In recent weeks, a common set of questions has come up in client conversations. They all center on the same theme: the role of the US dollar in a world that feels increasingly unsettled. These questions aren’t new, but the frequency and urgency behind them have picked up, reflecting a shift in both the market environment and the broader geopolitical backdrop. As such, they warrant a fresh look.

1. Is the US dollar still the dominant force in the global financial system?

Yes. The dollar remains at the center of the system in ways that are difficult to replicate. It’s still used in the vast majority of foreign exchange (FX) transactions, anchors global funding markets and represents roughly 57% of global FX reserves.1 The gradual decline in the USD’s share of reserves (from its peak of 72% in 2001) can be traced to structural developments such as the formation of the eurozone, China’s entry into the World Trade Organization and periodic de-dollarization efforts by countries seeking to reduce USD dependency, diversify reserves or limit exposure to US policy and sanctions.

That said, it’s important to keep the purpose of reserves in mind. Countries hold reserves to protect against economic shocks, influence their exchange rates, cover imports and service external debt. The currencies that meet these needs must offer economic strength, policy credibility, sound governance and deep, liquid and transparent capital markets. On these measures, the US continues to stand apart.

Recent market behavior reinforces this point. During the latest escalation in the Middle East, the dollar strengthened meaningfully, in some cases outperforming traditional safe havens such as gold, the Japanese yen and the Swiss franc. That response is consistent with past episodes of stress and highlights the system’s continued reliance on dollar liquidity. For all the discussion around de-dollarization, there’s still no viable alternative that can replicate the scale, depth and institutional backing of the US dollar system.2

2. Are central banks globally moving away from the US dollar?

No, but there’s clear evidence of incremental change. Central banks have been diversifying reserves, gold purchases have accelerated to multi-decade highs and some countries are experimenting with non-dollar trade settlement, particularly in energy markets.3 These trends are real and, in some cases, policy-driven.

However, scale remains the defining constraint. Across virtually every metric that matters, including trade invoicing, cross-border lending, international debt issuance and payment systems such as SWIFT, the US dollar continues to dominate.4 This reflects not only the size of the US economy, but also the credibility of its institutions, the independence of its legal framework and the depth of its financial markets.

What we’re observing is not a move away from the dollar, but a gradual erosion of its exclusivity. Recent research and market commentary suggest that the pace of diversification is increasingly tied to US policy decisions, including the use of sanctions, trade policy and concerns around fiscal sustainability and institutional credibility. In that sense, diversification is no longer purely economic; it’s also geopolitical.

Heightened uncertainty around the Iran war, and the risk of broader regional disruption, has reinforced the need for countries to reassess their exposure to global systems, including the dollar-based financial architecture. Even so, these shifts remain incremental rather than systemic.

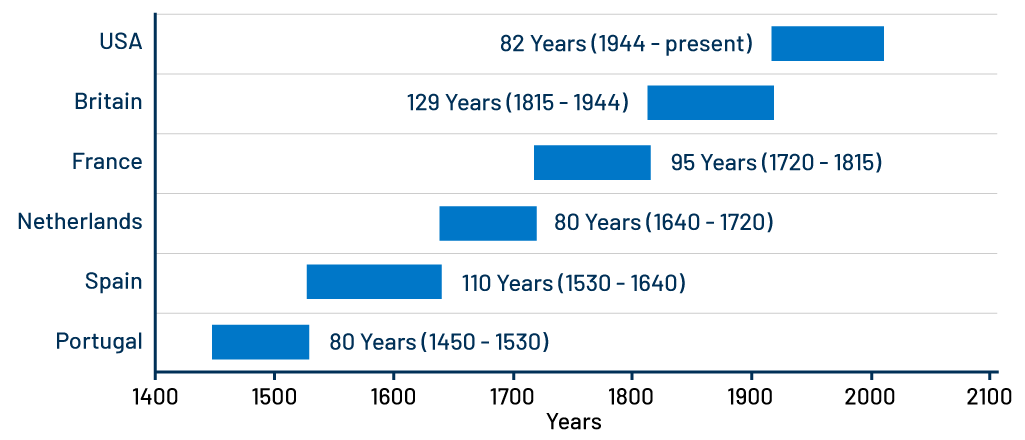

3. History shows that the transition of each global reserve currency took place over roughly a century, often during periods of major economic and political upheaval. Is the US poised to meet the same fate, and how should investors view the US dollar at this point?

Investors shouldn’t be quick to abandon the view of the dollar as a safe-haven asset. While the dollar has, at times, lagged expectations in recent risk-off environments, it continues to strengthen during periods of more acute stress, reaffirming that alternatives such as the euro, the Chinese yuan, special drawing rights or digital currencies still fall short of providing the same level of liquidity, convertibility and institutional support.

At the same time, it’s becoming increasingly clear that the dollar is no longer driven solely by growth and interest-rate differentials. Policy credibility is playing a larger role these days. Markets are paying closer attention to US fiscal dynamics, trade policy, political pressure on the Federal Reserve and, more recently, the implications of strategic overstretch.

In international relations, strategic overstretch refers to a situation in which expanding military commitments begin to strain a country’s ability to sustain its global role.5 As the US becomes more engaged across multiple geopolitical fronts, including the ongoing conflict involving Iran, questions are emerging around the sustainability of its security commitments, the adequacy of military stockpiles and the fiscal cost of prolonged engagements.

These concerns are unfolding alongside an already elevated fiscal backdrop. US federal debt now exceeds $38 trillion, and additional military and security expenditures risk adding further pressure over time.6 While none of these factors may challenge the dollar’s dominance in the near term, they do introduce a new dimension to how markets assess US credibility.

The implication is not that the dollar is losing its role, but that the conditions under which that role is expressed are evolving. Dollar movements remain driven by familiar cyclical forces, but those forces are now interacting more directly with geopolitics and policy. The result is a currency that is more sensitive, more reactive, and, at times, more volatile than in prior cycles.

ENDNOTES

1. Neely, C., Cole. A. 25 February 2026. “The U.S. Dollar’s Role as a Reserve Currency.” Federal Reserve Bank of St. Louis.

2. The other major reserve currencies with their respective shares are the euro (20%), the Japanese yen (6%), the British pound (5%), the Canadian dollar (3%) and the Chinese renminbi (2%).

3. Deutsche Bank. 24 March 2026. “’Petrodollar regime’ could be undermined by Iran war.” The Guardian.

4. Bertaut, C. von Beschwitz, B. and Curcuru, S. 18 July 2025. “The International Role of the U.S. Dollar – 2025 Edition.” Board of Governors of the Federal Reserve System; The Society for Worldwide Interbank Financial Telecommunications (SWIFT) is a messaging system that allows banks and other financial institutions globally to send and receive encrypted information, specifically cross-border money transfer instructions.

5. Cordesman, A. 31 January 2022. “Strategic Triage vs. Strategic Overreach.” Center for Strategic and International Studies.

6. Joint Economic Committee. 9 January 2026. “National Debt hits $38.43 Trillion, Increased $2.25 Trillion Year over Year, $8.03 Billion Per Day.”