Macros, Markets and Munis

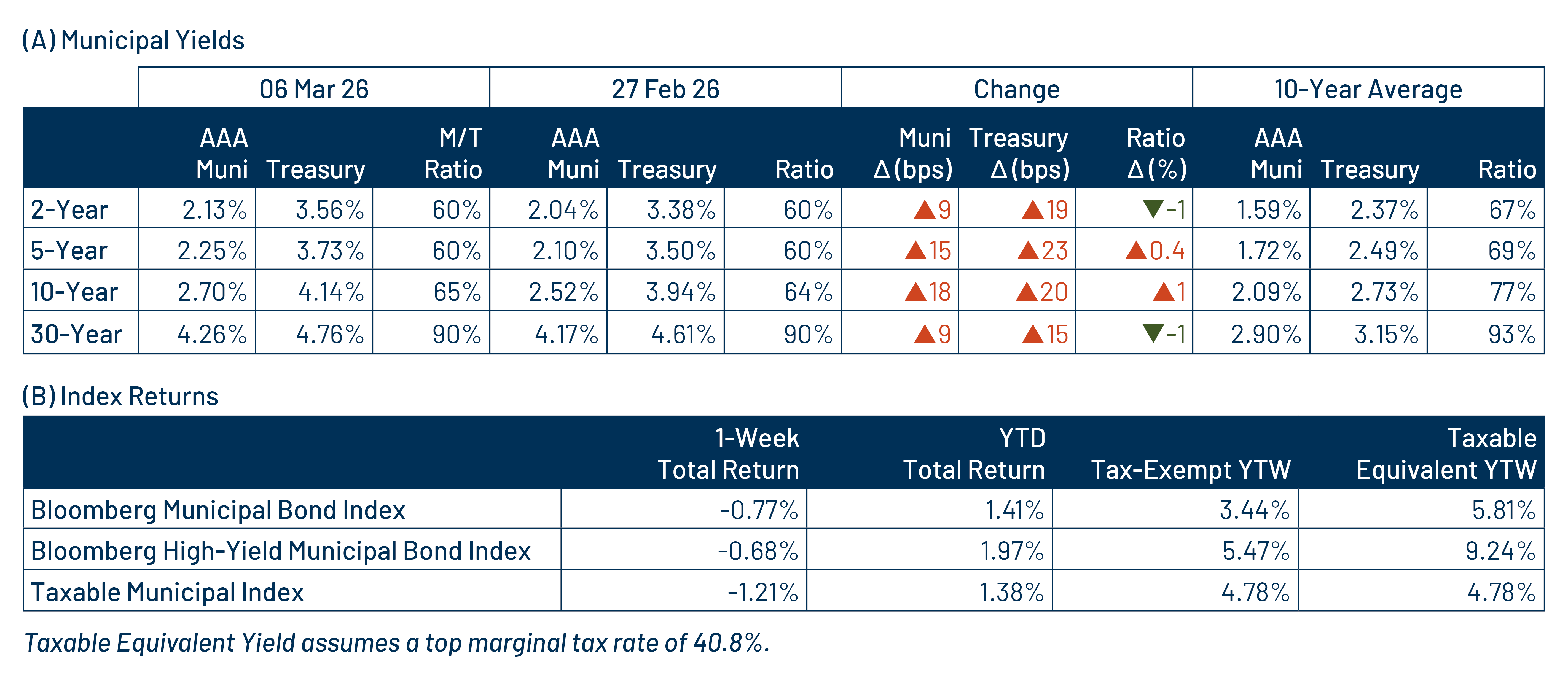

Munis posted negative returns amid heavy market volatility last week. Market volatility increased across sectors following the US and Israel’s strikes on Iran, along with concerns that higher oil prices could reignite inflation pressures. Stronger than expected manufacturing data further fueled inflation concerns. However, those worries were partially alleviated by Friday’s nonfarm payrolls report which indicated a decline of 92,000 positions in February, significantly below the expected gain of 55,000 jobs added for the month. All told, the Treasury curve moved 15–23 basis points (bps) higher across maturities. High-grade municipals moved in sympathy with Treasuries but outperformed on a relative basis, with yields increasing 9-18 bps across the curve. Meanwhile, municipal mutual funds recorded a 15th consecutive week of net inflows. Against the current backdrop of heightened geopolitical uncertainty, we discuss muni market performance last week and potential implications ahead.

Muni Flows Improve Amid Geopolitical Volatility

Fund Flows ($1.4 billion of net inflows): During the week ending March 4, weekly reporting municipal mutual funds recorded $1.4 billion of net inflows, according to Lipper. Long-term, intermediate and short-term categories recorded $798 million, $361 million and $183 million of inflows, respectively. Last week’s inflows marked the 15th consecutive week of net inflows and led year-to-date (YD) inflows higher to $18 billion.

Supply (YTD supply of $87 billion; up 18% YoY): The muni market recorded $12 billion of new-issue supply last week, up 21% from the prior week. YTD new-issue supply of $87 billion is 18% higher than the prior year, with tax-exempt issuance up 20% year-over-year (YoY) and taxable issuance down 23%, respectively. This week’s calendar is expected to increase to $13 billion. The largest deals include $2.5 billion Dormitory Authority of the State of New York (personal income tax) and $2.4 billion state of California transactions.

This Week in Munis: Geopolitical Implications

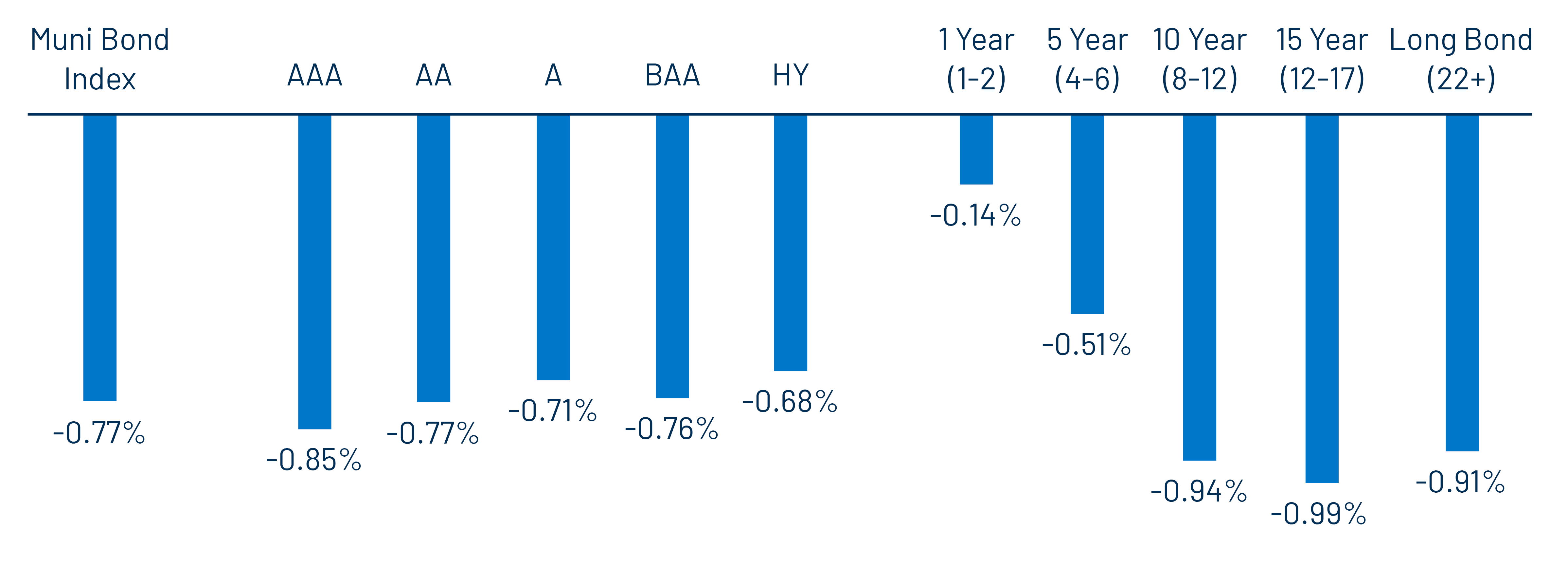

Municipal bonds were not immune to the geopolitical volatility that roiled markets following the Iran conflict, despite their high-quality characteristics. The Bloomberg Municipal Bond Index declined -0.77% last week. While returns were negative, tax-exempt municipals outperformed Treasuries (-0.96%) and Corporates (-0.95%) during the week.

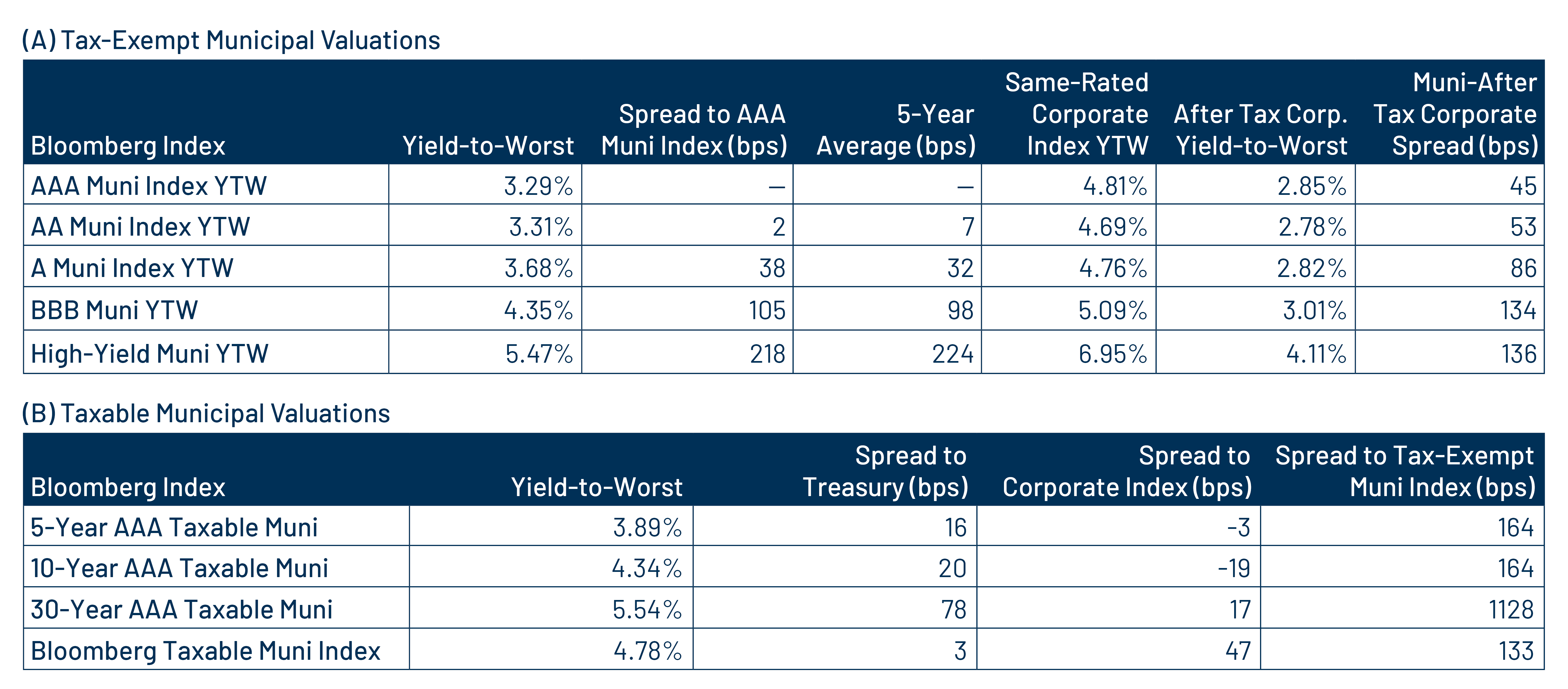

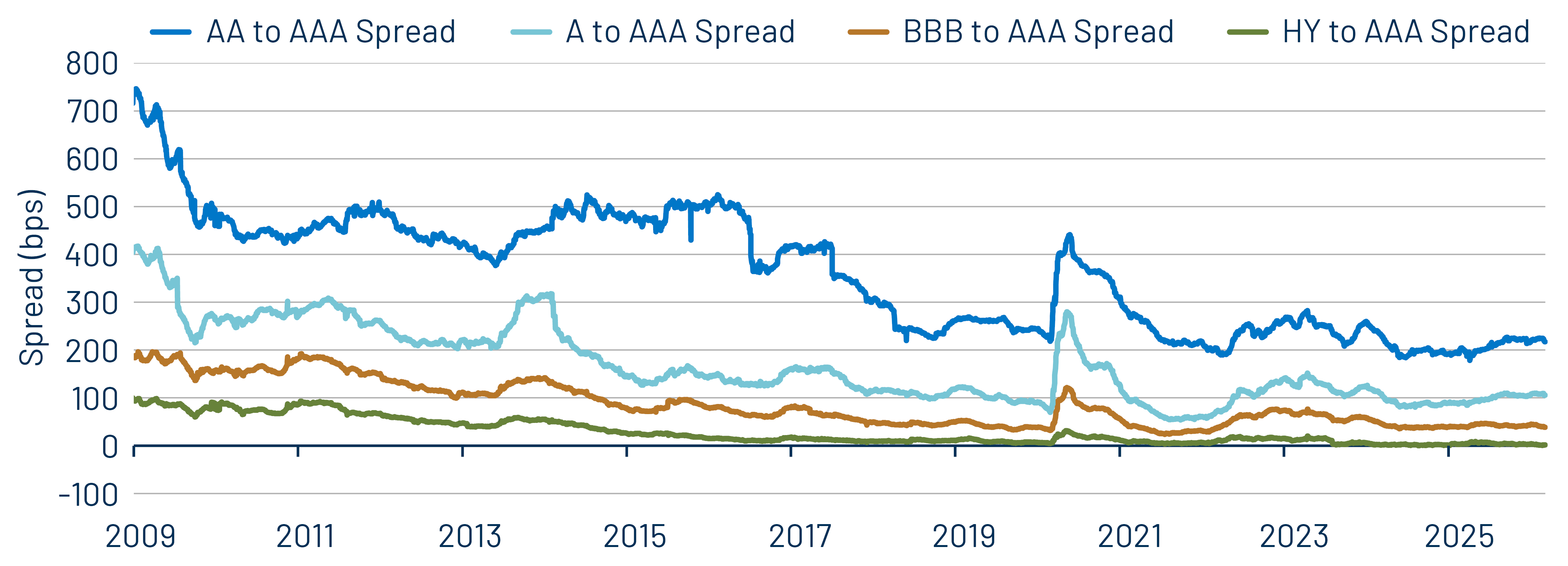

Within the municipal market, there were few places to hide from the negative returns. Higher-quality municipals underperformed, reflecting the selling pressures that often surface in the more liquid segments of the market during periods of elevated volatility. The Bloomberg AAA Municipal Index returned -0.85% during the week, while BBB rated and high-yield municipals returned -0.76% and 0.68%, respectively. Along the yield curve, shorter-duration municipals outperformed, while longer maturities lagged. The underperformance of top-rated municipals further compressed credit spreads, which were already near historically tight levels, underscoring the importance of diligent credit selection.

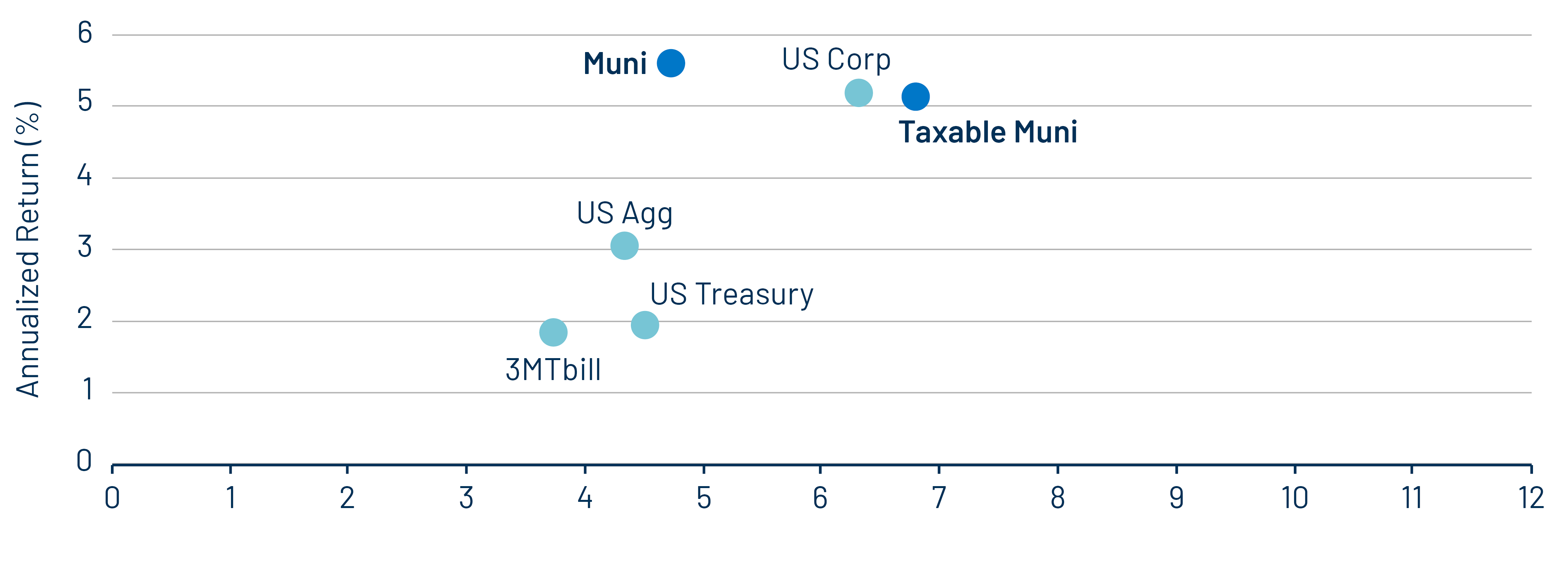

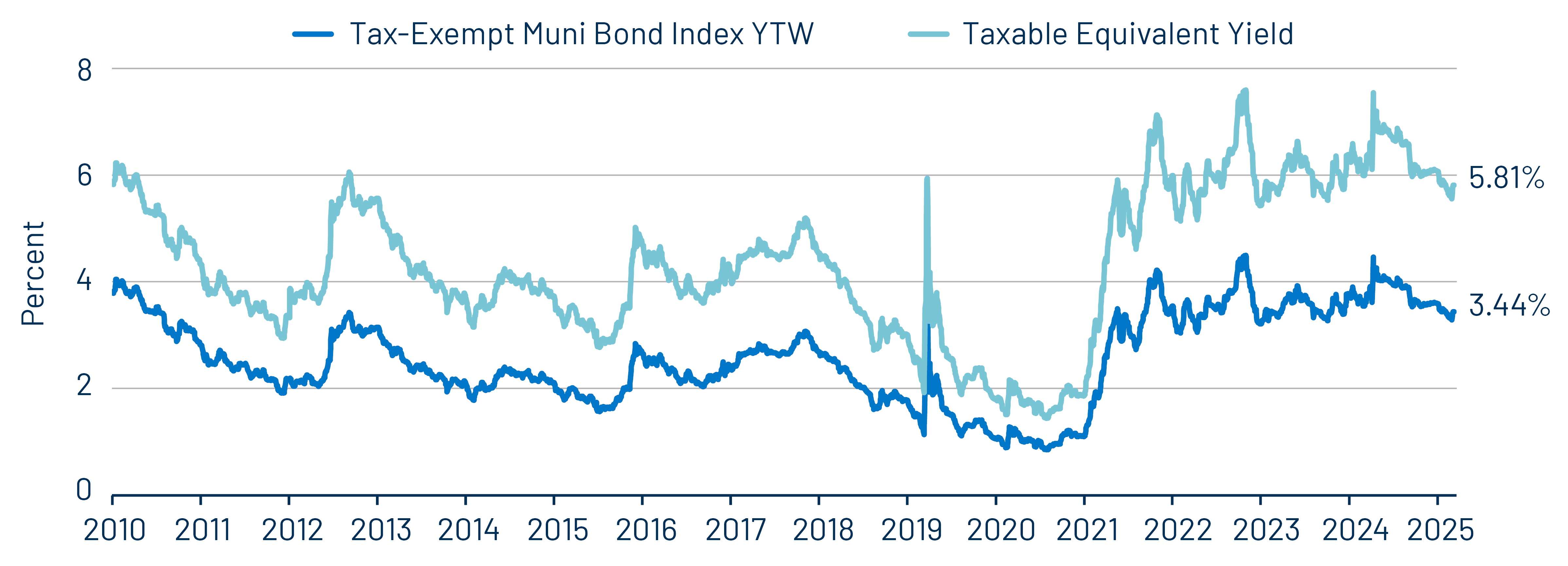

While the length, scope and ultimate implications of the current conflict remain uncertain, for high-tax-rate investors, municipals have historically offered relatively attractive after-tax returns with lower volatility than taxable counterparts over longer time horizons. Notably, historical episodes of near-term volatility have often created attractive entry points for investors seeking tax-exempt income and last week the Bloomberg Municipal Bond Index yield increased 15 bps to 3.44% (or 5.81% on a taxable equivalent basis). Western Asset expects that the increased value of the municipal tax exemption at higher nominal rates, combined with a favorable fundamental and technical backdrop, will continue to support the after-tax relative value proposition of the municipal asset class.

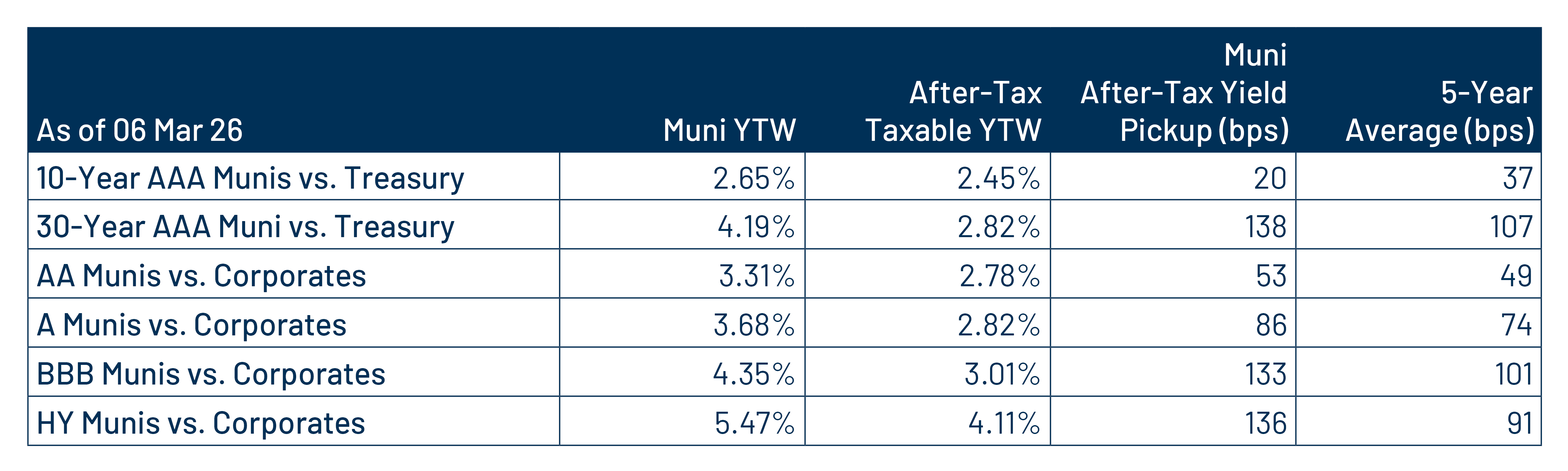

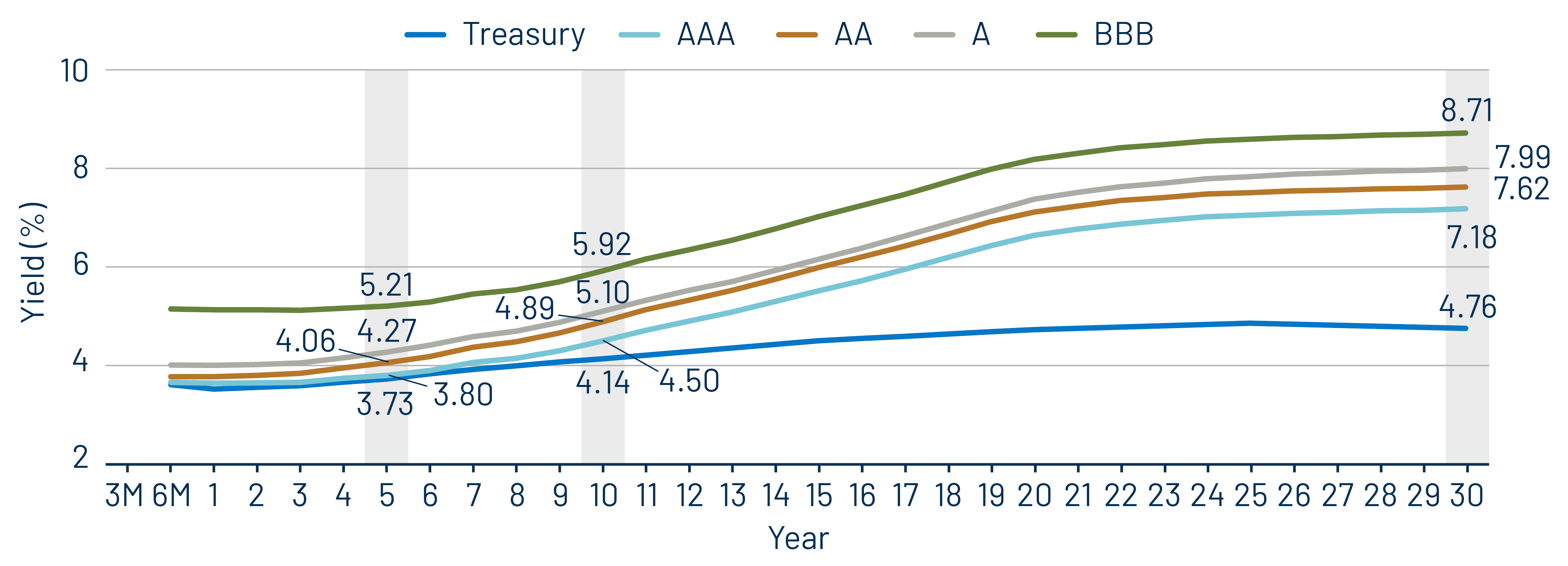

Municipal Credit Curves and Relative Value

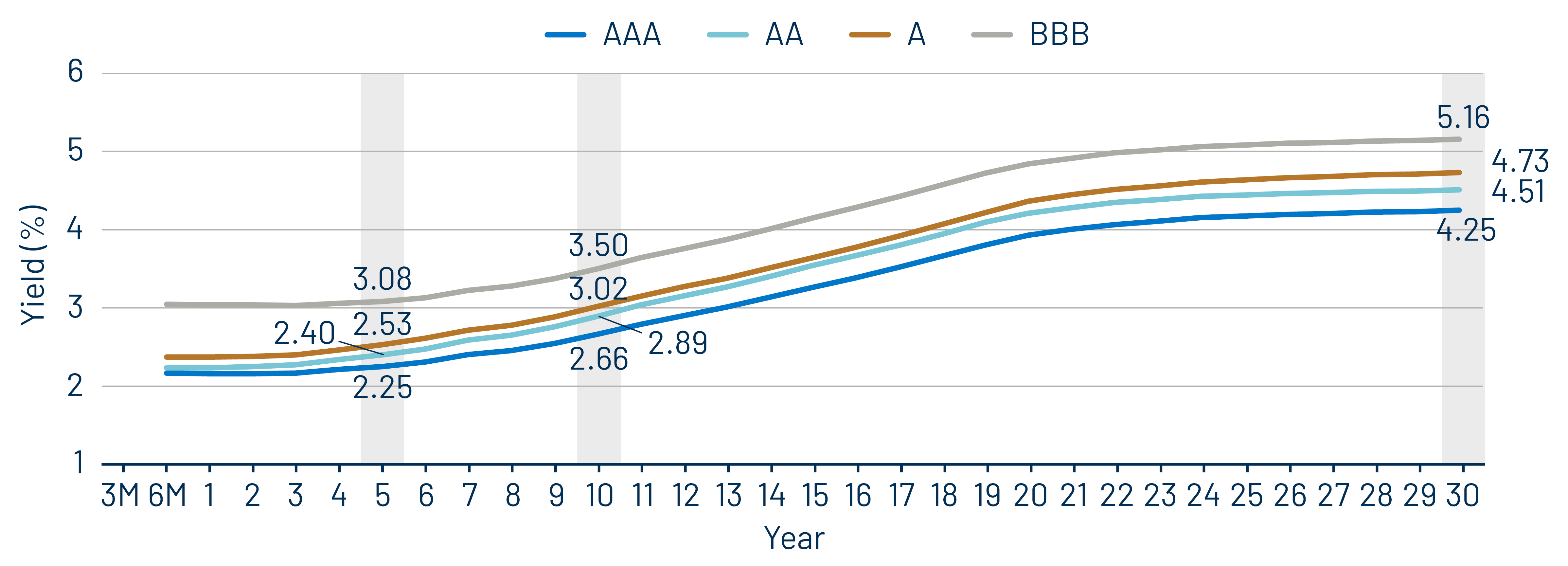

Theme 1: Municipal taxable-equivalent yields moved lower from recent highs, but remain above historical averages.

Theme 2: Munis offer attractive after-tax yield pickup vs. longer-duration and lower-quality taxable alternatives.

Theme 3: Historically tight municipal credit spreads underscore the importance of credit selection.