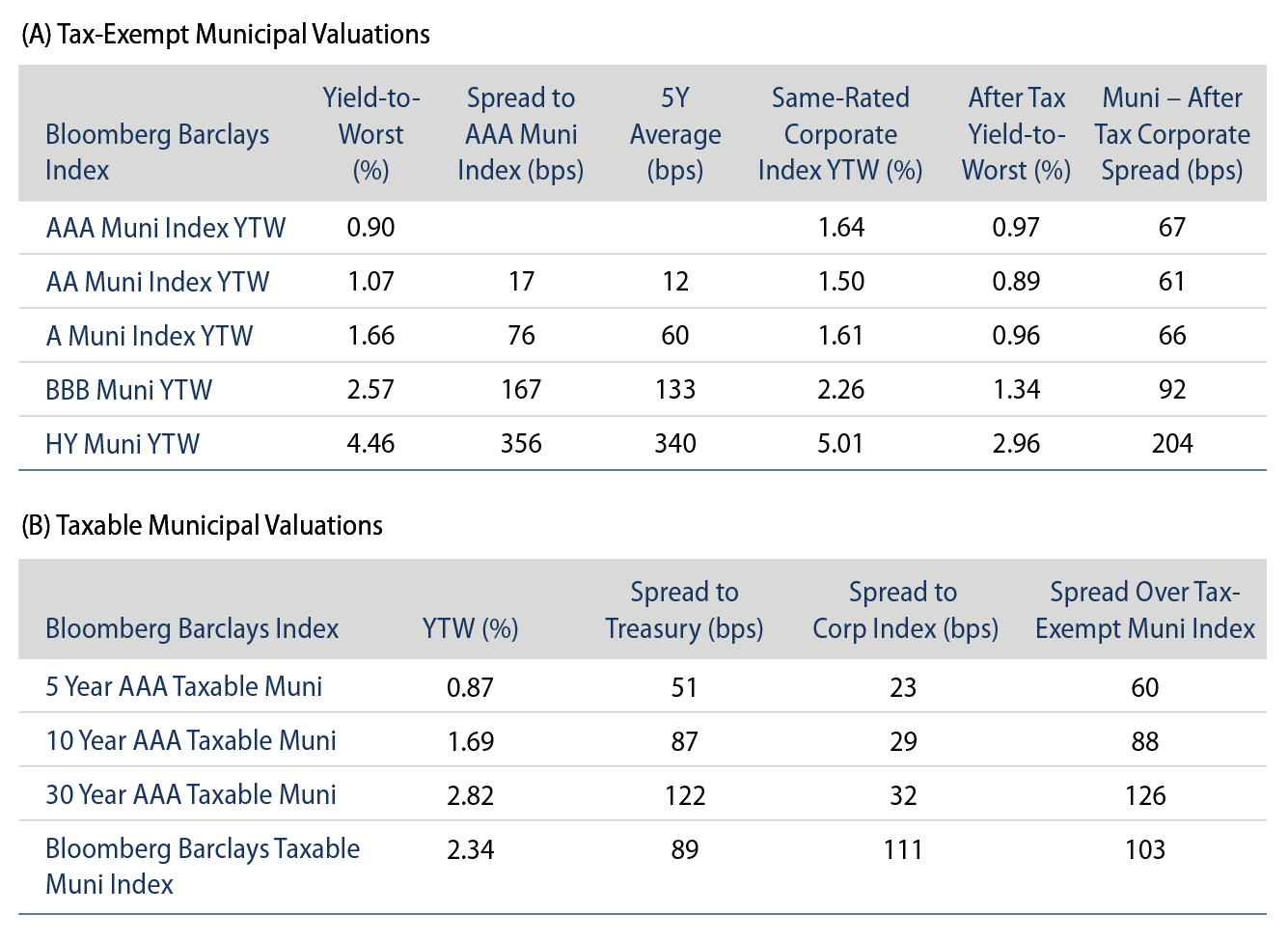

Municipals Rallied and Outperformed Treasuries

Municipals outperformed Treasuries, as Muni/Treasury ratios declined below 100% over the week. AAA municipal yields moved 3 to 15 bps lower across the curve. The Bloomberg Barclays Municipal Index returned 0.63%, while the HY Muni Index returned 0.71%. This week, we highlight election outcomes on state and local governments.

Municipal Supply and Demand Slowed During Election Week

Fund Flows: During the week ending November 4, municipal mutual funds recorded $954 million of outflows following four consecutive weeks of inflows, according to Lipper. Long-term funds recorded $888 million of outflows, intermediate funds recorded $120 million of outflows and high-yield funds recorded $260 million of outflows. Municipal mutual fund net inflows YTD total $26.3 billion.

Supply: The muni market recorded $1.4 billion of new-issue volume last week, down 92% from the prior week, attributable to the election week. Issuance of $416 billion YTD is 27% above last year’s pace, mostly driven by higher taxable issuance as tax-exempt issuance is just 2.5% above last year’s levels. Issuance is expected to remain light amid election uncertainty, with approximately $3.4 billion expected this week. Largest deals include $424 million State of Louisiana and $300 million taxable California Earthquake Authority transactions.

This Week in Munis: Election Outcomes

As highlighted in last week’s blog post, key state tax reform initiatives in Illinois and California failed to gain sufficient voter traction. However, Colorado was successful in passing proposition B. This will remove the Gallagher Amendment which has limited residential property tax collections, and we expect this will be a credit positive for local governments within the state. Elsewhere, a tax increase was passed in Arizona, increasing the state’s top marginal tax rate from 4.5% to 8.0%, which should increase the relative value of the tax-exemption of Arizona municipal debt.

Outside of tax policy, New Jersey, Arizona, Montana and South Dakota voters passed measures that will legalize the recreational use of marijuana. While the legalization of marijuana is often framed as a panacea for budget woes, incremental projected revenues typically comprise a relatively small proportion of state budgets, and we do not expect a material credit impact as a result of the legislation. S&P appears to agree, as the agency downgraded New Jersey to BBB+ from A- on Friday evening.

While the ultimate outcome of certain congressional seats remain unknown, a divided government appears a likely scenario of this election cycle. Under this scenario, we would expect more of the status quo from a tax policy standpoint rather than potential swift tax increases associated with a “Blue Wave.” Overall, we believe a divided government is neutral for municipal debt. While it may be more challenging to pass tax increases, we anticipate it would be just as difficult to overturn SALT deductibility limitations which have increased effective tax rates for wealthy earners in high-tax states.