Macros, Markets and Munis

Munis posted positive returns but underperformed taxable fixed-income last week. Economic data was relatively limited last week, as market volatility remained elevated on concerns surrounding rapid AI development. While Producer Price Index (PPI) readings and consumer sentiment came in above expectations, a flight-to-quality sentiment took hold and high-grade fixed-income rallied. Treasuries moved 10-15 basis points (bps) lower across the yield curve, while municipals outperformed with high-grade munis yields moving 2-6 bps lower across the curve. Meanwhile, municipal demand remained robust, underscored by a 14th consecutive week of inflows. Following a strong month of performance, we provide a muni market update for the month of February.

Muni Fund Flow Streak Continues Amid Elevated Supply Conditions

Fund Flows ($1.0 billion of net inflows): During the week ending February 25, weekly reporting municipal mutual funds recorded $1.0 billion of net inflows, according to Lipper. Long-term and intermediate categories recorded $530 million and $488 million of inflows, respectively. Short-duration funds recorded $68 million of outflows. Last week’s inflows marked the 14th consecutive week of net inflows and led year-to-date (YTD) inflows higher to $18 billion.

Supply (YTD supply of $79 billion; up 17% YoY): The muni market recorded $11 billion of new-issue supply last week, up 31% from the prior week. YTD new-issue supply of $79 billion is 79% higher from the prior year, with tax-exempt issuance up 19% year-over-year (YoY) and taxable issuance down 17% YoY, respectively. This week’s calendar is expected to increase to $13 billion. The largest deals include $1.3 billion city of Houston, TX and $786 million Arizona Highway Transportation Board transactions.

This Week in Munis: February Update

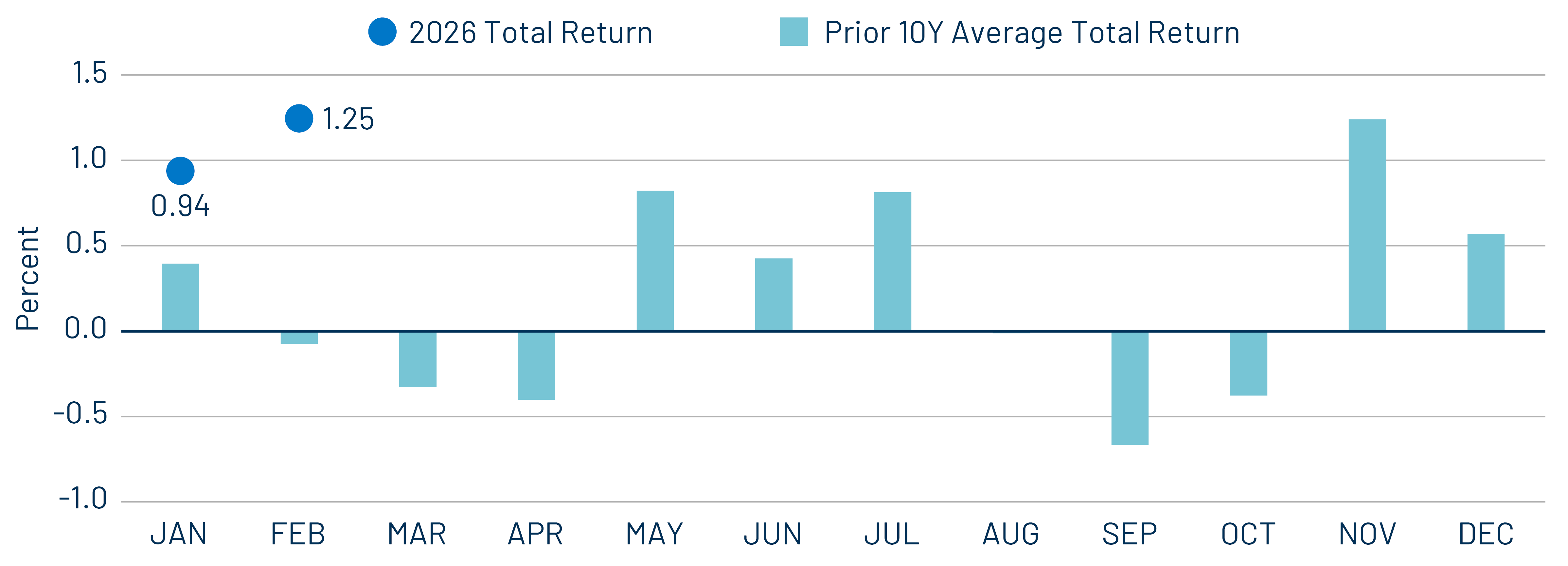

The municipal market posted strong returns in February, with the Bloomberg Municipal Bond Index gaining 1.25% and leading YTD returns higher to 2.20%. Longer-duration and lower-credit-quality municipals generally outperformed during the month. February’s strong performance counters the recent historical weakness with the index averaging negative returns in February, largely driven by softening demand ahead of tax season and limited new issuance.

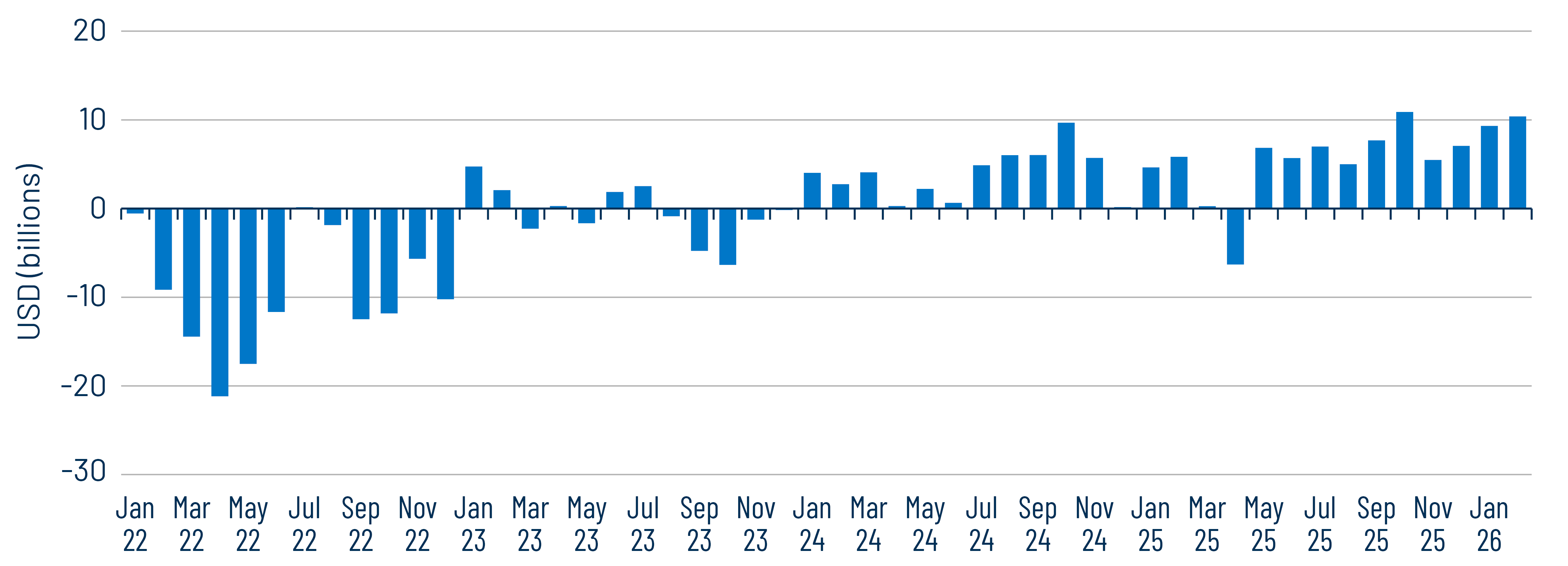

The strong start of the year has been supported by renewed investor demand, as capital has moved decisively back into municipal mutual funds. Investors appear to show an increasing willingness to capitalize on relatively attractive municipal valuations during periods of elevated market volatility, particularly in longer maturities as the yield curve steepened. According to weekly and monthly Lipper and ICI data, municipal mutual funds recorded over $10 billion of net inflows in February. Notably, Lipper estimates that approximately 86% of the $18 billion in YTD inflows has been concentrated in intermediate and long duration fund categories. Since January 2024, cumulative net inflows of over $126 billion on top of strong SMA demand, have fully offset the $122 billion of net outflows experienced in 2022 and 2023.

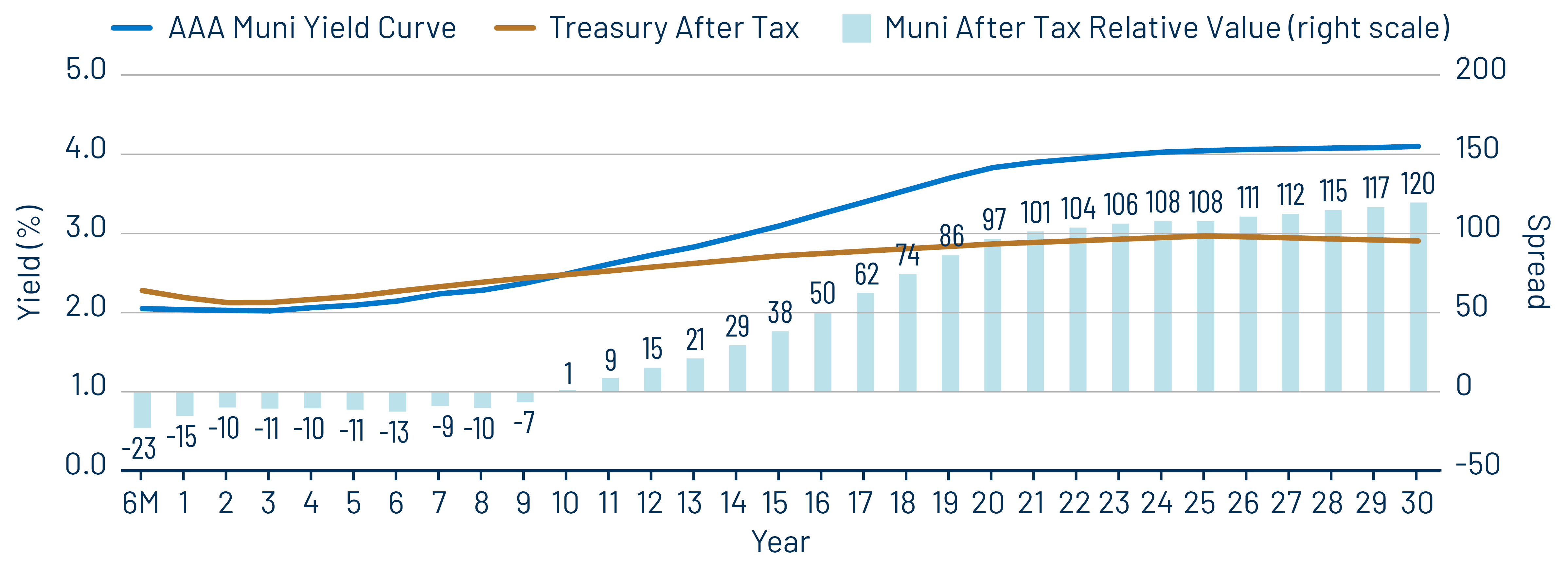

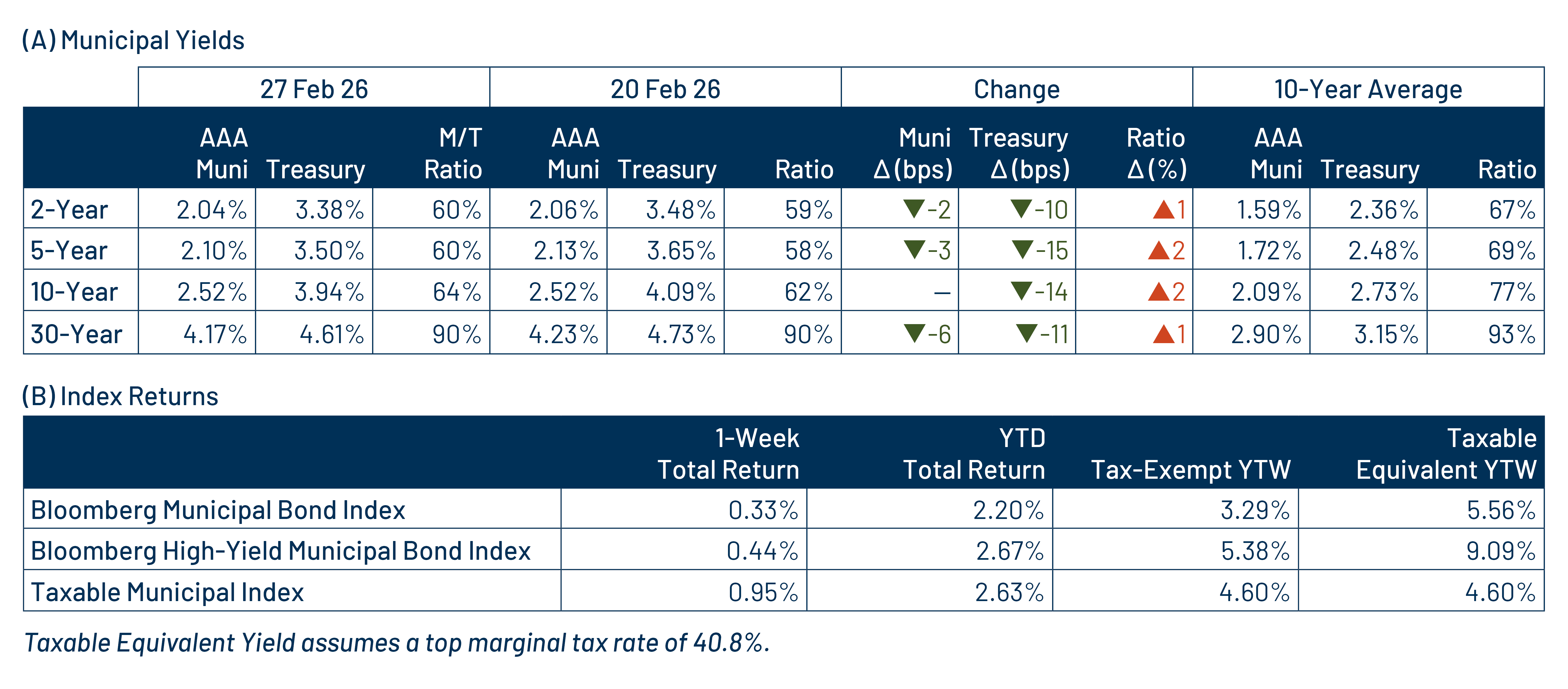

The strong YTD performance also represents a meaningful reversal of the underperformance the municipal market experienced in 2025, and muni supply and demand dynamics have shifted valuations in certain segments of the market. For example, AAA rated municipals maturing inside of 10 years now yield less than comparable Treasuries on an after-tax basis, assuming a 37% effective tax rate, largely attributable to high demand for SMA strategies concentrated in shorter maturities. In contrast, using the same tax rate, AAA municipals beyond 20 years offer more than 100 bps of after-tax yield advantage relative to Treasuries. We believe these valuation disparities create opportunities for active managers to deliver tax-efficient outcomes.

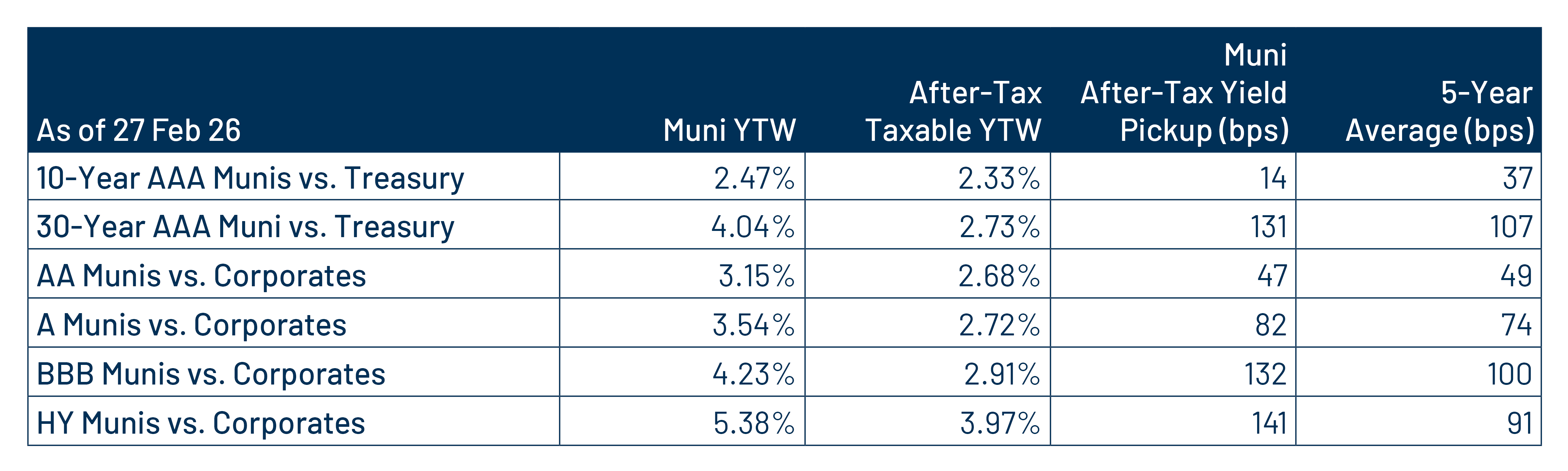

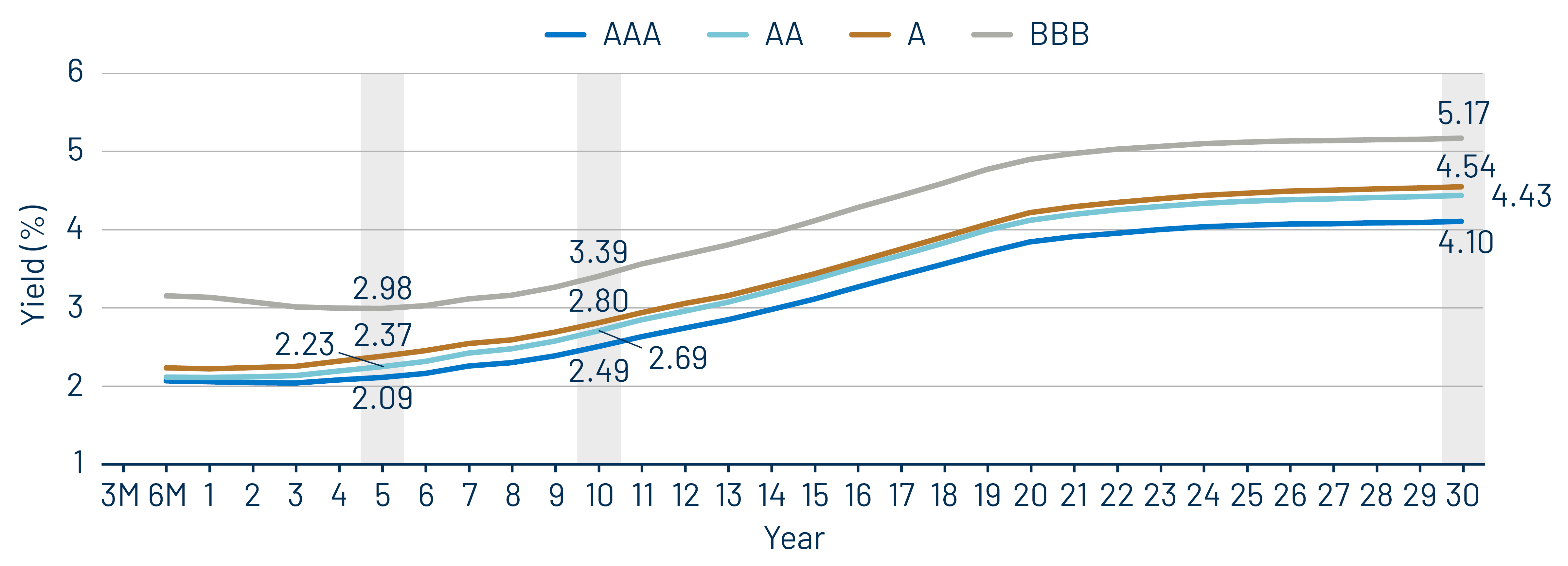

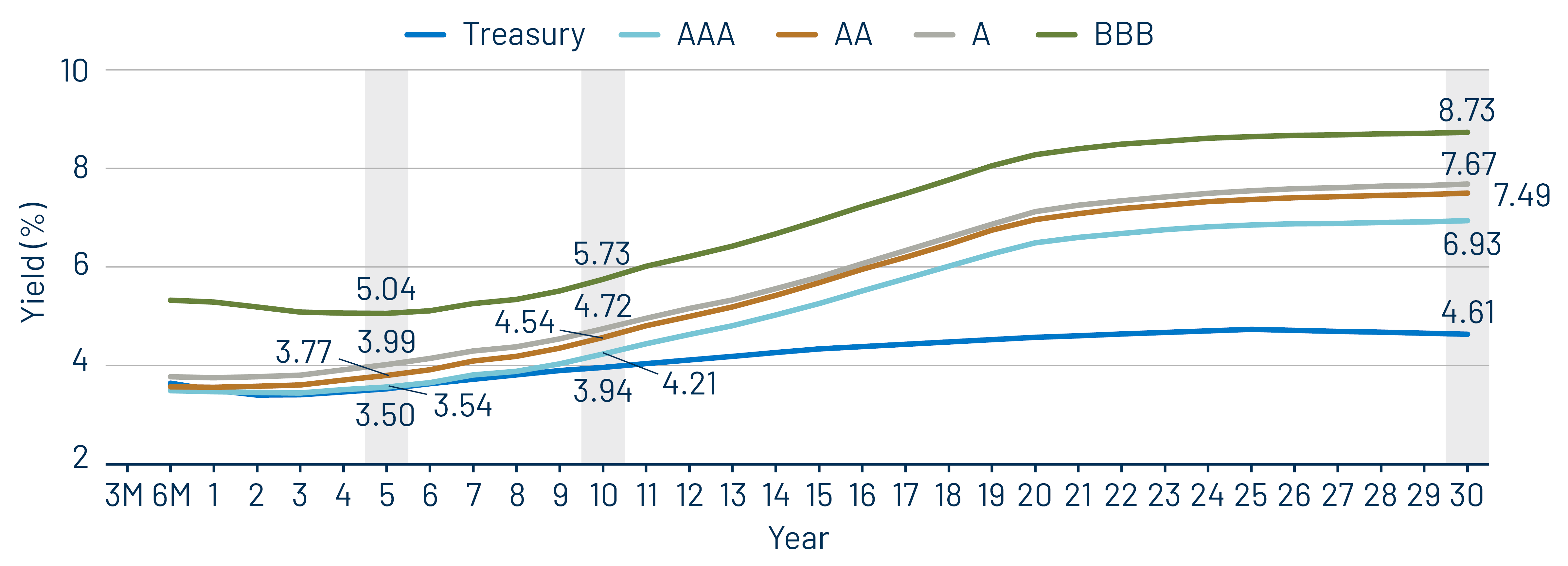

Municipal Credit Curves and Relative Value

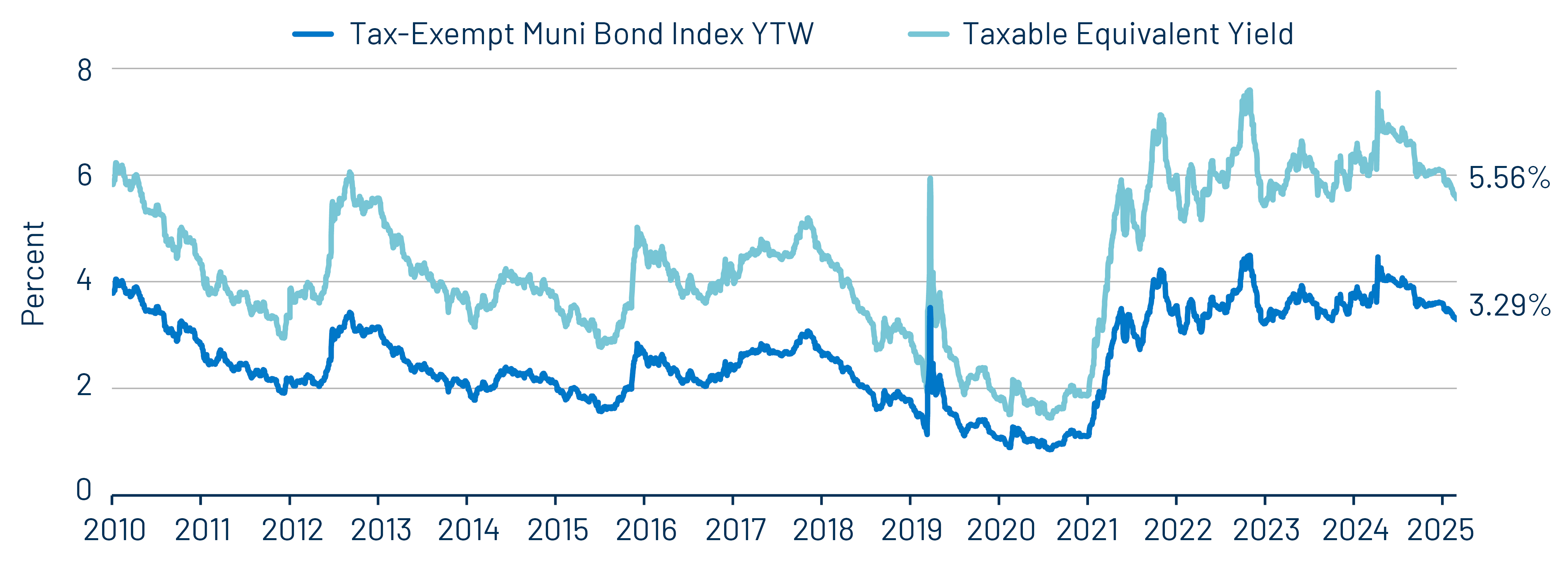

Theme 1: Municipal taxable-equivalent yields moved lower but remain above historical averages.

Theme 2: Munis offer attractive after-tax yield pickup vs. longer-duration and lower-quality taxable alternatives.

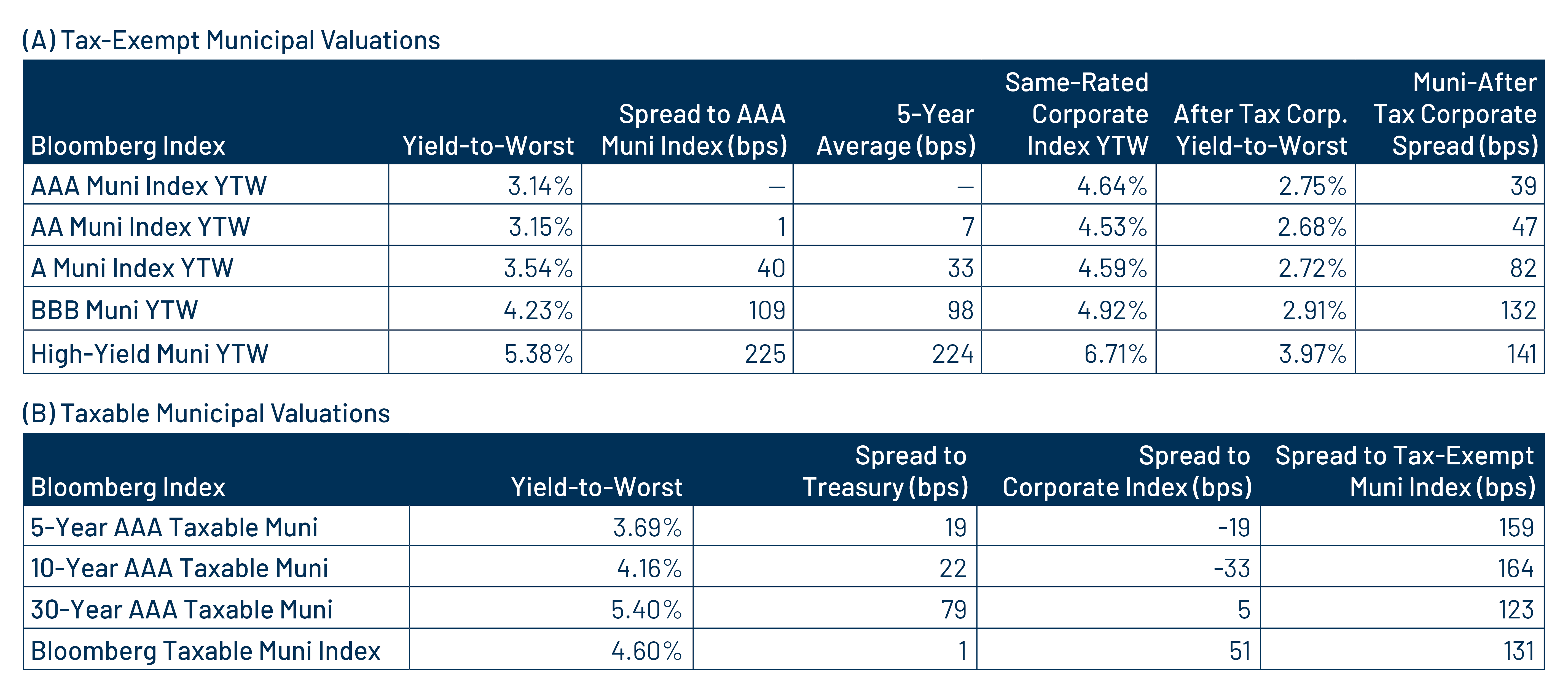

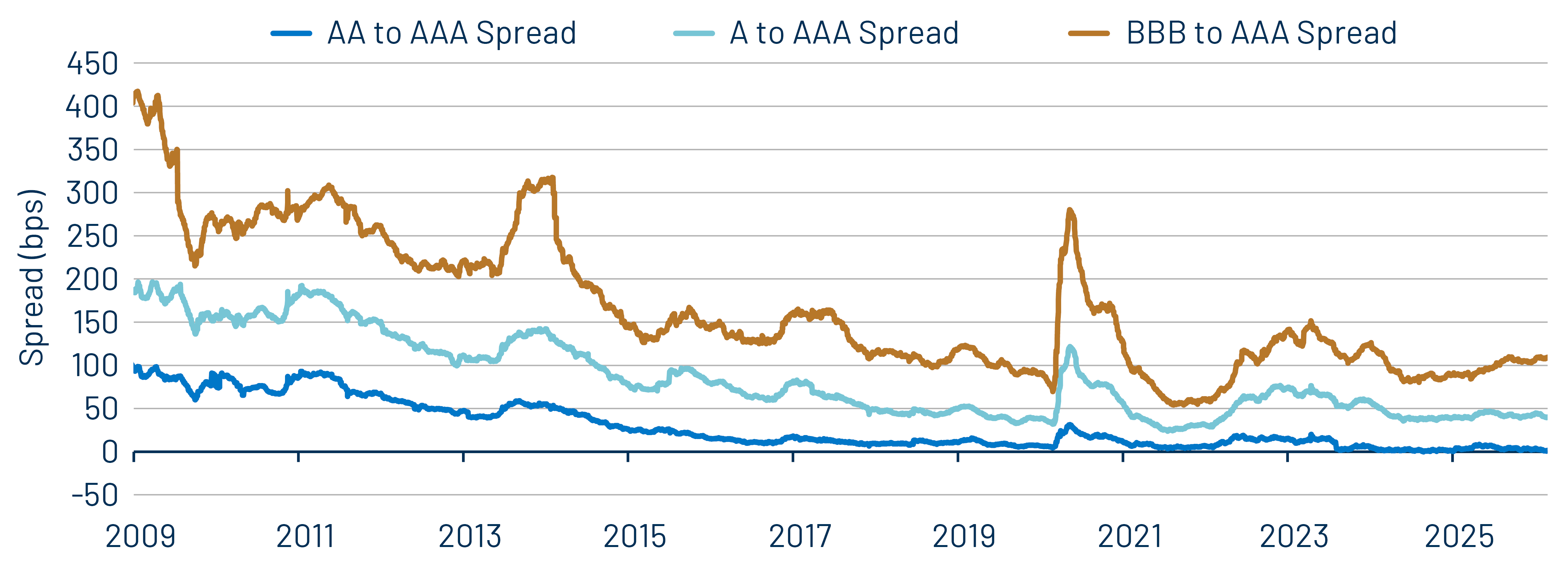

Theme 3: Tight municipal credit spreads underscore the importance of credit selection.