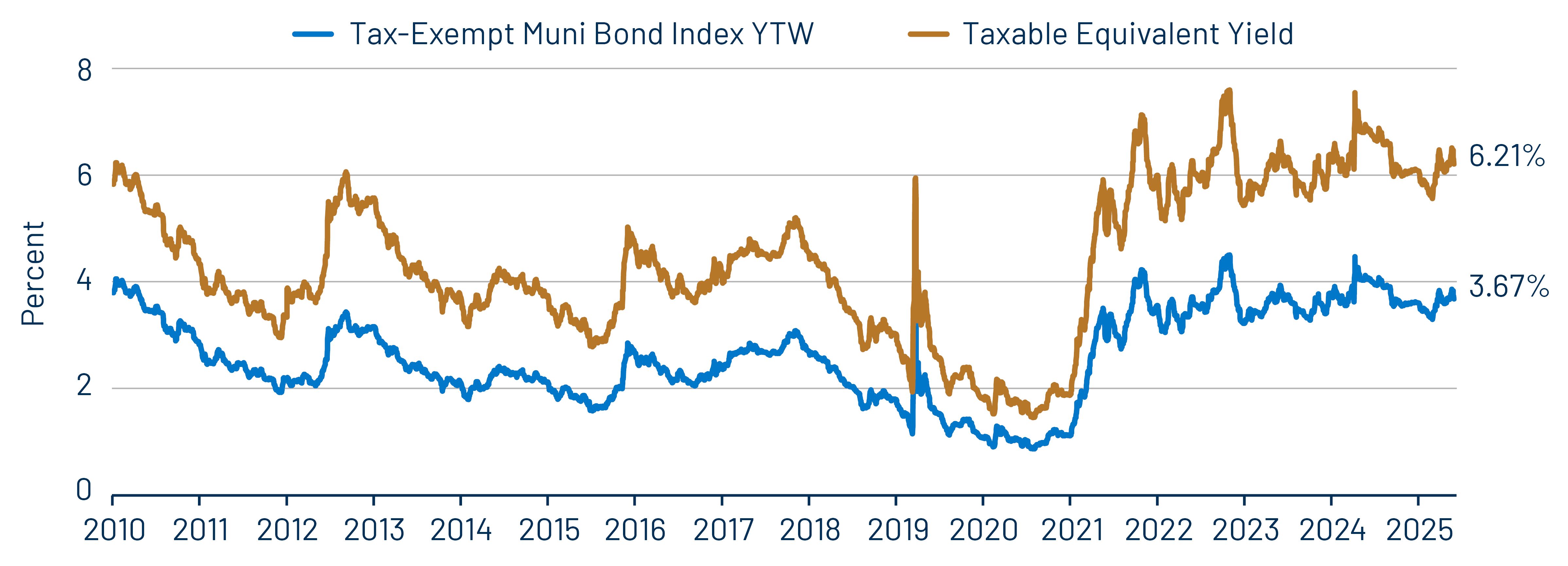

Despite recent outperformance, Western Asset believes the municipal market continues to offer attractive after-tax income opportunities. The Bloomberg Municipal Bond Index yield-to-worst stands at approximately 3.7%, or about 6.2% on a taxable-equivalent basis, remaining above levels observed at the start of the year. While nominal credit spreads remain tight relative to historical averages, for high-tax investors, municipal credit continues to provide compelling after-tax relative value compared to similarly rated taxable fixed-income securities. Looking ahead, seasonal technicals are expected to remain supportive, and the potential for lighter supply conditions alongside elevated summer reinvestment demand could compound the strong fund flow trend observed in recent months and reinforce the asset class’s value proposition.

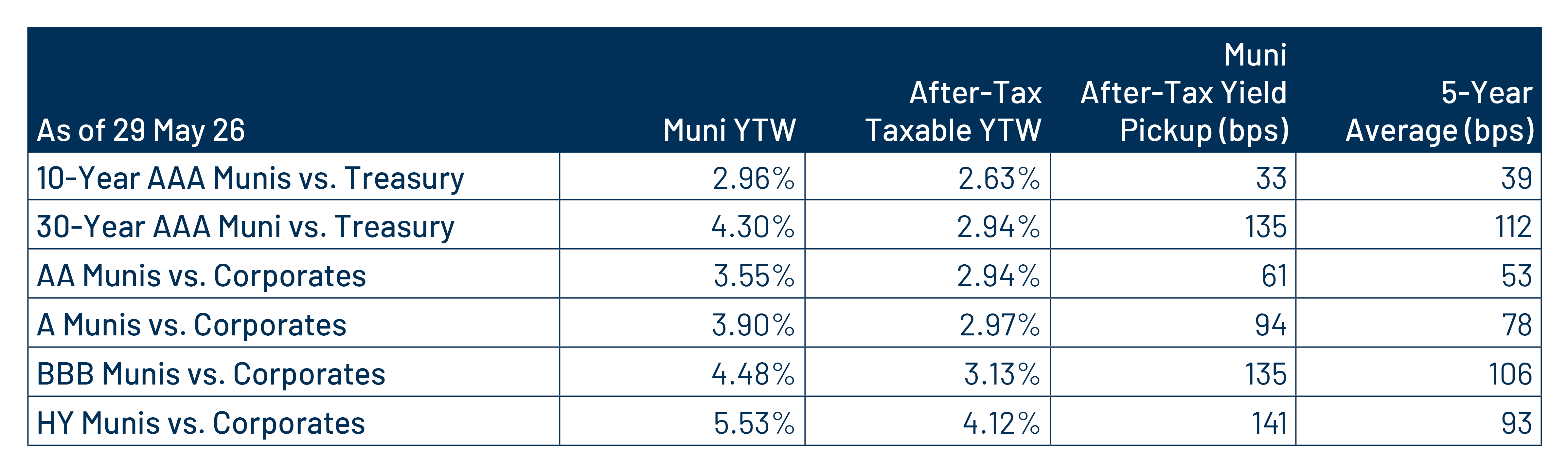

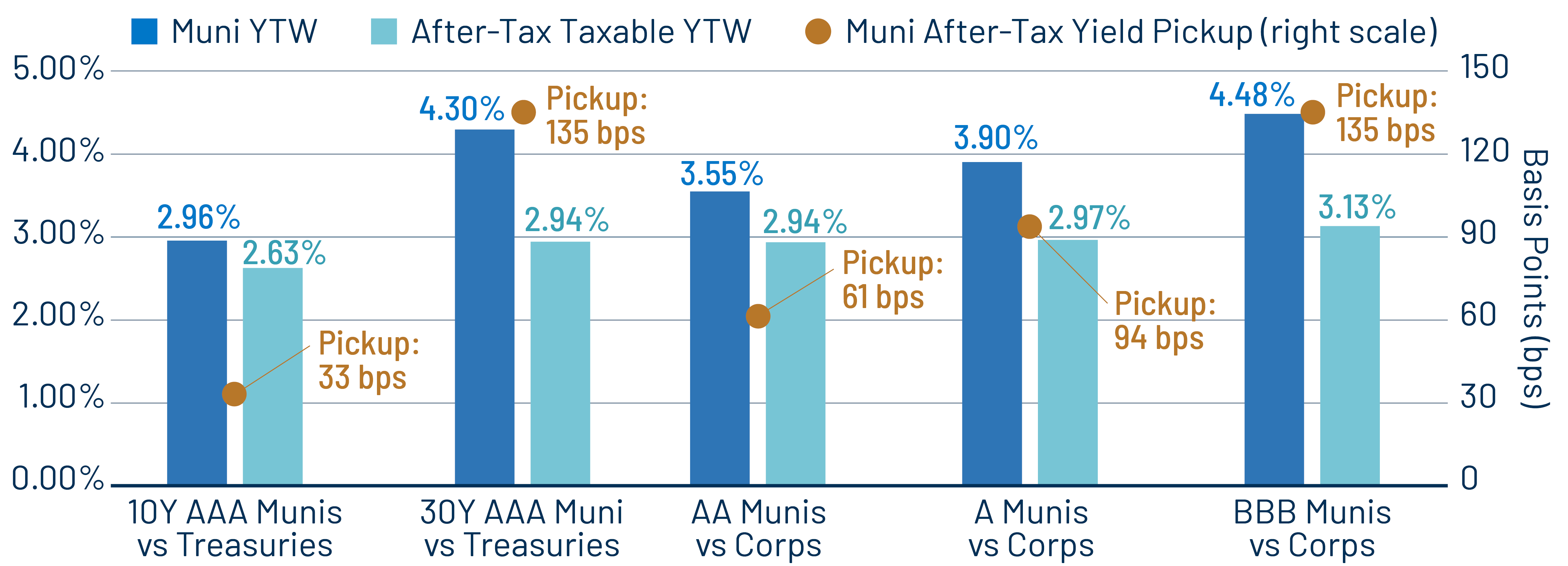

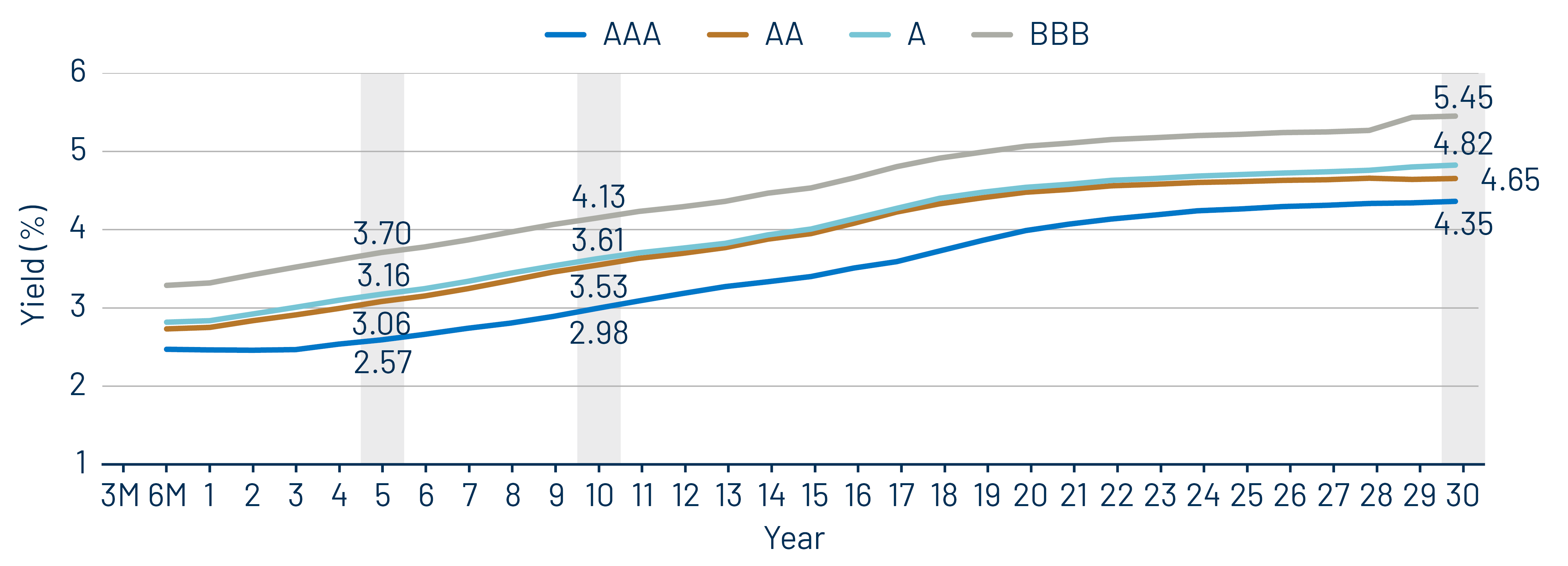

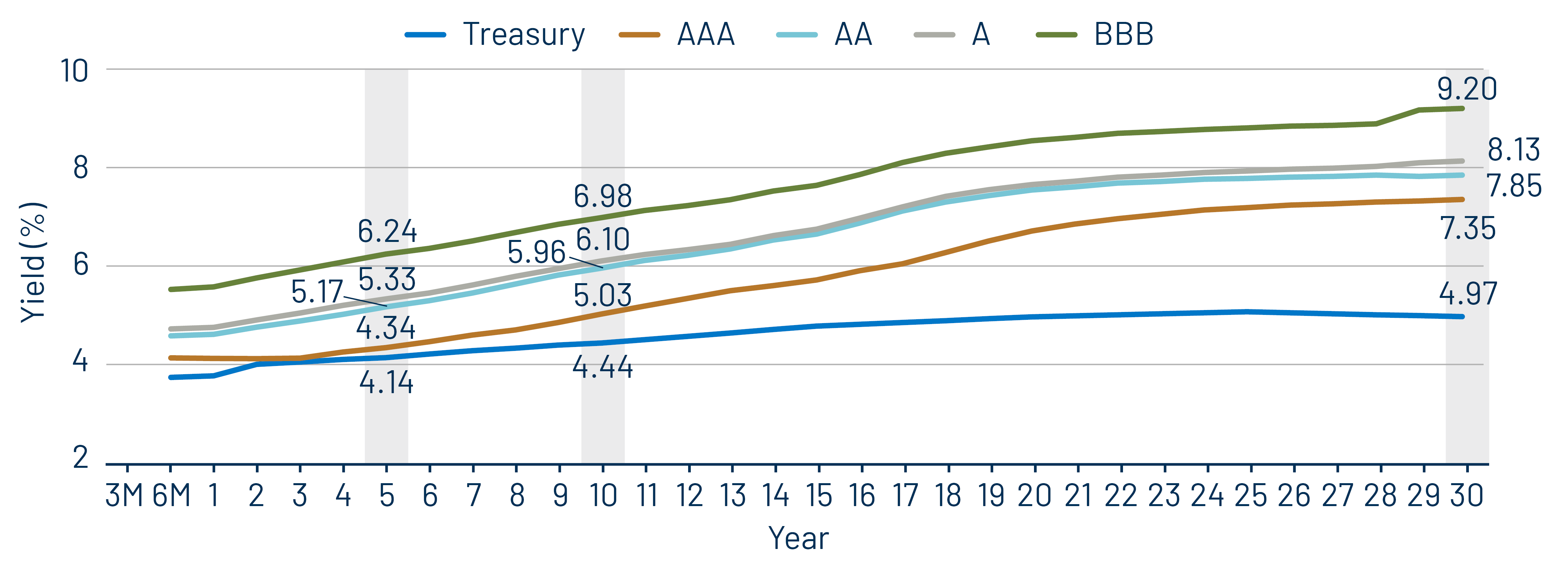

Municipal Credit Curves and Relative Value

Theme 1: Municipal taxable-equivalent yields moved lower from recent highs, but remain above historical averages.

Theme 2: Munis offer attractive after-tax yield pickup vs. longer-duration and lower-quality taxable alternatives.

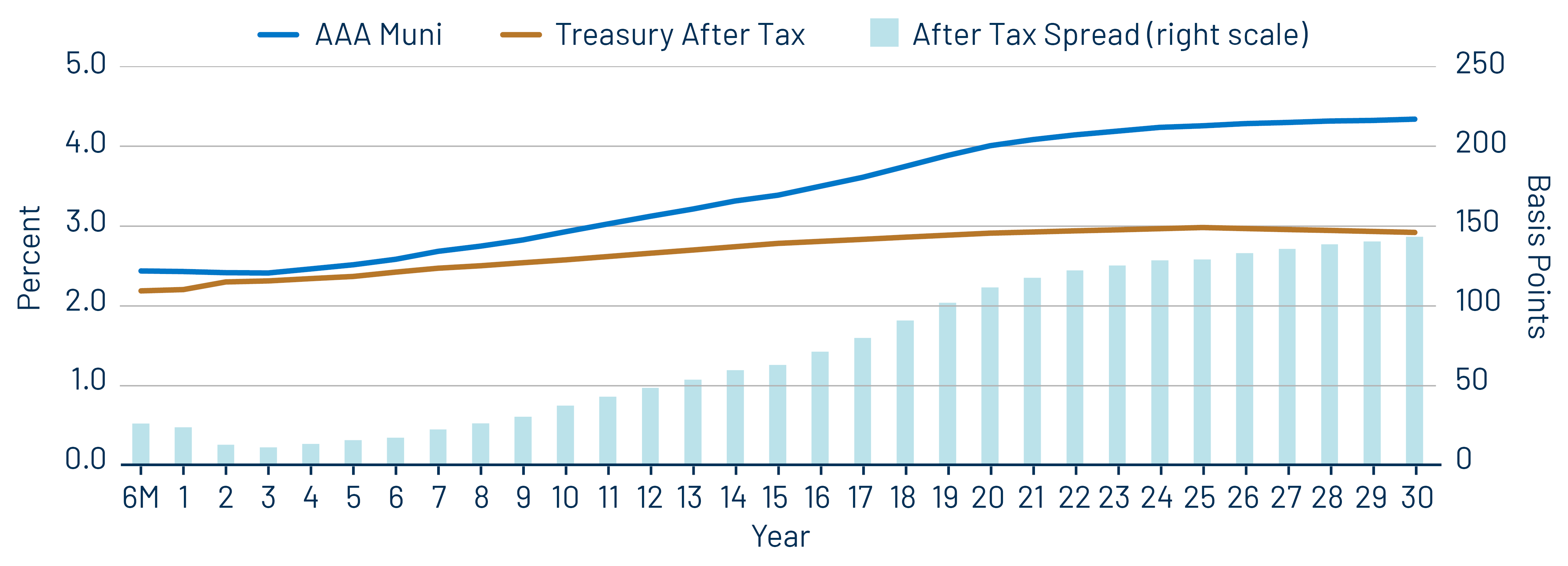

Theme 3: The muni curve remains steep and offers relative value in longer maturities.