Performance Overview

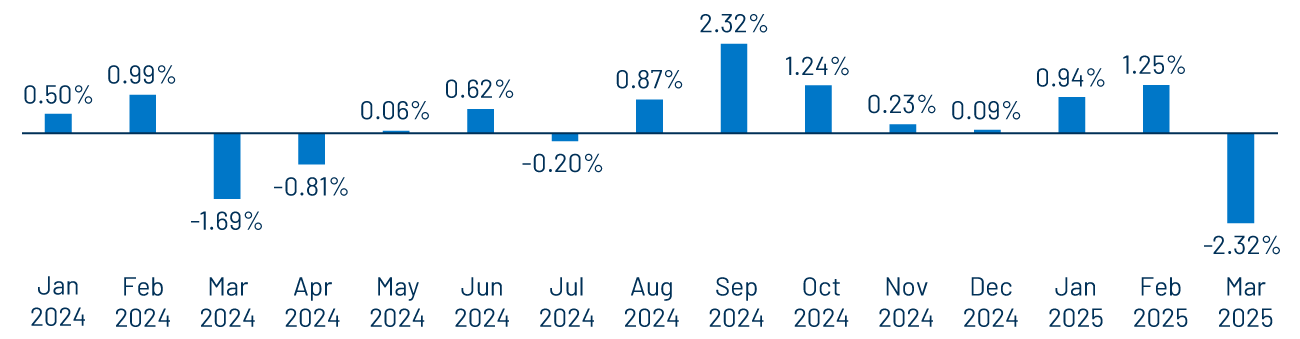

Muni returns turned sharply lower in March.

Fixed-income market sentiment was dominated by geopolitical headlines, particularly the conflict in the Middle East following disruptions to the Strait of Hormuz and rising oil prices, which contributed to renewed inflation concerns. The Federal Reserve reiterated a “wait-and-see” stance at the March Federal Open Market Committee meeting, leaving rates unchanged and projecting one additional rate cut in 2026.

Treasury yields moved higher by 18–45 basis points (bps) across the curve, while high-grade municipal yields underperformed, rising by as much as 60 bps in intermediate maturities. The Bloomberg Municipal Bond Index returned -2.32%, reversing positive year-to-date (YTD) returns to -0.18%, as seasonal technical weakness compounded broader market volatility.

Technicals

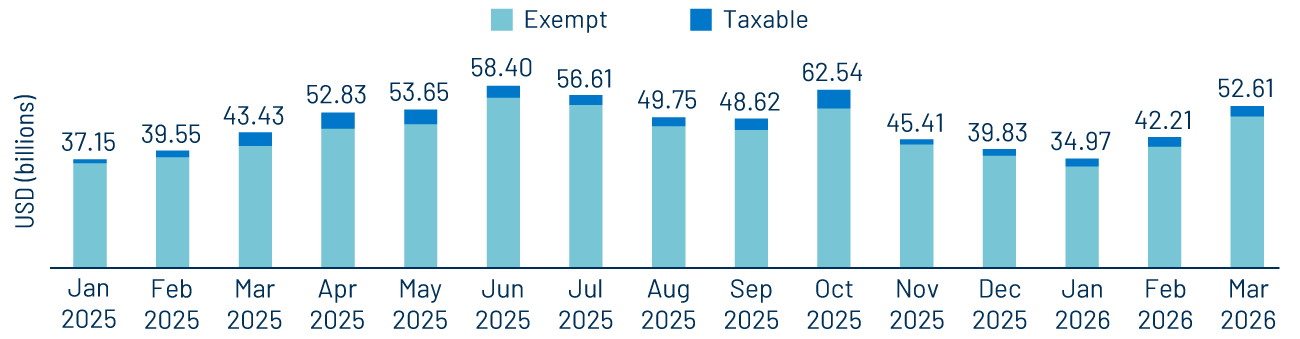

Muni supply increased to the highest levels of the year.

Municipal technicals weakened and weighed on performance during the month. Total municipal supply of $53 billion was the highest level recorded this year and the largest March supply on record. Tax-exempt issuance of $50 billion increased 23% year-over-year (YoY), also a record level, while taxable supply declined 7% YoY to $3 billion. YTD issuance of $130 billion is up 8% versus the prior record year.

From a demand perspective, municipal fund flows were resilient early in the month despite typical seasonal tax-related weakness. Following two strong months of inflows in January and February, municipal mutual funds recorded $7 billion of net inflows, according to ICI. Demand softened in the final two weeks of March amid broader market volatility and as tax day approached. Overall, demand has remained sound, with first-quarter net inflows of $28 billion, approximately half of the total flows observed in the prior calendar year.

Fundamentals

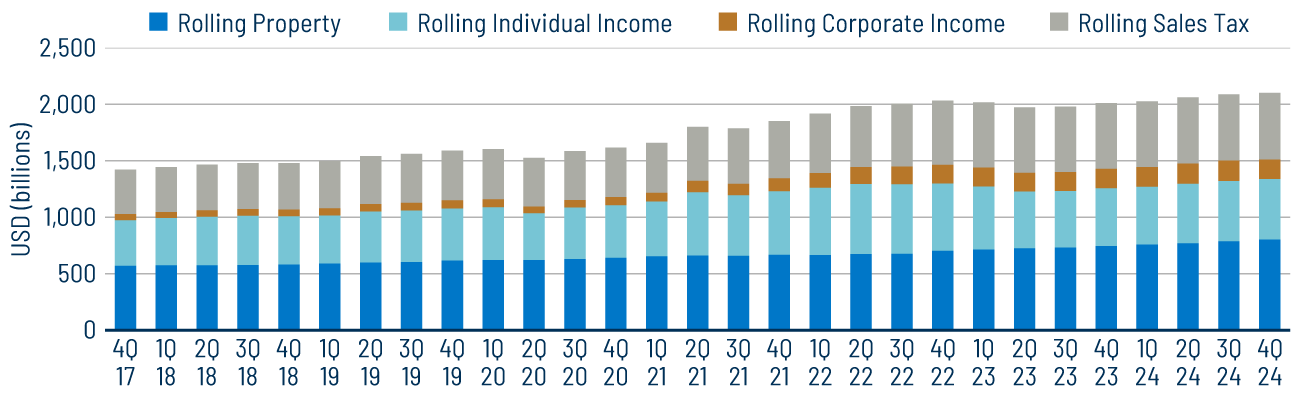

Tax revenue growth remains resilient.

Earlier in the month, the U.S. Census Bureau released its 4Q25 state and local tax collection data, effectively closing out full-year 2025 results. In the fourth quarter, total state and local tax collections reached $671 billion, representing a 6.2% YoY increase. Among major revenue sources, individual income taxes led growth, rising 10.8%, followed by corporate income taxes (+9.0%) and sales taxes (+5.7%). Property taxes, the primary revenue source for local governments, increased 4.2% YoY. The strong tax collections, building on already elevated levels, underscore the resilience of state and local credit and their capacity to manage potential budgetary pressures. As the municipal market navigates budget season, Western Asset expects these revenue trends to support overall credit stability and the historically high quality of the asset class.

Valuations

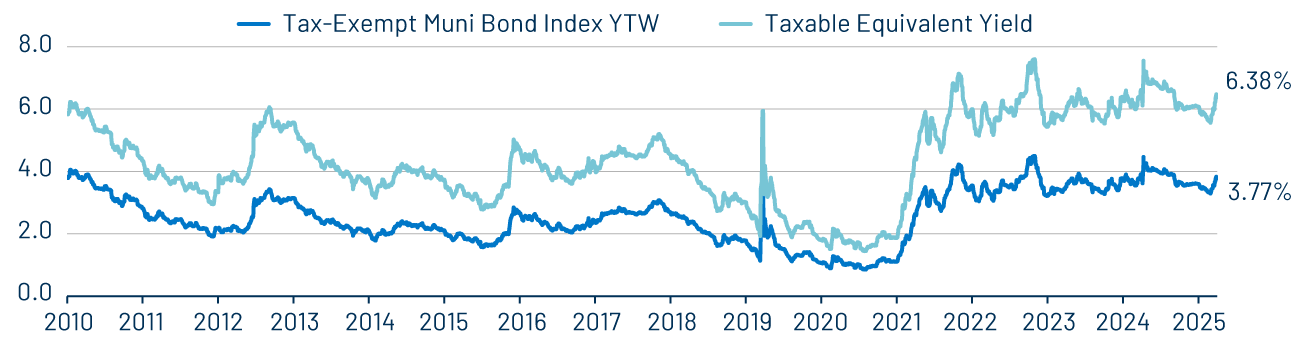

Taxable-equivalent yields jumped in March.

While periods of market volatility can contribute to short-term underperformance, they often create attractive long-term opportunities for investors to capture tax-exempt income at improved valuations. The Bloomberg Municipal Bond Index yield-to-worst increased to 3.77% (6.37% taxable-equivalent yield), up from February lows of 3.29% (5.56% taxable-equivalent yield). Notably, the 5- to 14-year segment of the curve experienced the largest increase in yields of over 50 bps, providing improved relative value, particularly for SMA strategies that had faced valuation challenges through much of the past year.