What’s happening in the oil markets?

Geopolitical considerations have always been a part of oil market discussions. Focus on the changing world order has increased in recent times, with different theaters of conflict operating. To add another layer to an already complex analysis, the world has entered a year of elections—over 60 countries, with more than half the world’s population, are going to the polls. Higher energy prices are likely a major focus for most of these elections given the impact of increased consumer spending on gasoline and the erosion of consumers’ disposable income.

We contend that oil market fundamentals weakened at the start of 2024 relative to 2023 as supply-side dynamics, such as the return of OPEC’s role in balancing the market, have overtaken demand, warranting a more cautious approach to considering current valuations. Consequently, we believe the market is more supply-driven in this cycle and therefore prices are set to remain volatile. Forward oil prices, however, are biased downward, as evidenced by exchange-traded futures (ETF) prices.

Nonetheless, we acknowledge both the potential for price spikes if geopolitical tensions escalate as well as the prospect of supply disruptions—whether drone attacks on Russian refineries and oil infrastructure, or maritime attacks in the Red Sea (the Strait of Hormuz has been spared as of the time of writing). Any escalation in the region and subsequent broader involvement of other countries in the conflict is closely monitored for its potential to impact behavior, relations, production and exports. This adds volatility to an already tense situation; the recent tit-for-tat strikes between Iran and Israel, and potential US intervention are adding jitters. Continued supply-side restraint (namely from OPEC+), the domestic US oil industry remaining conservative in allocating capital to growing production, and a more sustained economic recovery taking hold (which would bolster demand) would also add upward pressure to prices. We contend, however, that any acceleration in demand would likely warrant a supply response, which would dampen the overall impact on prices.

What do we see as the major price catalysts this year?

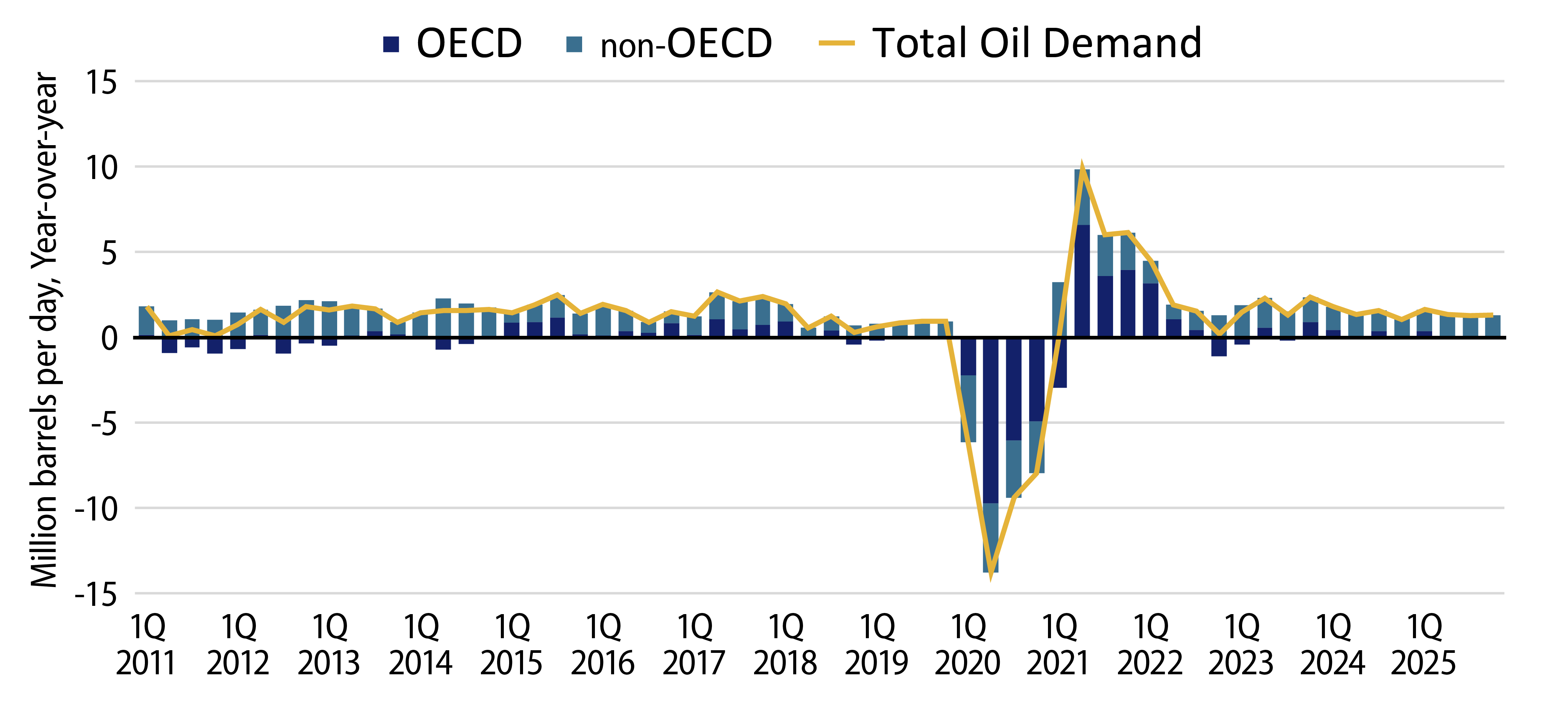

On the demand side, global oil consumption is at an all-time high, surpassing pre-Covid levels and still increasing, but at a slower rate. We observed some softness in demand at the start of this year, which is attributable to slower worldwide economic conditions and the subsequent rise in economic and geopolitical uncertainty. However, a soft-landing scenario now appears to be market consensus, partially dampening uncertainty and providing a more supportive base of demand. Pockets of demand in 2024 have arisen in petrochemicals and aviation sectors, where capacity expansions and travel have increased, respectively. Strategic petroleum reserves were in the process of being replenished or bolstered at lower prices, but now the potential for a release is evident given higher energy prices and US election timing. Higher energy prices, the continued strength of the US dollar and higher borrowing costs themselves may also lead to demand destruction.

As we look beyond 2024, electric vehicle demand growth is estimated to erode approximately 200,000 to 300,000 barrels per day of demand alongside increased focus on energy efficiency. However, offsetting this is the growth in China, India and other emerging market (EM) economies as key drivers for future demand, with increasing appetites for petrochemicals and transportation.

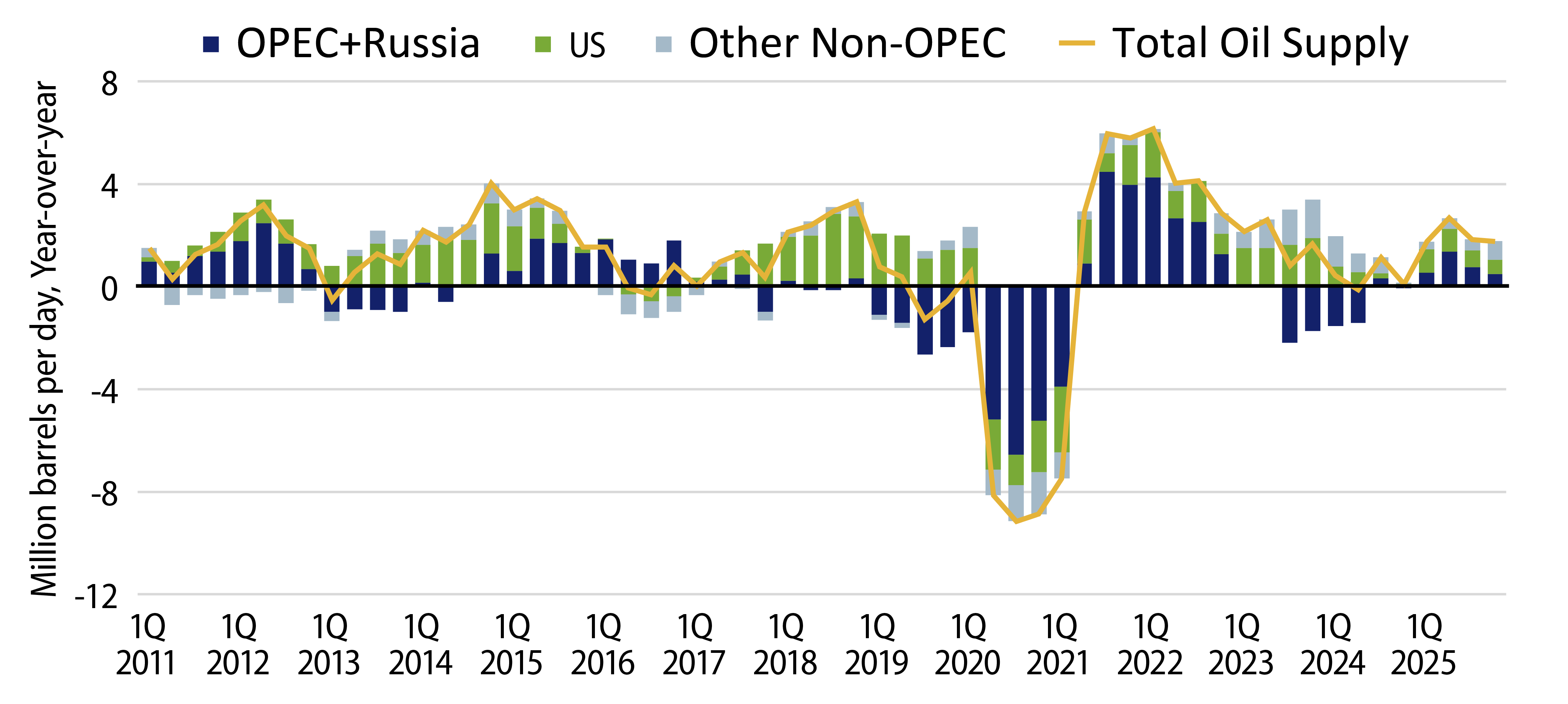

On the supply side, growth in non-OPEC supply from prior investment in large-scale, long-lived reserves in places such as Brazil, Guyana and Canada, have started to bear fruit. This is coupled with the return of US shale production; domestic oil producers have improved productivity and grown production at a lower rate than historically has been the case. Consequently, consolidation within US shale has continued to grow, protecting future drilling inventory and reducing the number of domestic players, which serves to better manage supply as a result. This has occurred while adhering to capital discipline amid current elevated market prices. Consequently, supply growth has outpaced the growth in demand. We contend that the OPEC+ alliance would need to shoulder the burden (again) to balance the market, with the responsibility falling primarily on Saudi Arabia, which would increase spare capacity and, in turn, erode its market share. All of this, however, raises the question of how long cuts will persist. Current OPEC+ actions are appearing to keep pressure on the Biden administration in the run-up to the November elections in the US. We believe the next OPEC meeting on June 1 will be closely monitored with a focus on the enforcement of voluntary cuts by members. As a result, we believe inventory builds (on crude and crude products) can be managed, but with a lower margin of safety for preserving market balance.

Where do we see value in the energy space today?

We believe the energy sector has become appealing as a “carry trade” over a “total return” opportunity. We continue to see value investing in pure commodity exposure such as exploration and production (E&P) companies and pipeline/midstream companies that facilitate moving products to market. The E&P companies benefit from current price realizations, while midstream companies are more “utility-like” in nature, with a high proportion of contracted cash flows. While many energy companies have benefited from the focus on building liquidity and repairing balance sheets, attention has turned to shareholder returns. However, the current cycle is different than many in the past, with management respecting the cyclical nature of the sector. As a result, companies are managing to lower leverage and funding shareholder returns from excess free cash flow, and not to the detriment of their balance sheets.