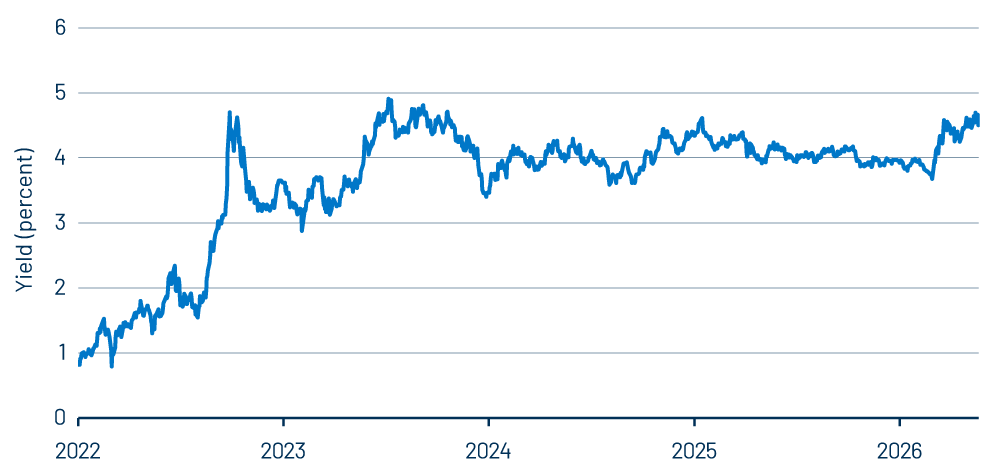

There has been no shortage of commentary on global government bond markets in recent weeks as yields have risen to levels not seen in many years, or in some cases, ever. This is especially true for the UK gilt market where several factors have combined to amplify the rise in yields. This blog post shares some of our high-level thoughts on the outlook and how we are positioned in global portfolios.

The Pre-Iran Outlook

First, it is worth taking a moment to consider the outlook for the UK gilt market that had prevailed prior to the war in Iran. We had written last year about our constructive view as we expected further disinflation progress, a looser labour market and slowing wage growth to provide confidence for the Bank of England (BoE) to reduce its monetary policy restrictiveness further than the market was discounting. In the months that followed, the market consensus converged towards our view and UK gilts rallied as the market expected the BoE to lower its policy rate to 3.25%. Given that narrowing between our view and market pricing, and with consideration to the potential for political risk to resurface in 2026, we significantly reduced our overweight UK duration stance in the final quarter of last year.

Post-Iran

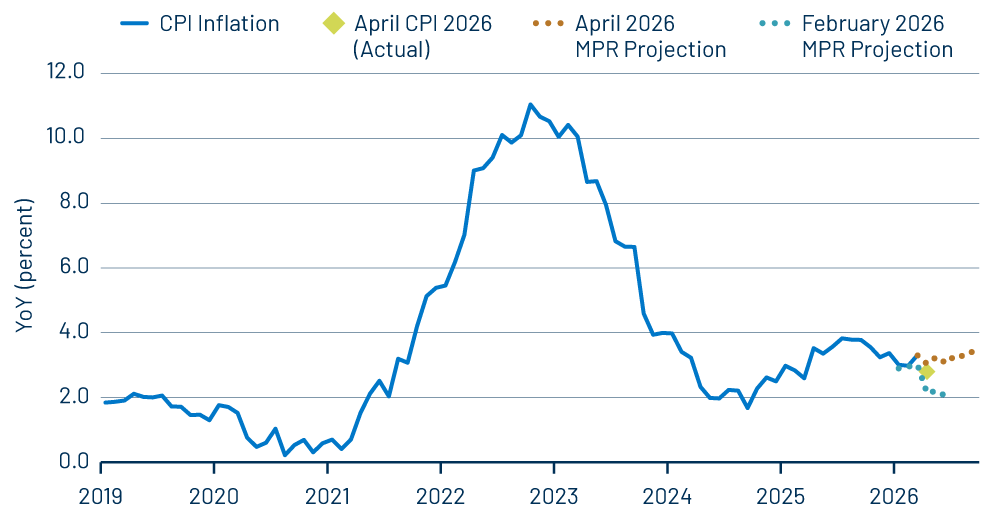

The war in Iran and the energy price shock that resulted from the closure of the Strait of Hormuz have clearly shifted the outlook abruptly. One way to illustrate this is to compare the BoE’s inflation projections in February (pre-war) and April (Exhibit 1). Prior to the jump in energy prices, inflation was set to return to the 2% inflation target in the second quarter of this year. Instead, inflation is now expected to rise later this year as higher prices pass through.

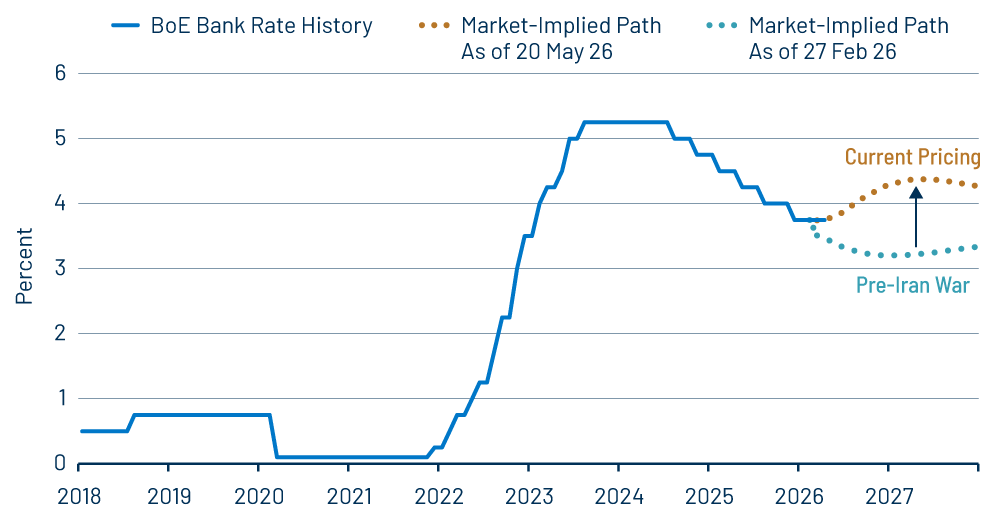

Correspondingly, the market has moved from pricing additional policy rate cuts to discounting multiple rate hikes (Exhibit 2).

Political Risks

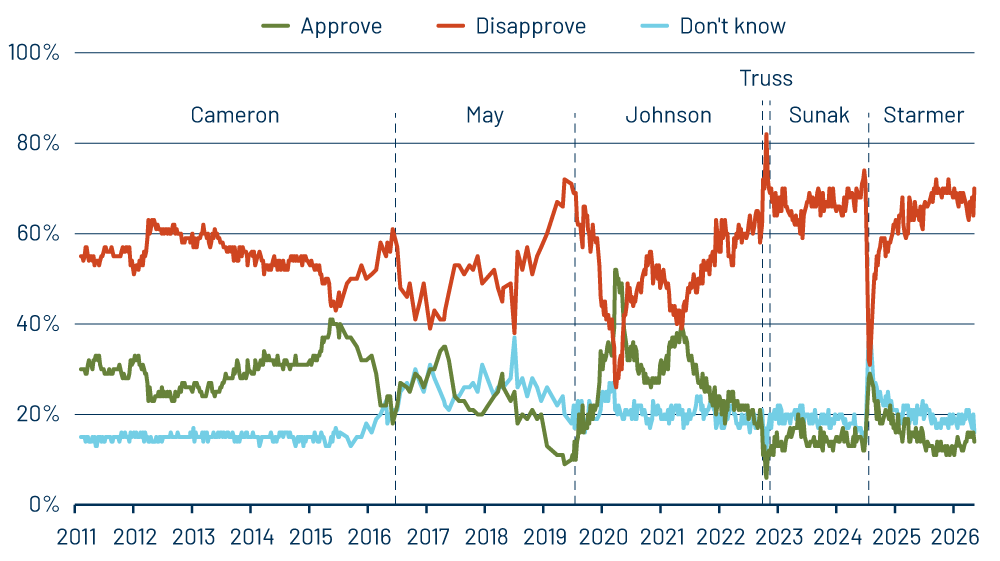

Speculation over Prime Minister Sir Keir Starmer’s position has been a topic of conversation for much of the past year. Public dissatisfaction with his ruling Labour government (Exhibit 3) has seen declining support in polls, towards alternative parties both to the left (Green Party) and the right (Reform). While the next general election is not due until 2029, poor results in local and devolved elections at the start of this month acted as a catalyst for several Labour MPs to call publicly for a change in leadership, hoping to restore the Labour party’s standing among voters. Momentum is clearly building towards a leadership challenge, with political and fiscal uncertainty likely to remain for some months to come.

Our Current Thoughts and Positioning

The UK is highly exposed to the energy shock given its reliance on imports and limited strategic storage capacity. Additionally, a relatively high proportion of the UK’s debt is inflation-linked, which worsens the fiscal projections as inflation rises. The move by Labour MPs towards replacing Starmer raises the prospect of a looser commitment to the current self-imposed fiscal rules and additional public borrowing. Similarly, the prospect of a seventh prime minister in less than 10 years does little to encourage overseas investment and growth in the UK. Therefore, a rise in gilt yields is understandable.

However, there is a reasonable debate whether the BoE tightening currently priced by the market (Exhibit 2) may be too much. Our assessment of the economic data, particularly the rise in unemployment and slowing wage growth, leaves us to expect domestic inflationary pressures to remain contained. Surveys of businesses since the start of the Iran war have shown that firms expect to remain very cautious in their hiring intentions. While almost two thirds of firms indicate they plan to pass on higher costs through pricing, the same amount expect lower profit margins, and half the firms expect lower sales volumes, which begs the question of how strong their pricing power will be.

As a result, with Bank Rate at 3.75% currently and medium-term inflation expectations remaining anchored, we believe that there is scope for the BoE to hold its current policy setting while it monitors developments in the Middle East and additional incoming data. Recent comments from various Monetary Policy Committee members note how financial conditions have already tightened as market-based interest rates have moved meaningfully higher and real incomes have been squeezed, mitigating some of the urgency to act.

The situation in the Middle East remains highly unpredictable and the threat of renewed escalation or an extended closure of the Strait is not conducive to an overly pronounced overweight to duration despite the rise in yields. However, in our view the current UK gilt yields offer an attractive opportunity for fixed income investors. We favour the 5-year part of the yield curve, which should benefit if the market does moderate its view on expected BoE tightening, while being less exposed to the possibility of a further rise in political/fiscal risk premium and the shifting structural demand of UK pension funds.