The Total Portfolio Approach, or TPA, is one of the most discussed topics in institutional investing, drawing interest from pension plans, reserve managers, endowments, consultants and other long-term asset owners. The appeal is straightforward: as investment opportunity sets continue to expand, so does the complexity of making investment decisions across large institutions.

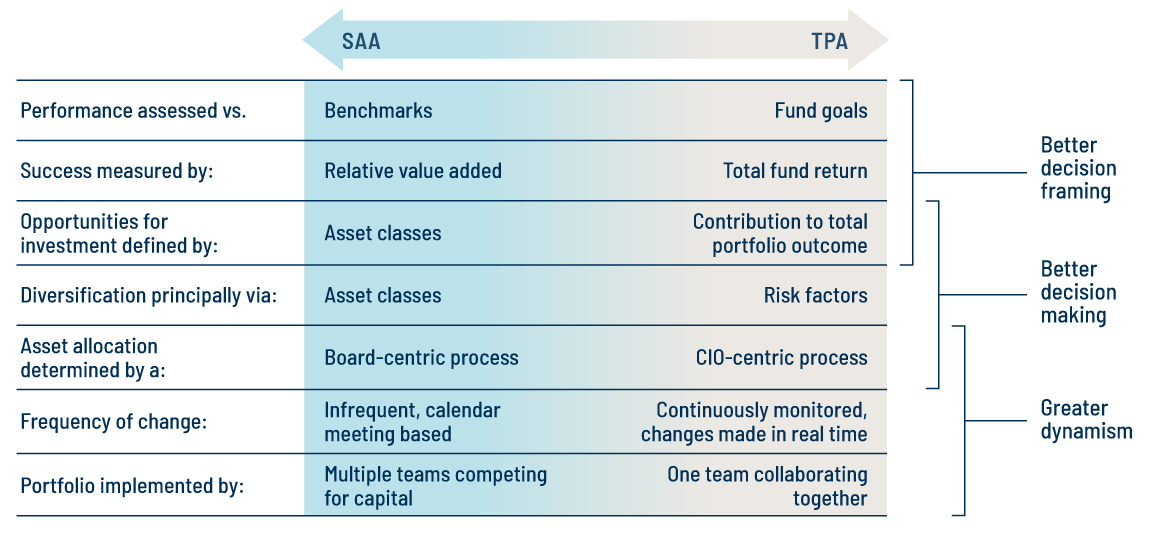

Traditionally, institutional portfolios have been managed through a Strategic Asset Allocation (SAA) framework that allocates capital across asset classes, each with its own benchmark, target allocation and investment team. TPA takes a different approach as highlighted in Exhibit 1. Rather than beginning with asset-class buckets, it evaluates opportunities based on their contribution to the portfolio as a whole, allowing investments to compete for capital across the teams and organizational structures that have traditionally managed them separately. While the discussion has been led largely by pension plans, many of the underlying questions are increasingly relevant to sovereign investors and reserve managers as they evaluate broader opportunity sets and more diverse portfolios.

It’s easy to see why the idea has gained traction. Over the past two decades, asset classes have expanded, nontraditional asset classes such as private markets have grown and specialized strategies have proliferated. Institutions have responded by building teams, benchmarks, committees and reporting structures to manage that complexity. Those changes brought expertise and broadened investment capabilities, but they also made investment decision-making more complicated.

The current market environment has made that harder. A lot of modern portfolio construction was built in an era of falling inflation, declining interest rates and relatively stable relationships between asset classes. Today, inflation has returned, rates have risen and correlations have become less predictable. Expected returns, valuations and risk premiums are also shifting faster than many governance frameworks can easily accommodate.

TPA addresses this challenge by evaluating opportunities across the entire portfolio rather than through individual asset-class silos. In many respects, the approach is less about improving investment selection and more about improving how investment decisions are made, which helps explain why discussions about TPA often focus as much on governance, delegation, accountability and incentives as they do on asset allocation.

At the same time, not every institution is equipped to adopt a full TPA framework. Many of the organizations most often cited as examples have substantial internal resources, sophisticated risk systems and governance structures built for delegated decision-making. That’s not coincidental. As portfolios grow larger and more complex, the challenge of coordinating investment decisions across multiple teams, asset classes and reporting structures grows as well. That helps explain why TPA has gained the most traction among institutions managing large, diversified portfolios.

The debate surrounding TPA will continue, and reasonable people will disagree on its merits. Not every institution needs a full TPA framework, and it’s unlikely to be the right solution in every circumstance. But the discussion reflects a broader reality. As portfolios have become larger, opportunity sets have expanded and investment teams have become more specialized; coordinating investment decisions across increasingly complex structures has become more challenging as well. The question is whether the institutions responsible for managing today’s portfolios are evolving at the same pace.