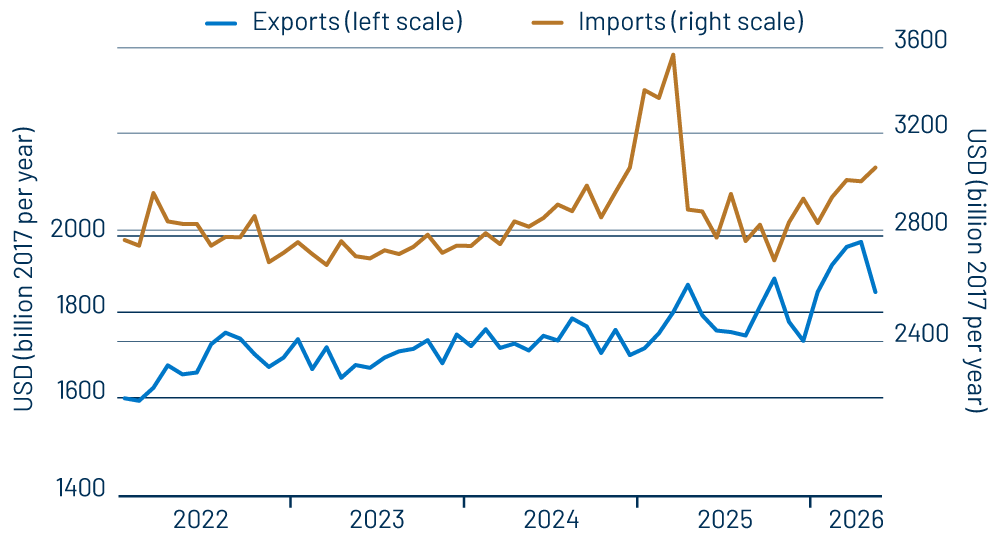

The US merchandise trade deficit increased in May to $105.9 billion on a seasonally adjusted basis, up from $82.2 billion in April, as exports fell $12.4 billion and imports rose $12.0 billion. That served to offset smaller deficits that had occurred over January-April of this year. However, it is evident from Exhibit 1 that not much has changed recently in terms of trends in the trade balance or in exports and imports separately.

Imports have been increasing this year, after appearing to decline over the last nine months of 2025. However, this is deceiving, as the import decline over April-October of 2025 is likely just an offset of the surge in imports in the first three months of 2025. US imports and foreign producers appear to have ramped up flows of goods into the US in early 2025 in order to get the goods into the country prior to the imposition of tariffs. Once that surge of imports had served to swell stockpiles of imported goods and once the tariffs were in place, import flows of new goods were then pulled back, and merchants filled orders by drawing down their inventories.

It is clear from the first chart—and our calculations will back up the fact—that on balance, since the start of 2025, the cumulative value of imports is higher than what pre-2025 trends would suggest. In other words, the Trump tariffs shifted trade flows forward (earlier) in time than what would otherwise have occurred, but they did not result in any net diminution in imports into the US. Meanwhile, with the tariffs struck down in large part this year by the Supreme Court, imports have resumed a rising trend.

It is true that essentially all the increase in imports this year has been in capital goods. This is the flip side of the massive increase in foreign investment in the US that the Trump administration has negotiated. As we have discussed previously, capital spending in the US has grown explosively over the last year plus. A good chunk of that over the last eight months has been imported equipment. Yes, US exports of equipment have picked up, and domestic production of equipment for domestic use has also increased, but the fact remains that foreign investment in the US must be financed, and much of that “finance” has consisted of bringing in foreign equipment.

Outside of equipment, US imports of merchandise remain lower than late-2024 levels, but, again, that is mostly an offset of the import surge of early-2025.

On the export side, much of the bulge in exports over February-April was in petroleum and related products, as US oil exports worked to offset reductions in oil shipments from the Mideast to Europe and Asia due to the Iran conflict. Other exports are growing, but with a lot of short-term “chop.” Tariffs and related trade swings have prominently affected short-term swings in the trade data, and those swings have distorted the GDP growth data in various quarters, namely 1Q25 and 1Q26.

However, there has been no real change in the US trade balance trend, and once the stockpiles accumulated in early-2025 are fully wound down, it is likely that the monthly trade flow data will be little changed or unchanged. In other words, the Trump tariffs have been a lot of heat, with little or no light.

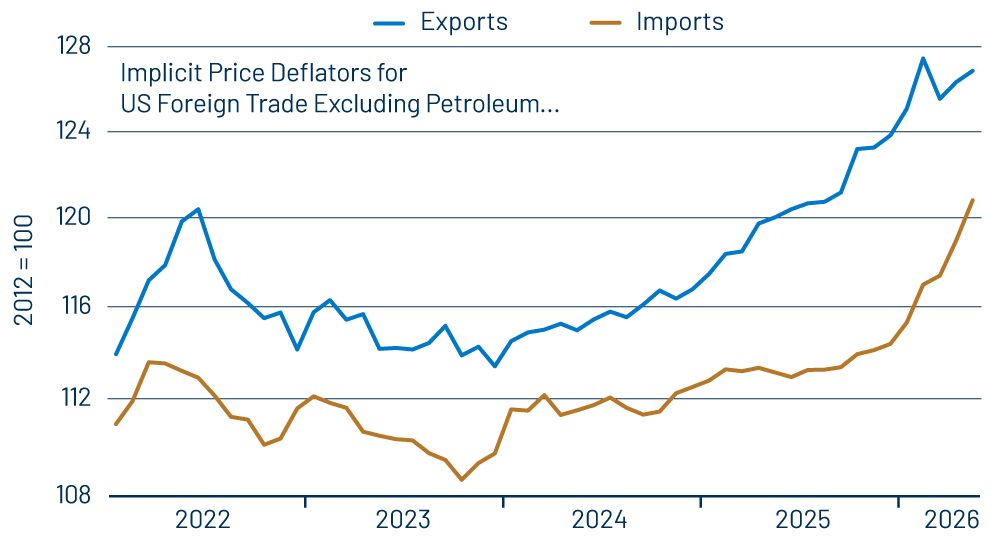

You can also see this in the trade price data charted in Exhibit 2. Tariffs are actually paid directly by US importers. For foreign producers to bear some of the costs of the tariffs, import prices on a c.i.f. basis, such as are shown in the second chart, would have to decline to offset some of the importers’ burdens from the tariffs. As Exhibit 2 makes clear, that was not the case in 2025, and this year, import prices have increased sharply, even though tariffs have largely been struck down.

Import price increases have occurred for capital goods, industrial materials and other goods. Prices of imported consumer goods have held steady, but they haven’t declined any. Meanwhile, yes, export prices have also been increasing. In fact, they had been rising for two years prior to 2026. It may be that these trends toward higher prices for traded goods have nothing to do with the Trump tariffs. Our point is that there is no indication in the data that tariffs—when they were in effect—were being absorbed by foreign producers.

Again, the tariffs—when they were in effect—looked to have little discernible effect on trade flows, other than inducing US importers to stockpile goods in 2025 before the tariffs were in place. Tariffs have largely been removed for a few months now, and by the end of the year, trade flow data will largely be unaffected by the trade furor. In the meantime, it is hard to see any effect of the tariffs on economic growth trends. They do look to have increased domestic goods prices in the last half of 2025, but those effects also appear to have waned.