Headline retail sales rose 0.5% (non-annualized) in April, on top of a +0.2% revision to the March sales estimate. We and other analysts focus on a “control” sales measure that excludes sales at gas stations, car dealers, building material stores and restaurants, partly because of the short-term volatility in these sectors and partly because these sectors sell to businesses as much as consumers, and our focus here is on consumer spending. That control measure also rose 0.5% in April, on top of a +0.4% revision to its March sales estimate.

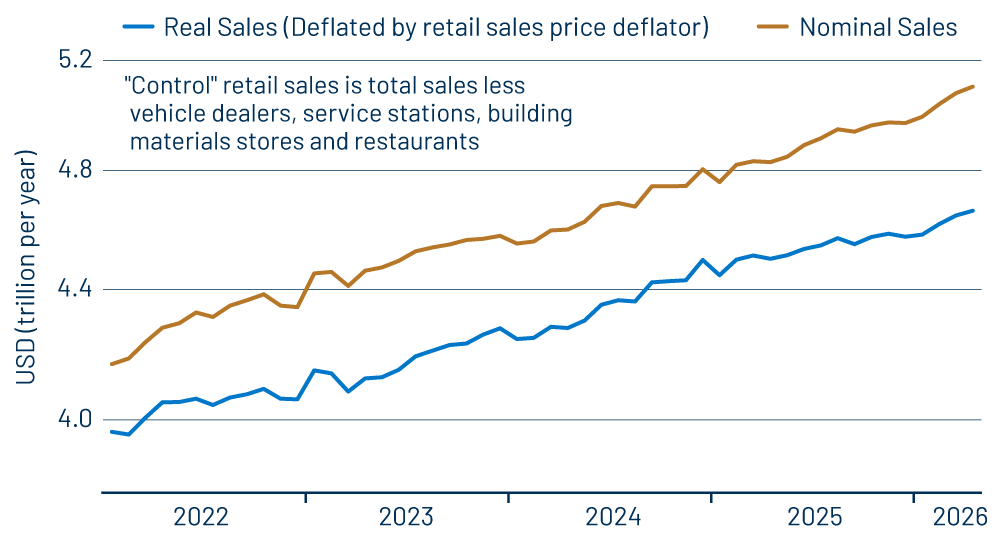

You might think that these upbeat April sales growth numbers reflect rising prices due to the Iran conflict. If so, you would be wrong. In real terms, that is, adjusting for inflation, control sales were up just as strongly as in nominal terms, as you can see in Exhibit 1.

The big increases that drove the April Consumer Price Index (CPI) measure were in fuel and, to a lesser extent, food and shelter. Again, service stations are excluded from the control sales measure, shelter prices don’t affect retail sales, and while food prices are reflected in the control sales aggregate, sales at grocery stores rose more sharply than did grocery prices.

For merchandise other than food and energy, prices were unchanged in April (actually up 0.03%), with prices declining for about as many items as those that saw rising prices. In other words, while conflict has driven up fuel prices and, apparently, food prices, there has been little or no “pass-through” as yet to prices of other items. As for the big reported increase in shelter prices, it is hard to see why global conflict should lead to rising rents.

Besides grocery stores, there were strong sales increases in April at sporting goods stores, online vendors and restaurants. (No, restaurant prices did not increase materially in April.) Sales declined only at furniture and apparel stores. The big increase in online vendor sales makes sense. With fuel costs up sharply, shoppers switched to buying goods via delivery rather than driving to the store.

The healthy sales gains reported for March and April clear up an issue we were puzzling over two months ago. As of the February data, retail sales had been softish for three straight months, and there were concerns about a weakening consumer sector. Since then, growth in both nominal and real sales has rebounded, and consumption of services has also risen respectably.

So, the apparent slowing of consumer goods spending around year-end 2025 now looks partly to have been a random swing, with real sales back on trend and nominal sales above trend. The difference between nominal and real sales reflects an increase in goods prices—an increase that predates the Iran conflict.

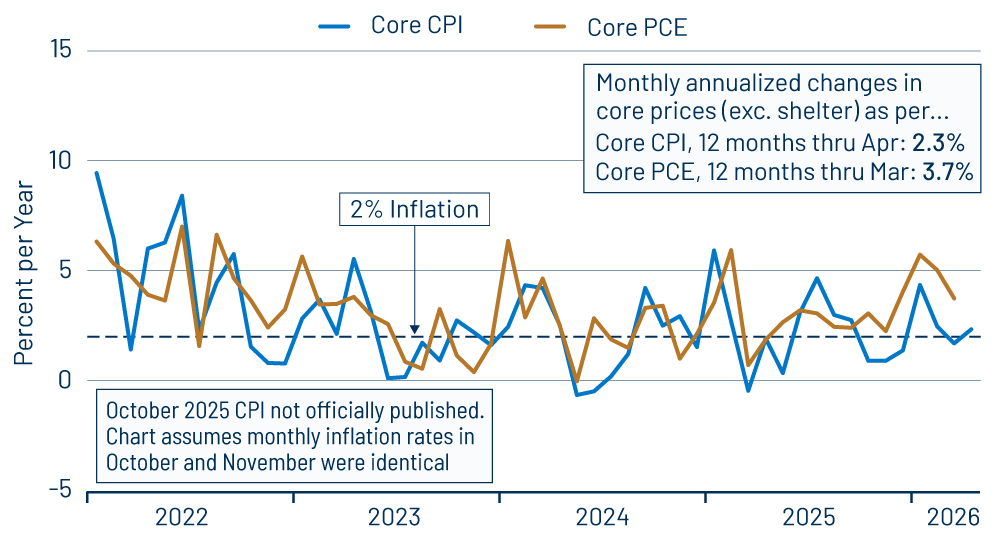

This leads into what might be the other part of the explanation for the brief slowing in real sales and real consumption. As we examined in some detail in our April 13 post, data on prices from the Labor (CPI) and Commerce (Personal Consumption Expenditures (PCE) price index) Departments show vastly different price increases for a number of specific items over December-February. The real consumer spending data contained within the GDP accounts uses PCE prices from Commerce. Given that nominal retail sales and nominal goods spending did not slow over those months, if CPI prices from Labor were used instead to produce real spending data, no slowing in 1Q would have occurred.

This is not to say that CPI data are more correct over those months than PCE data. We are merely pointing out (1) the discrepancy between the two data sets and (2) how unusual it is for them to diverge so significantly. This disparity in goods price measurements is the main factor behind the disparity in overall core inflation over December-February, as shown in Exhibit 2. (Focusing on goods prices alone, the disparity is even sharper.)

Whichever price measure was more accurate over December-February, the two inflation measures were more consonant in March and, hopefully, we will see a similar consonance in April and after. We will have to wait for data revisions down the road to get a final answer on what actually happened to inflation over the turn of the year a few months ago. For now, this doesn’t seem to be an issue for the 2Q data and after.

Rather, consumer spending is back on a decent growth track both before and after adjusting for inflation. Similarly, while the Middle East conflict is raising prices at the pump, spillover into other prices is, as yet, minimal. Through the first two months of the conflict, the US consumer sector has held up well, and the rest of the economy is doing as well or better recently than it was before the conflict.