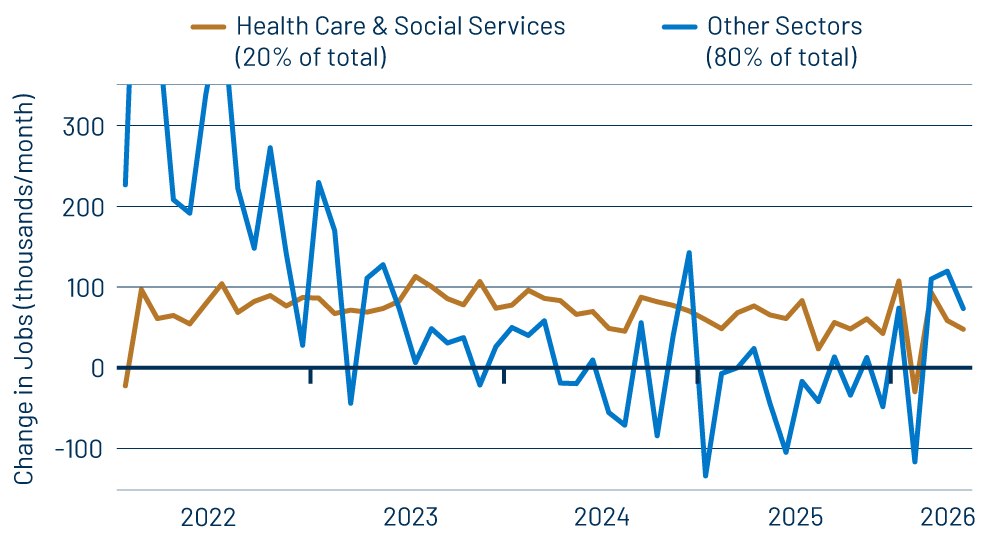

Data released today by the Bureau of Labor Statistics (BLS) showed private-sector payroll jobs rising by 120,000 in May, on top of a large, +56,000 revision to the April jobs estimate. Workweeks held generally steady and hourly wages rose only modestly. What’s more, there was better overall balance in the report, with health care and social assistance providing only about a third of the overall increase, whereas these two government-oriented private sectors provided the bulk of overall job growth through most of 2025. You can see this recent swing very clearly in Exhibit 1.

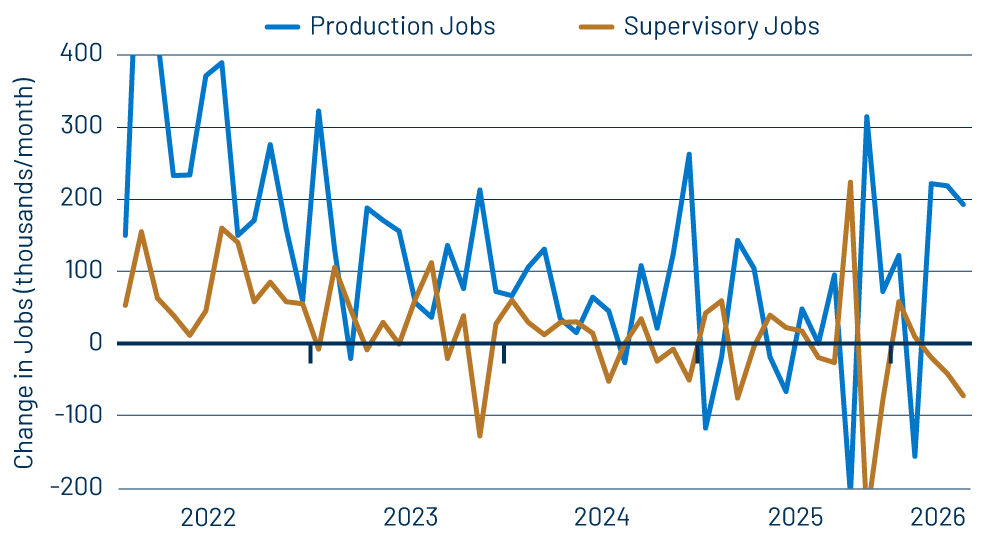

Another favorable feature of today’s report was that production jobs rose even more strongly than overall jobs, with private-sector production jobs up +190,000, on top of a +63,000 revision to April, compared to the aforementioned +120,000 and +56,000 changes for total private-sector jobs. In other words, employers have focused on hiring line workers, even cutting back mildly on administrative staff.

This trend began in late-2024 and has intensified in recent months, as you can detect from Exhibit 2. The combination of production-focused employment growth and modest wage growth (within Federal Reserve [Fed] target rates) augurs well for sustained non-inflationary growth, if and when energy prices start to come back in line.

There were some oddities in the report which cause us to add some caution to the favorable assessment. That is, most of the recent pickups both in overall job growth and in production job growth occurred in just one sector: restaurants & bars. Elsewhere, job gains have picked up recently, but not nearly as impressively as when the restaurant gains are included.

In and of itself, there is nothing wrong with strong growth in restaurant jobs. The problems are that first restaurant sales and spending have shown no recent pickup that would justify a strong rebound in employment there, and second, again, the recent jobs picture is less robust elsewhere.

Bond markets reacted negatively to today’s news, as apparently the robust overall job gains fueled fears of Fed tightening. However, we believe such fears are misplaced. Even taking the job gains at face value, the facts remain that job gains are relatively narrowly focused and, more importantly, wage gains remain restrained, within target, while unemployment has actually ticked up over the past two years. The Fed desires stable, non-inflationary employment growth. Even at face value, recent payroll data are the poster child for such conditions. And, once the possible flukes in recent restaurant-sector data are factored in, there is even less reason to think the Fed is contemplating a tightening.