Macros, markets and munis

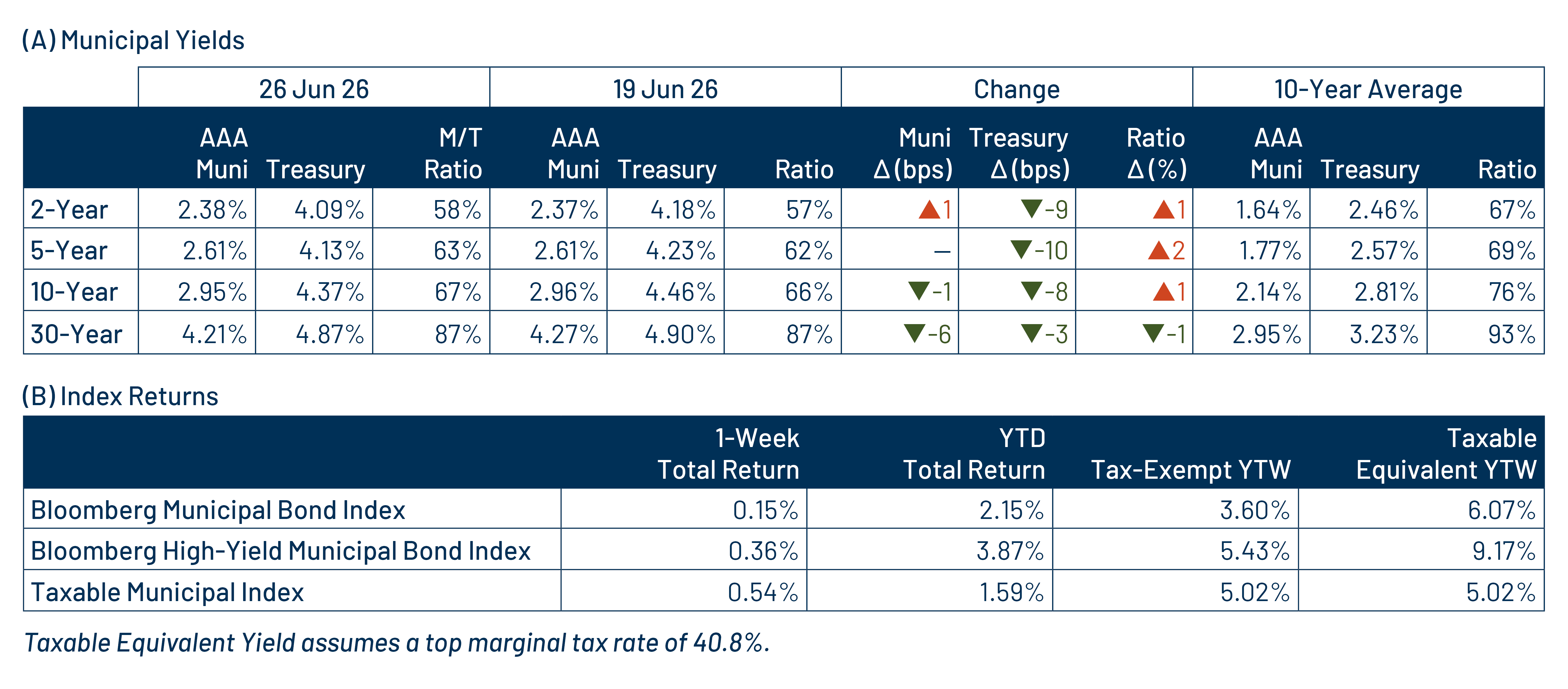

Municipals posted positive returns last week but underperformed Treasuries, particularly in shorter and intermediate maturities, as markets remained focused on the US-Iran conflict and the status of the Strait of Hormuz. Oil prices continued to decline, falling to $72 per barrel, easing some inflationary concerns. From an economic data standpoint, May core Personal Consumption Expenditures (PCE) was largely aligned with prior-month levels and expectations, while personal income and spending data exceeded prior-month levels and market consensus. The Treasury yield curve rallied with a steepening bias, moving approximately 8 to 10 basis points (bps) lower in shorter maturities and 3 bps lower in longer maturities. The timing of rate hike expectations has now moved from September to December. Meanwhile, muni demand remained positive amid elevated supply conditions. This week we highlight the evolving debt ownership trends in the municipal market.

Steady demand absorbed elevated supply

Fund Flows ($633 million of net inflows): During the week ending June 24, weekly reporting municipal mutual funds recorded $633 million of net inflows, marking the 10th consecutive week of inflows, according to Lipper. The short-term category led demand with $416 million of inflows, the long-term category recorded $74 million of inflows and the intermediate category reported $92 million of inflows. Last week’s inflows bring year-to-date (YTD) inflows to $50 billion.

Supply (YTD supply of $300 billion; up 13% YoY): The muni market recorded $15 billion of new-issue supply last week, up 50% from the prior week’s level. YTD new-issue supply of $300 billion is 13% higher than the prior record-issuance year, with tax-exempt issuance up 13% year-over-year (YoY) and taxable issuance up 10% YoY, respectively. This week’s calendar is expected to drop to $5 billion, given the holiday-shortened week. The largest deals include $2.4 billion Aquarion Water Authority Water System Revenue and $920 million Black Belt Energy Gas District transactions.

This week in munis: Holders of muni debt

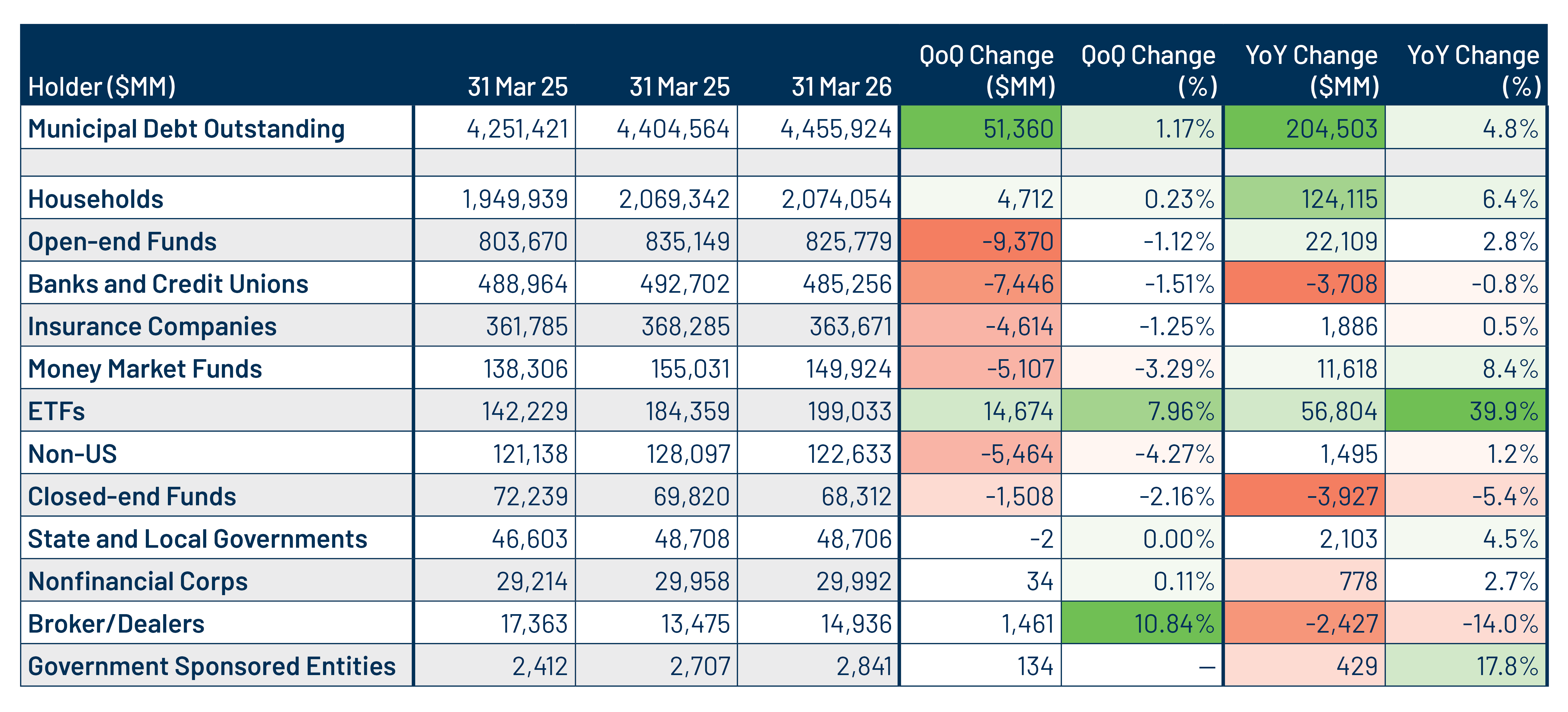

This month, the Federal Reserve released updated Flow of Funds data highlighting the primary holders of municipal debt through the first quarter of 2026. According to the data, the size of the municipal market increased by $51 billion, or 1%, during the first quarter and by $205 billion, or 5%, over the past 12 months, consistent with the positive net supply trends observed over the past year.

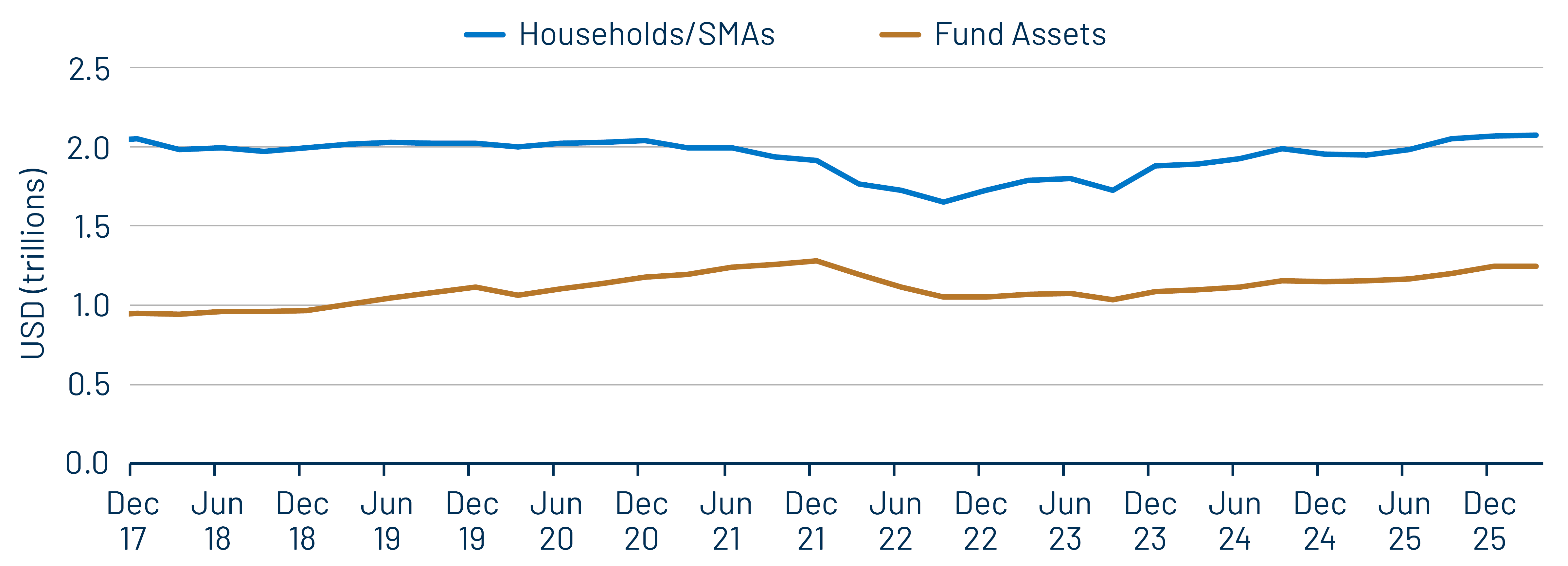

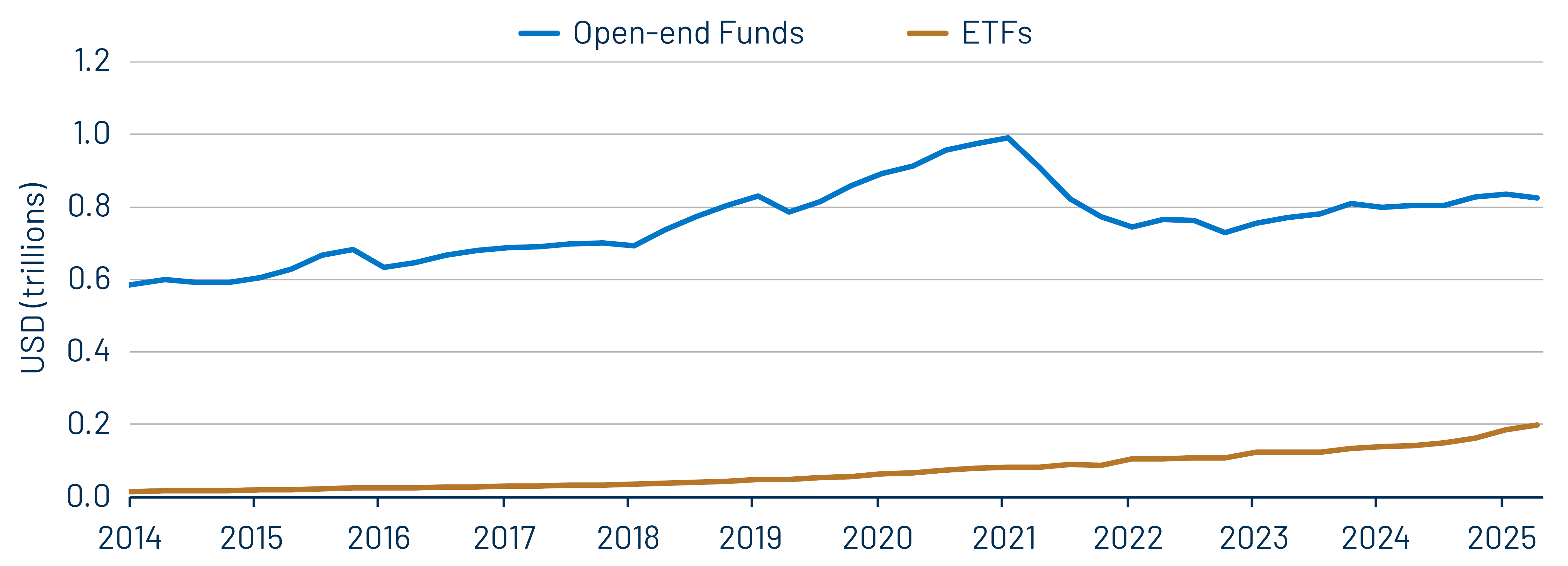

The market continued to trend away from traditional open-end funds and toward ETFs and SMAs. Municipal ETF holdings increased by $15 billion, or 8%, during the first quarter, while individual household holdings rose by $5 billion, or 0.2%. By contrast, open-end fund holdings declined by $9 billion, or 1%, during the quarter. Over the past year, municipal ETF assets increased by $57 billion, or 40%, to $199 billion, while household/SMA assets rose by $124 billion, or 6%. Traditional fund assets increased just 3%, reaching $825 billion.

The holdings data also continues to point to a shift away from institutional investors, a trend that has persisted since 2018, when corporate tax rates were lowered to 21%. Institutional municipal holdings declined by $18 billion, or 2%, during the quarter, led by reductions among banks, insurance companies and non-US municipal holders. Bank holdings declined by $7 billion, or 2%, insurance company holdings fell by $5 billion, or 1%, and non-US municipal holdings declined by $5 billion, or 4%, during the first quarter.

As institutional investors continue to step away from munis, the market has become increasingly concentrated within the individual retail buyer base. We expect that strong demand from SMAs and ETFs has created unique relative value considerations, as these vehicles historically have operated within investment guidelines that can concentrate demand in certain market segments. A more concentrated retail-driven market can also contribute to heightened bouts of volatility. We expect these dynamics to present ongoing opportunities for active managers to provide favorable tax-efficient outcomes.

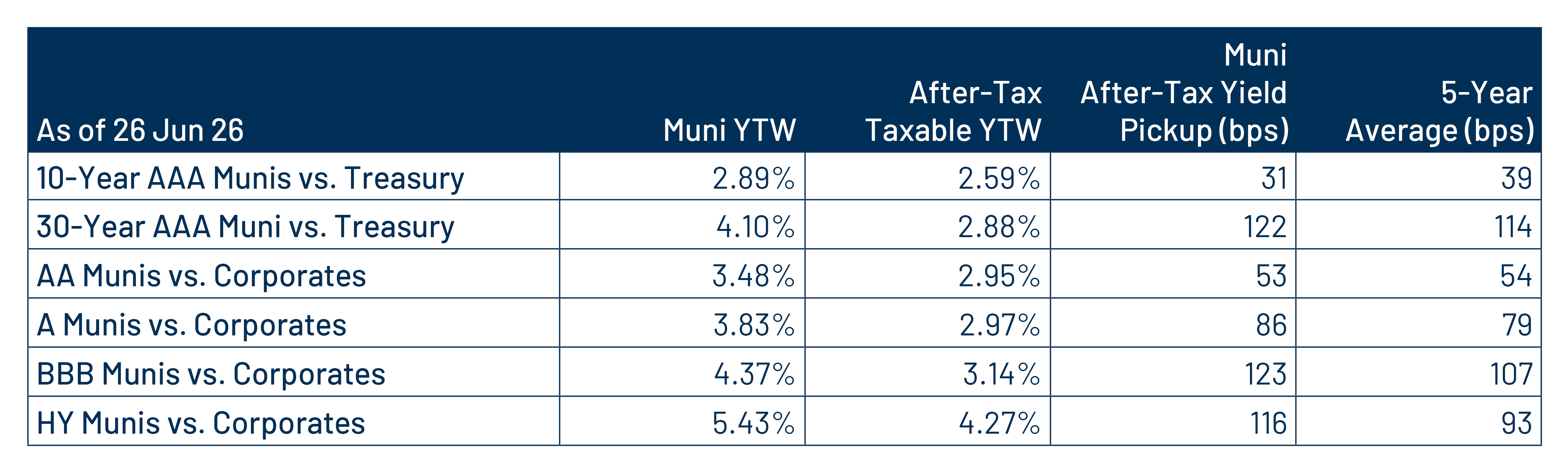

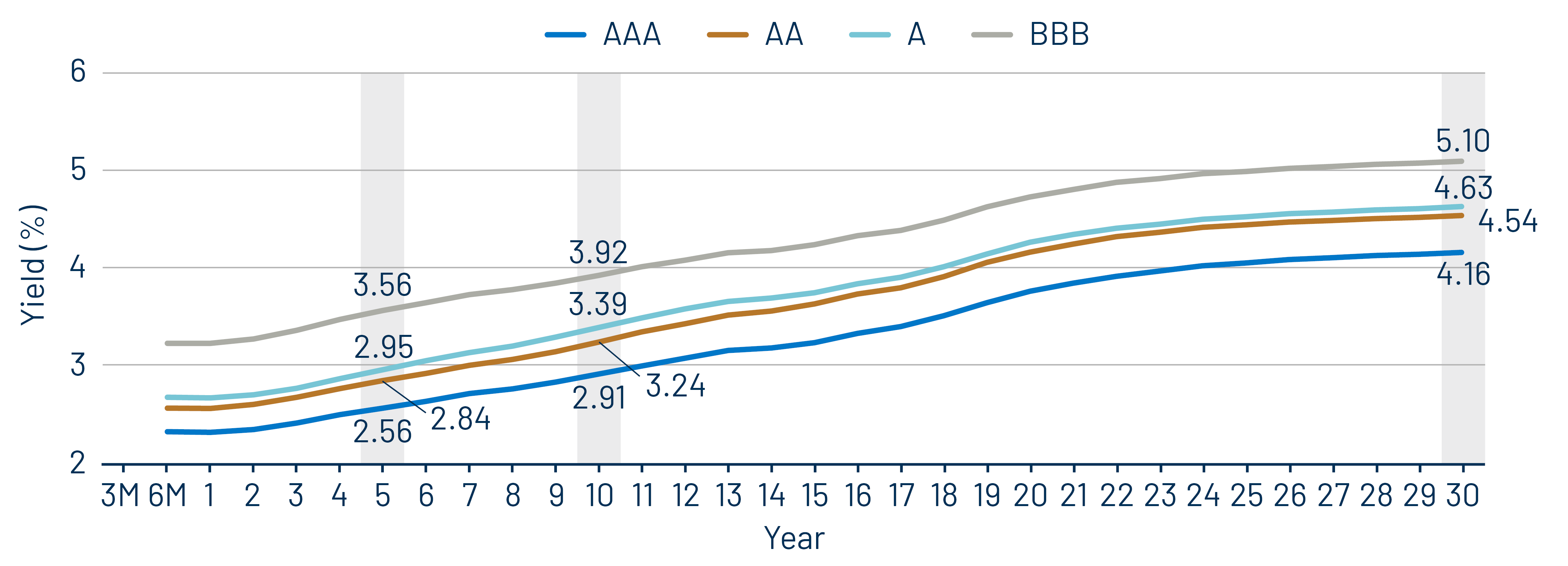

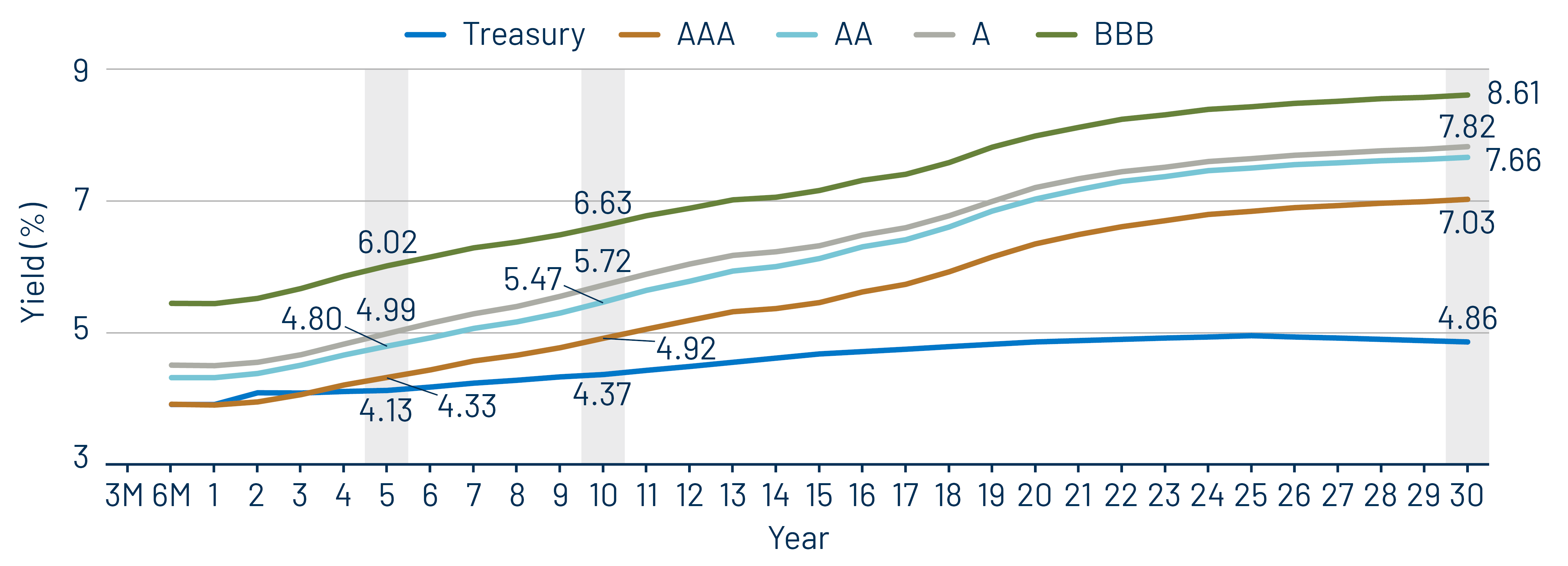

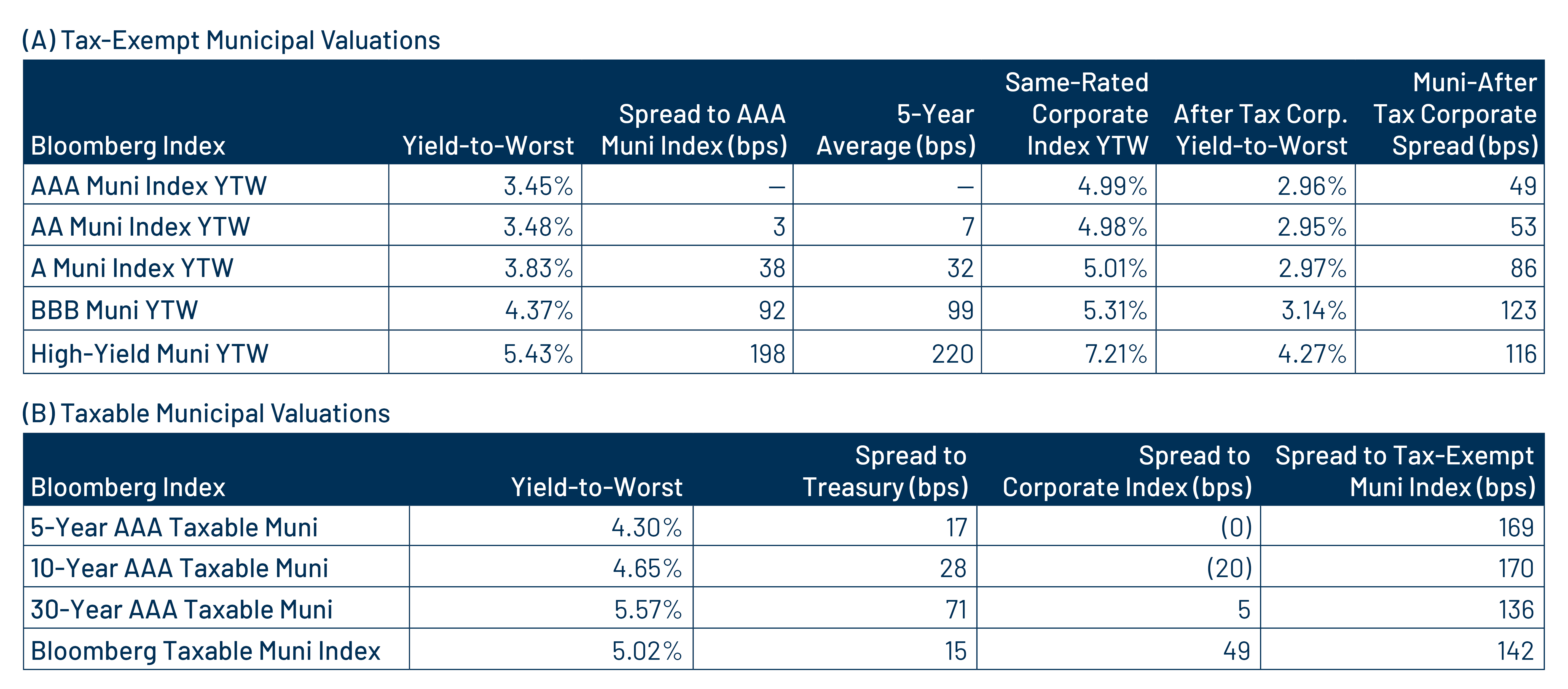

Municipal Credit Curves and Relative Value

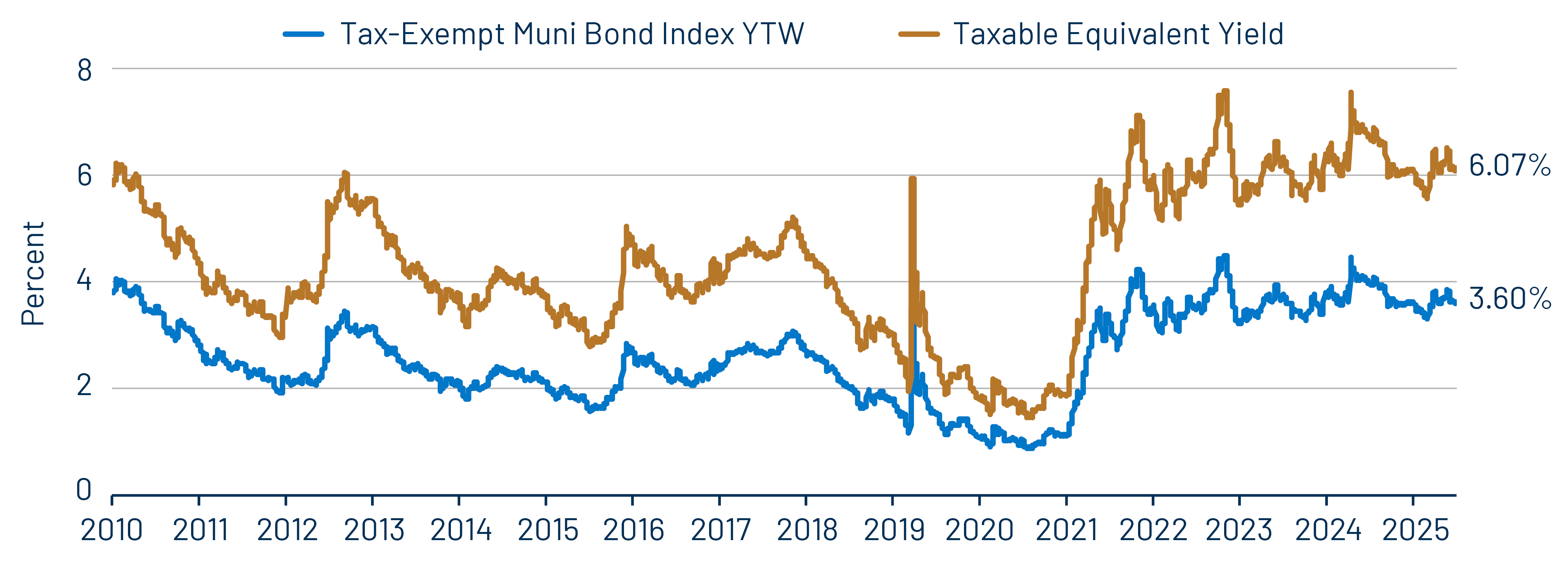

Theme 1: Municipal taxable-equivalent yields remain elevated relative to historical averages.

Theme 2: Munis offer attractive after-tax yield pickup vs. longer-duration or lower-quality taxable alternatives.

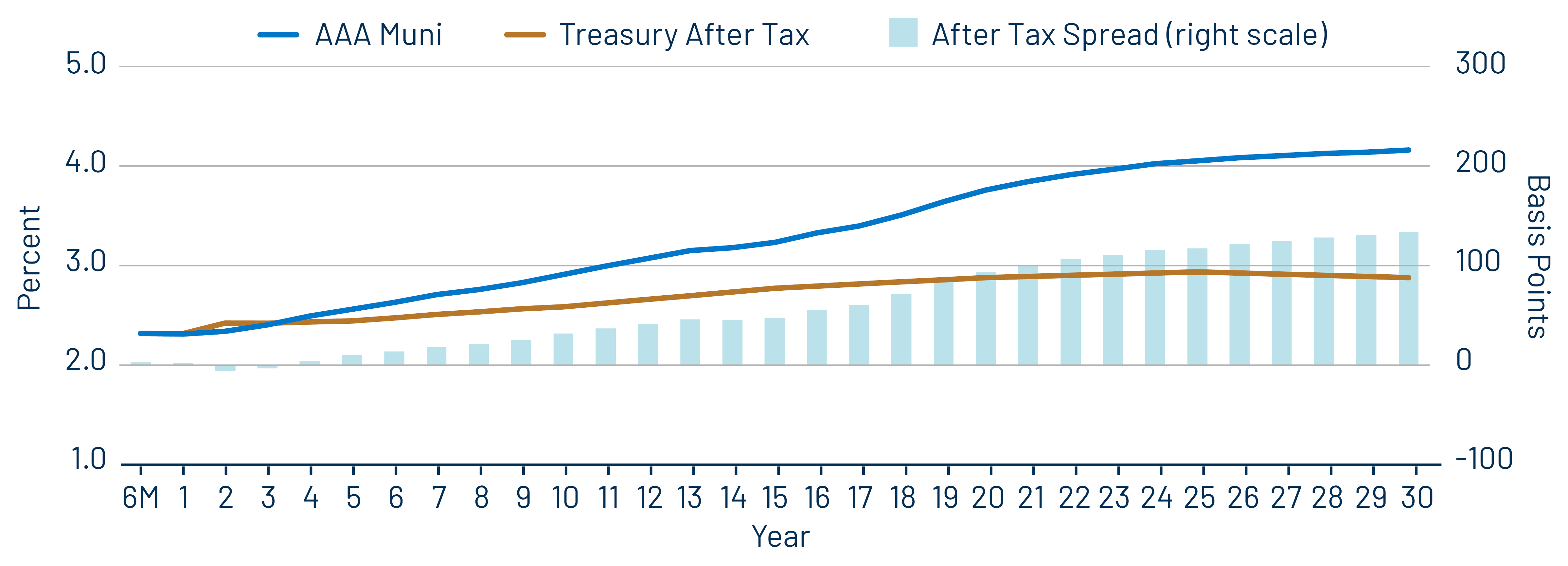

Theme 3: The muni curve remains steep and offers relative value in longer maturities.