As global financial markets have expanded in breadth and sophistication, reserve management practices have likewise evolved to capture enhanced opportunities for return and portfolio diversification. Facing geopolitical uncertainty, rising inflation and rapid monetary policy shifts, reserve managers are reevaluating the traditional “safety and liquidity first” framework while safeguarding core objectives of capital preservation. Risk management and resilience now drive diversification. Gold has re-emerged as a favored diversifier and store of value—it recently surpassed the euro as the second-largest reserve asset globally—while US dollar dominance remains intact but is modestly eroding. For fixed-income investment tranches of central banks, we continue to highlight the benefits of agency mortgage-backed securities (MBS).

Agency MBS—US mortgage bonds with government backing—offer yield pick-up over US Treasuries (USTs) and have historically delivered attractive risk-adjusted returns, albeit with prepayment risk. With the current backdrop of high interest rates and low housing affordability, refinancing activity remains limited. Most US mortgages are locked in to sub-4% rates, as borrowers refinanced en masse during the Covid pandemic—particularly in 1Q21, when mortgage rates were as low as 2.25%.1 This creates a fundamental underpinning for agency MBS, with prepayment risk constrained given that prevailing mortgage rates are currently about 6.5%.1 Agency MBS represent the second largest and most transacted US fixed-income market, rivaled only by USTs, and offer the potential for attractive risk-adjusted returns without sacrificing liquidity.

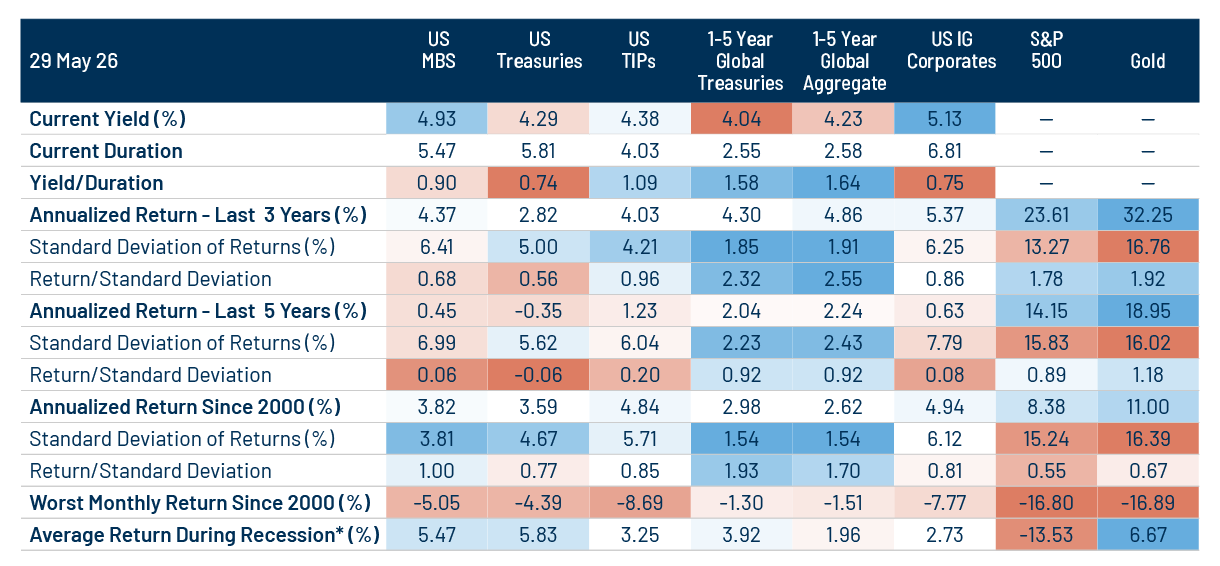

In the context of portfolio diversification, the long-term track record of US agency MBS stands out in the sandbox of fixed-income options that reserve managers and sovereign investors allocate to. Agency MBS have historically offered a high risk-adjusted return profile compared with similar high-quality fixed-income sectors, as highlighted in Exhibit 1. Key features from the historical comparison include lower volatility, better downside outcomes and a low correlation to equities and gold. Agency MBS have been less correlated with stocks than corporate bonds, offering overall portfolio diversification especially during times of market stress. Historically, the correlation of agency MBS returns is highest with USTs (83% since January 31, 2000).2 The yield advantage of agency MBS relative to USTs represents a significant source of alpha for investments of similar credit quality. The asset class outperformed USTs over longer investment horizons, a key consideration for investors looking to include agency MBS as a core allocation in their fixed-income portfolios.

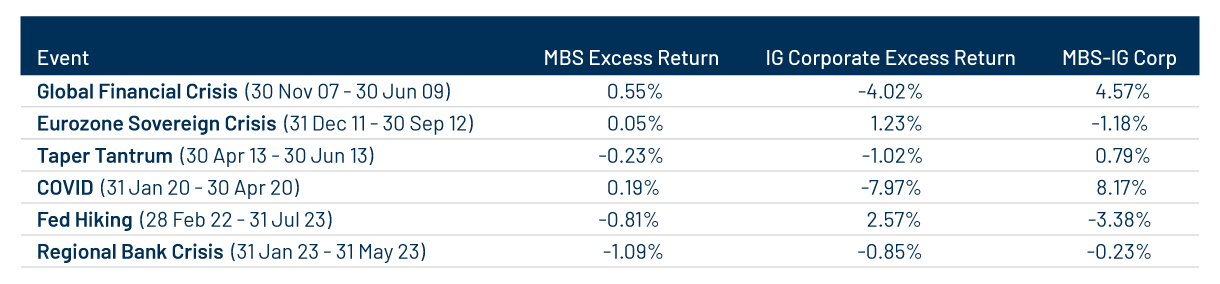

When economic growth contracts or there is stress in the market, businesses and consumers experience different outcomes when holding agency MBS compared to corporate bonds. Under the guarantee framework of the issuing agencies, delinquent mortgage loans are bought out from agency MBS securitizations, in which case the investor in that pool receives back the pro-rata principal value of the underlying loan. An early return of principal represents a prepayment at par. On the other hand, corporate credit investments can experience defaults and potential loss on principal during periods of recession. Exhibit 2 compares the excess returns of the two sectors relative to USTs, highlighting the diversification benefits of agency MBS during previous periods of stress in the market.

Seizing the opportunities in agency MBS will require active portfolio management. In practice, the Bloomberg US MBS Index itself is notoriously hard to replicate: the index comprises thousands of “cohorts” of mortgages grouped by issuer, term, vintage and coupon, which are not actually investable securities. No index fund can hold every underlying pool so tracking error is inevitable. This creates an opening for active managers to add value by carefully selecting or avoiding specific pools and subsectors rather than holding the entire index. To seek better risk-adjusted returns, specialized active managers can focus on security selection across the broader agency MBS universe, including specified pools and structured securities (i.e., collateralized mortgage obligations), as well as multifamily agency commercial MBS while managing risk relative to the benchmark.

ENDNOTES

1. Bloomberg. Optimal Blue 30-Year Conforming Fixed Rate, as of May 29, 2026.

2. Bloomberg. Monthly Index Total Returns; cumulative returns correlation of 83% since January 31, 2000, as of May 29, 2026.