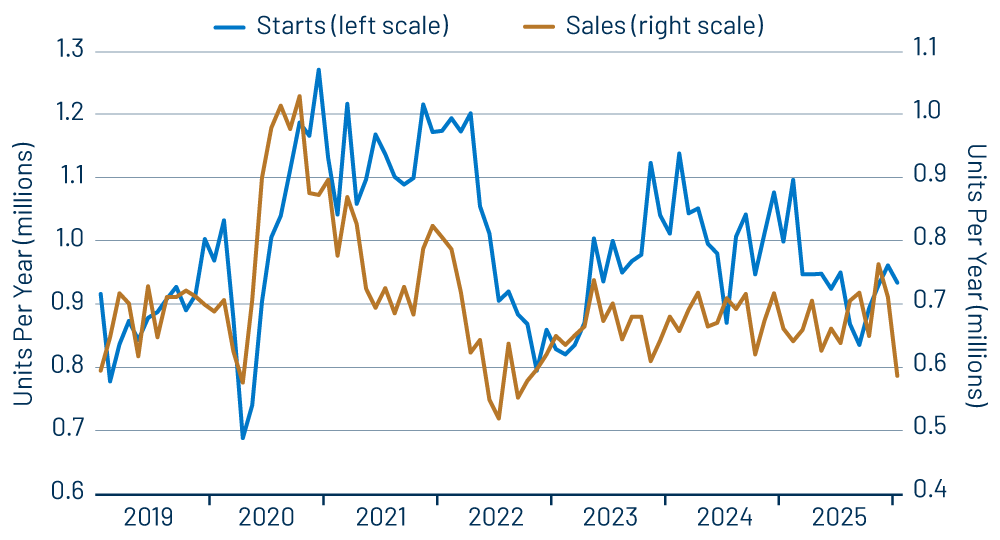

New-home sales declined -17.6% in January, while single-family housing starts dropped -2.8%. Is the new-home market collapsing? No, not at all. More likely at work are the blizzards on the East Coast that, combined with “normal” turn-of-the-year seasonal volatility, produced some wild swings in new-home market statistics, which will be worked out in coming data. Underneath all the noise, the new-home market actually looks to be stabilizing, after having contracted significantly last year.

Exhibit 1 bears out this contention. With respect to new-home sales, note that the January decline came off elevated numbers for November and December. Average sales for the three months together are 688,000 per month, right in line with prevailing sales levels for the last three years.

Given that new-home sales are especially volatile over the winter months, both the November/December jump and the January decline look to us to be statistical noise beneath a steady underlying sales pace. This makes sense especially given that the bulk of recent swings occurred in the South and Northeast, areas hit hardest by January blizzards.

Meanwhile, the January decline in single-family starts also looks like statistical noise around a steady trend. Homebuilders reduced production in the summer months of 2025 to get a better grip on inventories. Since then, amid generally stable demand, they have kept starts activity stable as well.

We hear a lot (too much?) about affordability these days. By our lights, affordability has been the major issue for housing since 2021. During the pandemic shutdown in 2020-2021, there was a flight to the exurbs, which stimulated housing demand there and pushed up home prices. Compounding the problem, Federal Reserve tightening in 2022 raised mortgage interest rates sharply, further crimping affordability.

New-home demand was quick to respond in 2021-2022 and has held remarkably steady since then. Builders were slower to react, though. They seem to have believed that the pandemic exodus to exurbs was a permanent jump in demand. With single-family starts not declining materially until mid-2022, homebuilders accumulated a huge stock of unsold production that they have been grappling with ever since.

Two to three years ago, our expectation was that housing starts would have to fall well below new-home sales levels (as per the Exhibit, that is, adjusting for the fact that owner-builds show up in starts but not in sales) in order to bring new-home inventories down to manageable levels. Starts did decline last year, but only to levels sufficient to stabilize new-home inventories rather than to cut into them.

And at present, there is little indication that builders are looking to further restrain production. Instead, they seem willing to sustain historically high inventory levels—eight to nine months of sales presently versus historical norms of around four months’ sales. One fact that may allow this is that the brunt of unsold homes today are those either not yet started or still under construction.

If inventories of unsold completed homes were to rise materially, builders would have to cut back further on starts, but, for now, new-home construction conditions look pretty stable. Again, our take is that the January new-home sales and starts data are not a threat to this generally stable condition, but merely seasonal noise that will dissipate with the onset of spring.