Macros, Markets and Munis

Municipals posted negative returns last week and underperformed Treasuries amid optimism for an end to the US-Iran conflict re-emerging as high-level negotiations continued and oil prices declined. Economic data released last week was mixed: The May Consumer Price Index (CPI) rose 4.2% year-over-year (YoY), in line with consensus expectations, marking the fastest annual inflation increase in more than three years. However, core CPI rose just 0.2% month-over-month, below the consensus forecast of 0.3%, and down from the prior month’s 0.4% gain. Meanwhile, the University of Michigan consumer sentiment improved and exceeded expectations. Municipals underperformed, catching up with the prior week rate weakness as heavy supply conditions persisted, and the Treasury curve declined 3 to 7 basis points (bps) across the curve, with a steepening bias as muni supply remained robust. Following the strong gas prepay issuance this month, we provide an update on the evolving sector, including the entry of Google parent Alphabet.

Demand Remained Strong Amid Elevated Supply Levels

Fund Flows ($625 million of net inflows): During the week ending June 10, weekly reporting municipal mutual funds recorded $625 million of net inflows, according to Lipper. The long-term category recorded $78 million of inflows, the intermediate category reported $175 million of inflows and the short category recorded $279 million of inflows. Last week’s inflows bring year-to-date (YTD) inflows to $48 billion.

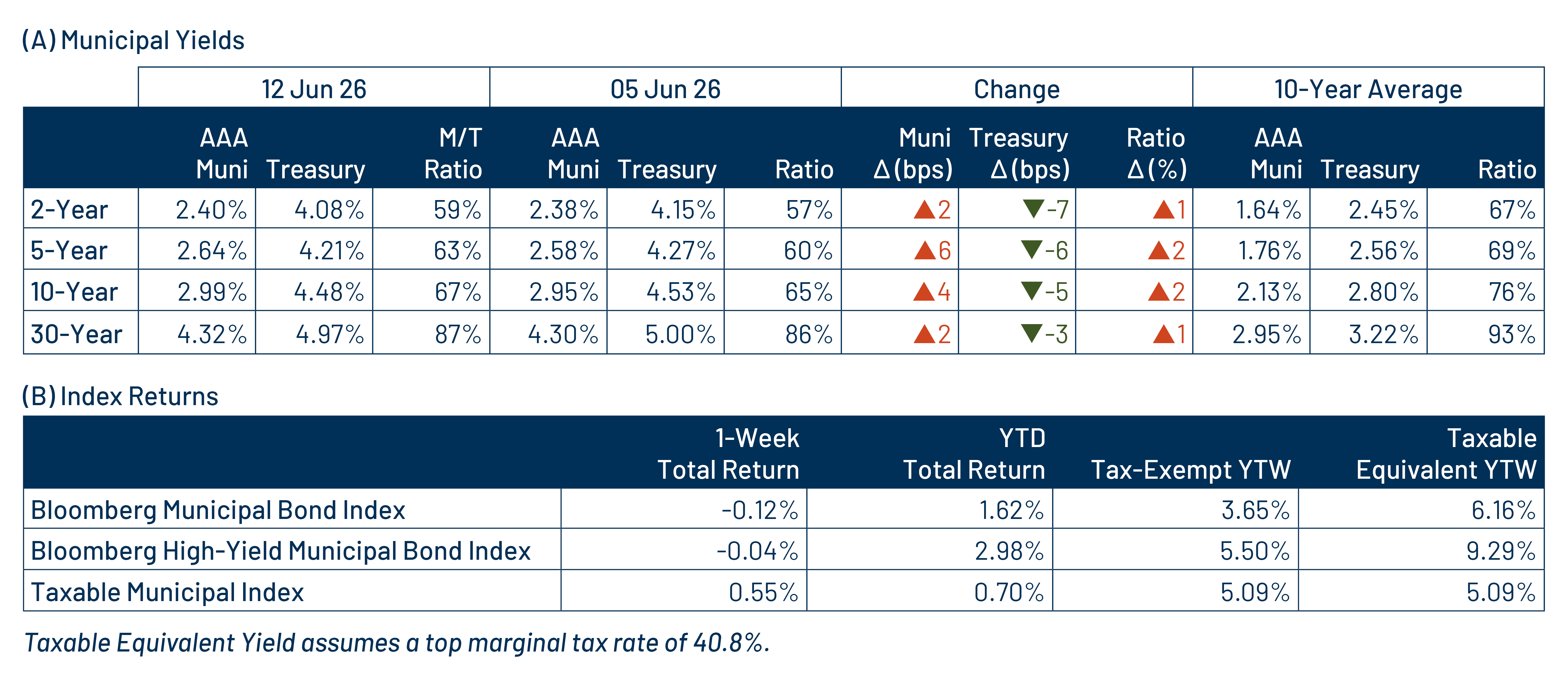

Supply (YTD supply of $274 billion; up 15% YoY): The muni market recorded $17 billion of new-issue supply last week, down from the prior week but remaining at very high levels. YTD new-issue supply of $274 billion is 15% higher than the prior record-issuance year, with tax-exempt issuance up 15% YoY and taxable issuance up 3%. This week’s calendar is expected to remain elevated at $13 billion. Largest deals include $2.5 billion State of Washington and $824 million Miami Dade County transactions.

This Week in Munis: Google Enters the Muni Market

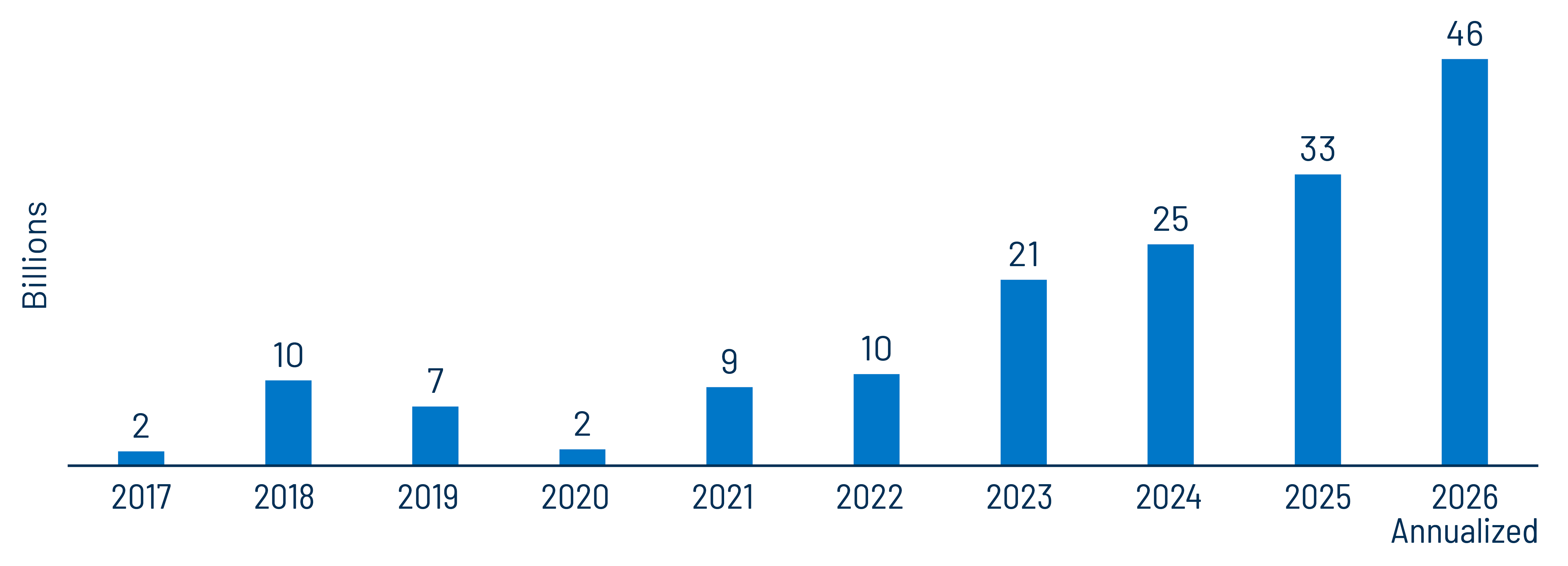

Earlier this year we highlighted the expansion of the gas/energy prepay market, the sector that allows municipal entities to finance longer-dated energy needs by structuring borrowing through a financial entity. The underlying credit exposure in these structures typically aligns with the financial institution providing credit support, while the economics are driven by the relative value advantage of tax-exempt financing versus taxable borrowing. This year’s gas prepay issuance has now reached $21 billion, on pace to reach $46 billion by year-end, supported by the two largest transactions priced last week: the $1.1 billion Black Belt Energy transaction backed by Bank of America and the $803 million Main Street Energy transaction backed by Bank of Nova Scotia.

The range of counterparties supporting prepay transactions continues to broaden. This month, the market expanded beyond its traditional reliance on financial institutions to the technology sector. On June 1, Google parent Alphabet supported a $1.2 billion financing structure designed to prepay for electricity in partnership with a public power provider. By backing the transaction, Alphabet gains access to the municipal market's low-cost financing, particularly in California where interest income benefits from state tax exemption. In return, the energy provider receives long-term discounts on power procurement, with resulting savings passed through to ratepayers.

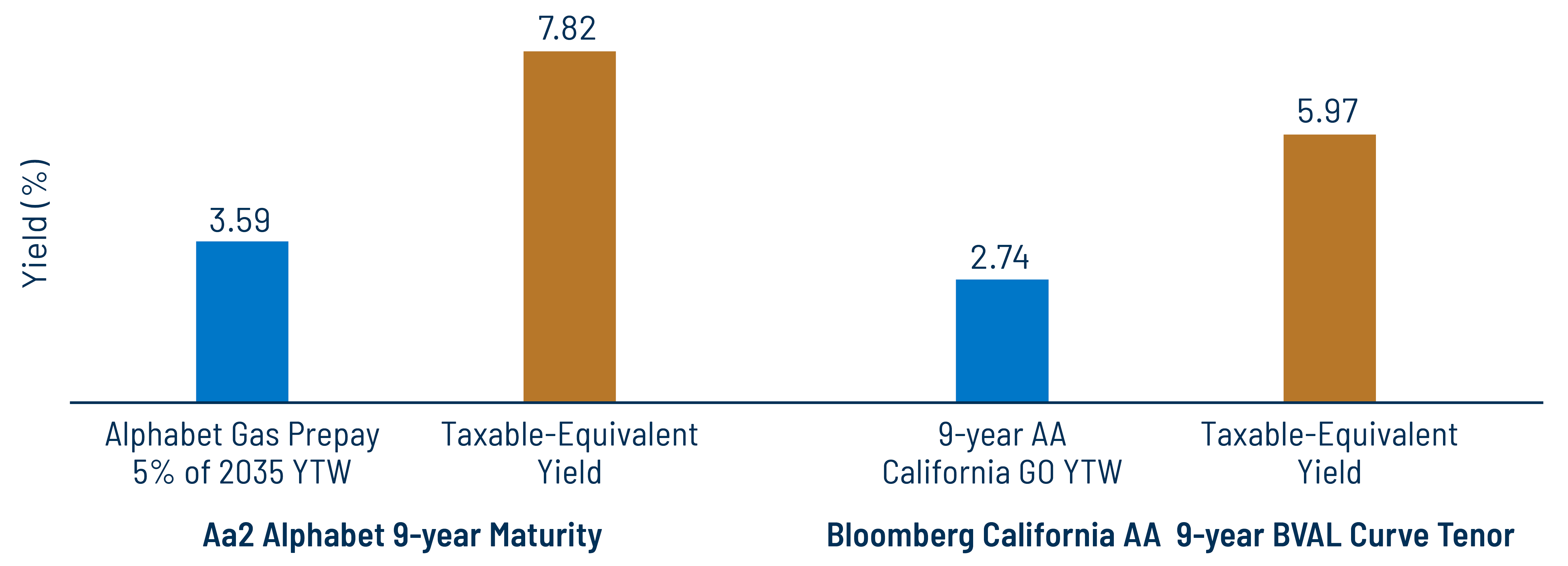

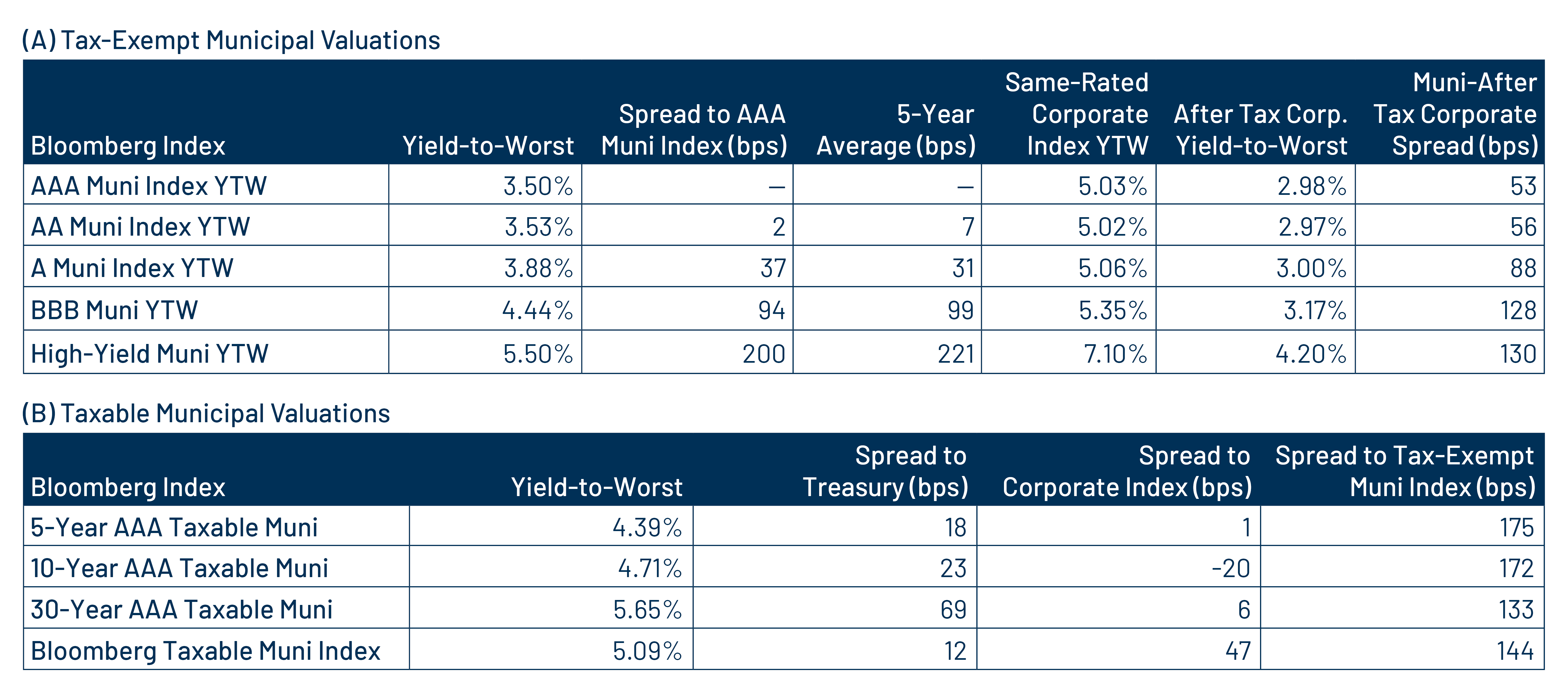

Alphabet’s entry into the municipal market provides investors with additional diversification beyond traditional municipal issuers and offers higher relative income opportunities, particularly for California investors seeking relief from high state and local tax rates. The Alphabet-backed structure, rated Aa2 by Moody’s, traded at a yield of 3.59% in its longest nine-year maturity on Friday, approximately 85 bps above the comparably rated California AA General Obligation curve. After accounting for top state and local tax rates, the bond’s taxable-equivalent yield of 7.82% was nearly 200 bps higher than the taxable-equivalent yield available on comparable traditional California general obligation (GO) securities.

Western Asset believes the expansion of the energy prepay market beyond traditional municipal participants is likely to continue as corporate energy demand rises alongside the growth of data centers and AI infrastructure. While this evolution may provide higher income opportunities and greater diversification within the municipal market, it also highlights the increasing importance of active management within the asset class. We believe managers with deep credit research capabilities spanning both municipal and corporate markets are better positioned to evaluate these increasingly complex structures and identify relative value opportunities that can contribute to favorable after-tax outcomes.

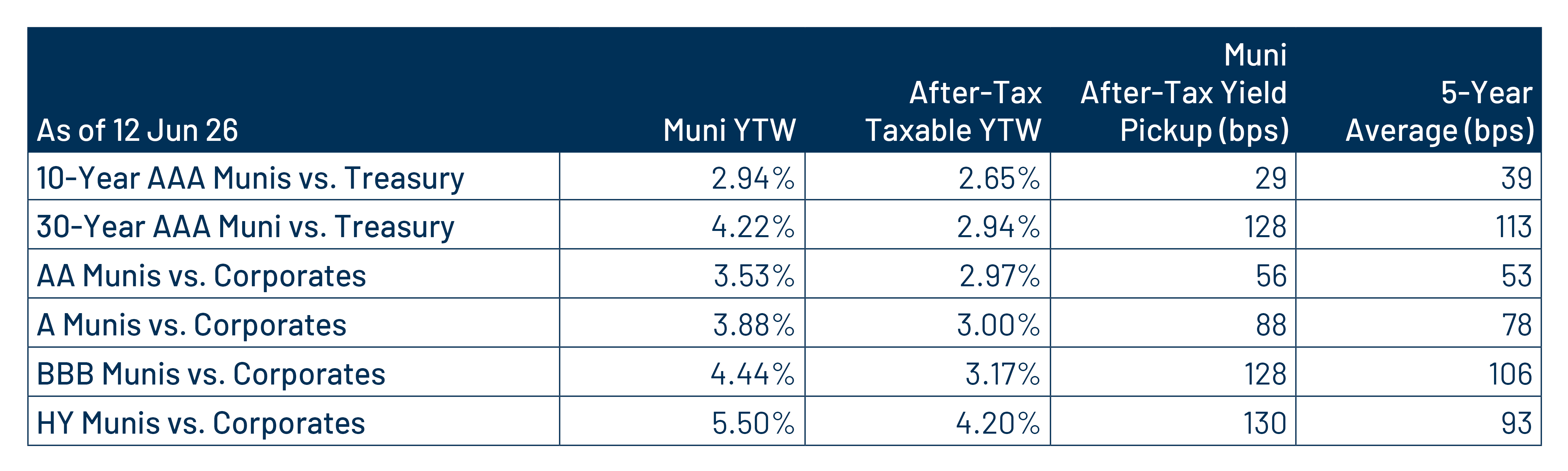

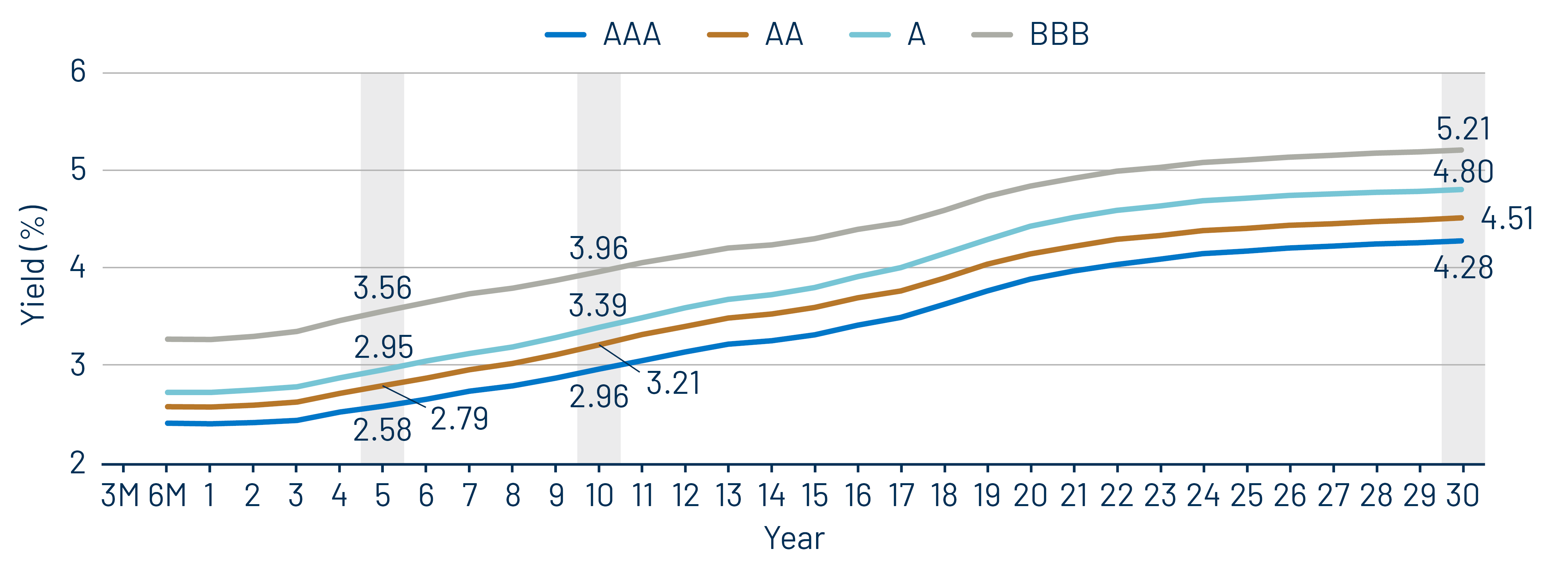

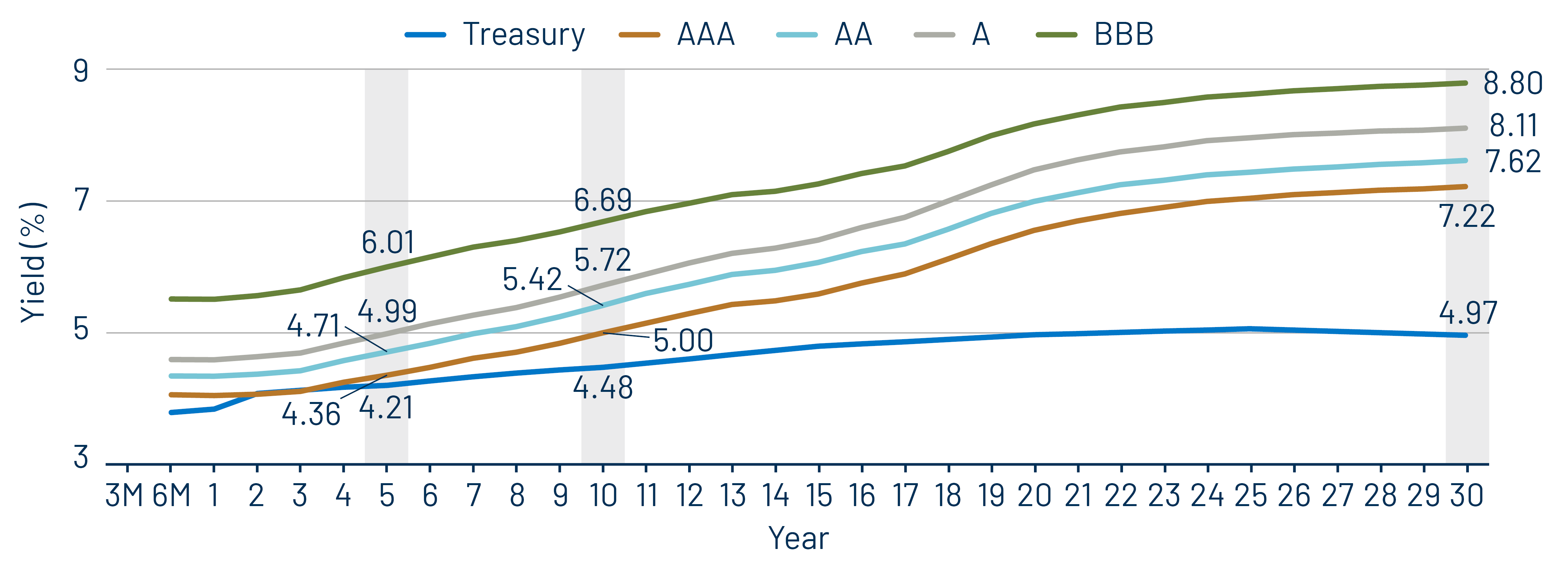

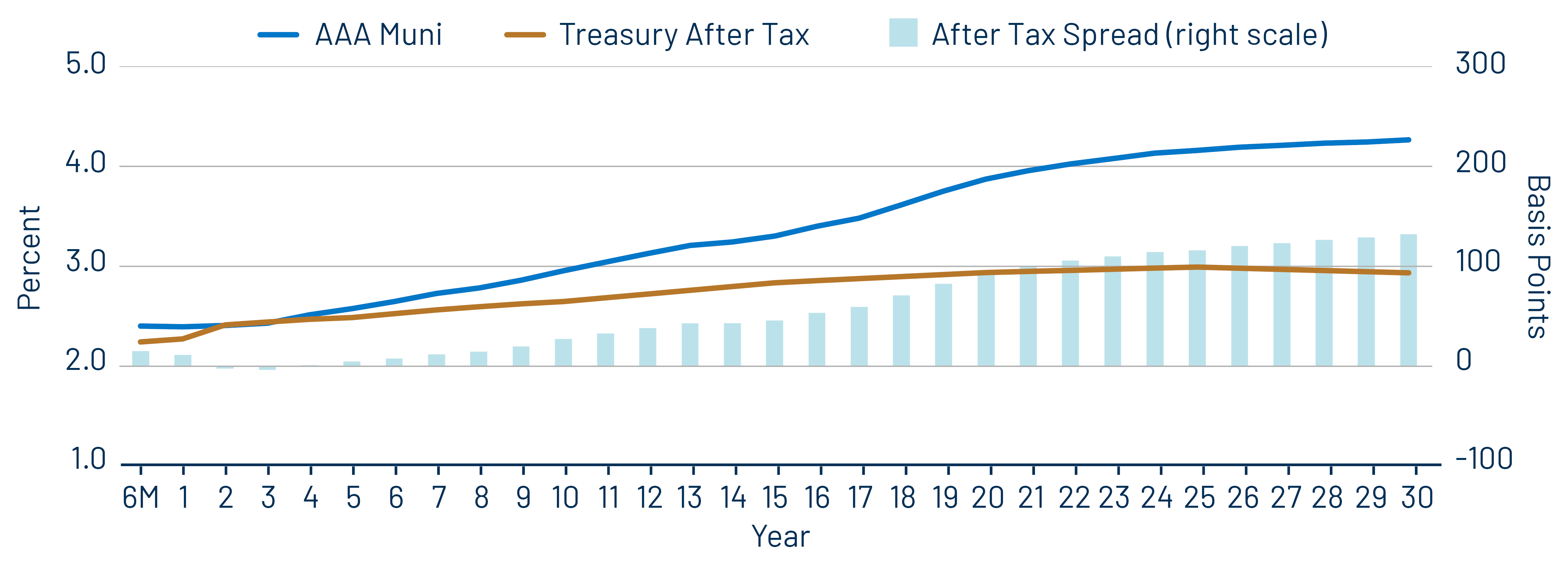

Municipal Credit Curves and Relative Value

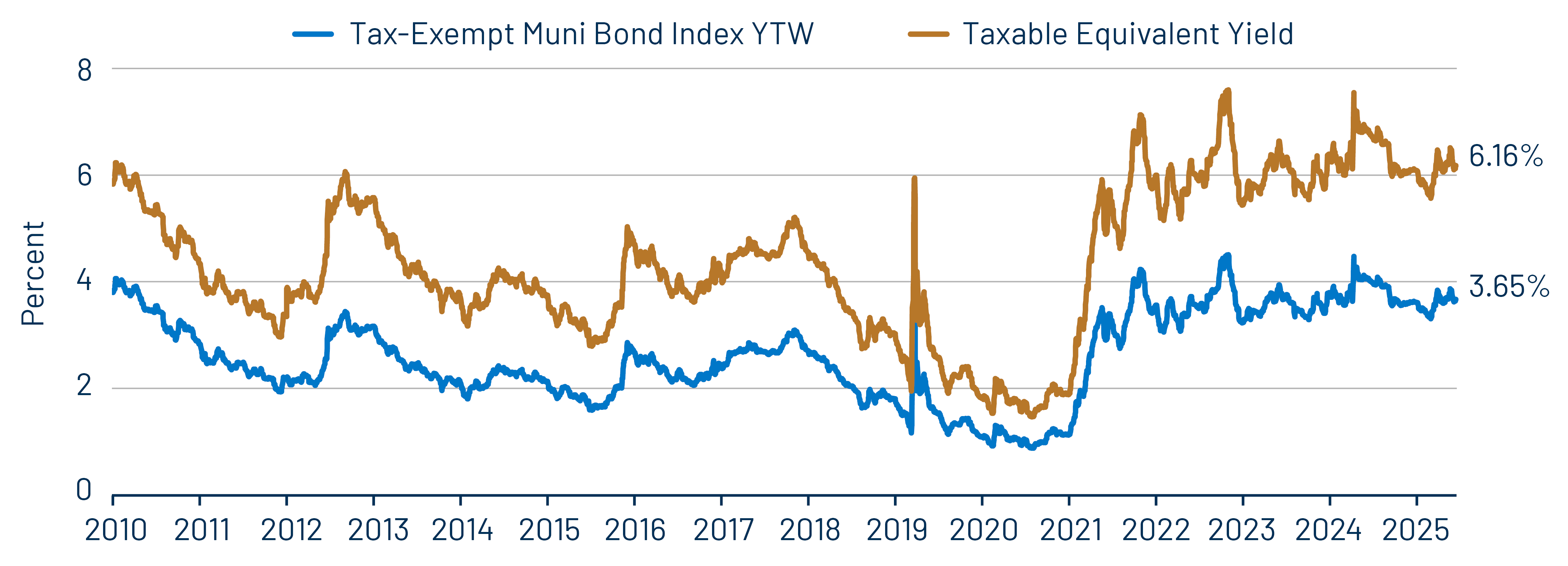

Theme 1: Municipal taxable-equivalent yields moved lower from recent highs, but remain above historical averages.

Theme 2: Munis offer attractive after-tax yield pickup vs. longer-duration and lower-quality taxable alternatives.

Theme 3: The muni curve remains steep and offers relative value in longer maturities.