Private-sector payrolls rose by 123,000 in April, with only a slight -15,000 revision to March estimates, according to data released today by the Labor Department. Average workweeks increased, while average hourly earnings rose at just a 1.9% monthly annualized rate. These data show job growth substantial enough to quash any recession fears out there, while wage growth is at rates that won’t raise any inflation hackles. In other words, today’s data should be encouraging to stock and bond markets alike.

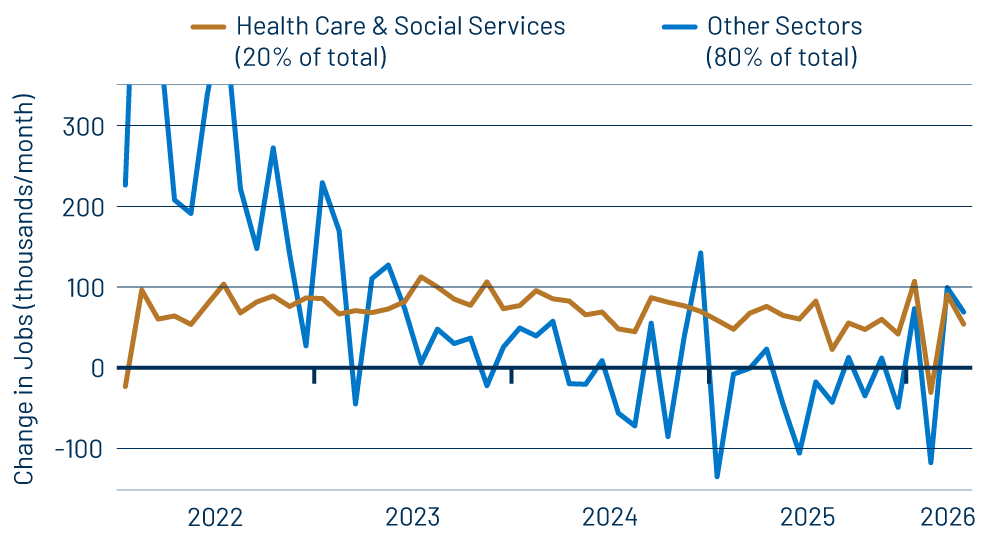

No, the report wasn’t a perfect testament to the economy. Health care and social assistance continue to account for a large share of the reported job growth, as shown in Exhibit 1, and the bulk of the gains elsewhere came from a handful of sectors: building material stores, big-box retailers, courier and messenger services, professional services, entertainment and restaurants.

The fact remains, however, that the overall performance of the non-health-care economy has been markedly better so far this year than what we saw in 2024 and 2025, this despite a prolonged government shutdown and the outbreak of hostilities with Iran. Similarly, it is encouraging to see the bounces in job growth reported for the sectors listed here, as these had been languishing over the preceding two years.

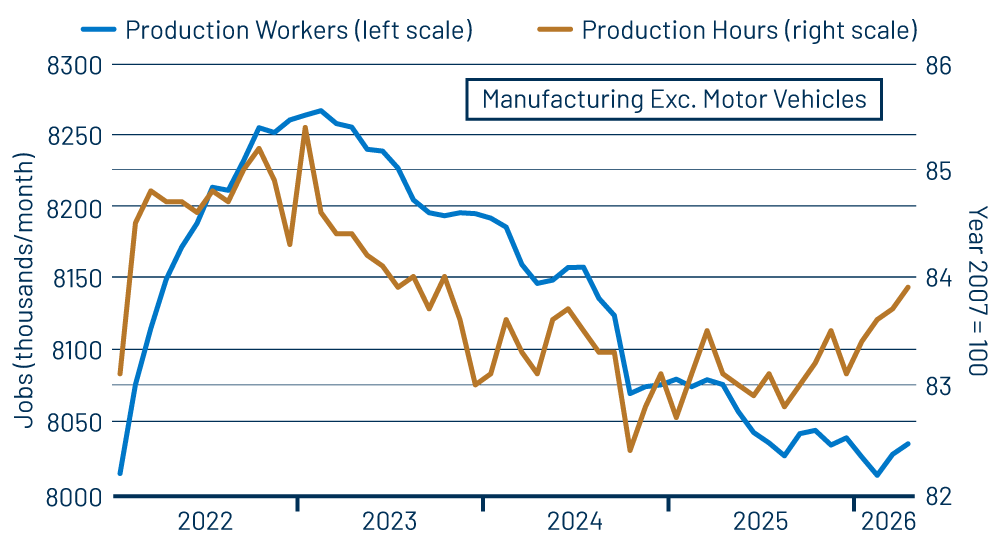

Furthermore, the underlying details of the report were also favorable, as private-sector production jobs rose even more strongly, by 154,000. In other words, employers are trimming administrative staff, even while adding line-worker jobs, which augurs well for production growth going forward. This trend has been in evidence since last summer.

The increase in average hourly wages was especially small in April. However, it is also the case that average wages have been moderating for quite some time. Over the last six months, average hourly wages have risen at an annualized rate of just over 3%. We estimate that a rate of 3.5% or less is consistent with the 2.0% inflation target of the Federal Reserve (Fed). So, inflation above 2% recently and in months to come will likely be due to the effects of tariffs and military conflict, not generated from within the domestic economy. In other words, there is nothing in the labor market trends to trouble the Fed.

In past posts, we have mentioned a rebound in manufacturing activity occurring since late 2024, spurred in part by strong growth in business capital spending. This burst has so far not generated a huge number of jobs, but it has arrested the preceding downward trend in factory jobs, and it has also led to increased work hours on factory production lines. Both these swings are on display in Exhibit 2.

The CAPEX boom and factory revival have been credited to AI and the construction of data centers. This has surely been a significant factor behind the rebounds. However, we are also seeing production of textile products, metals, metal products, industrial machinery and electrical equipment, as well as high-tech equipment. So, the manufacturing rebound is well spread out, not confined to high-tech.

Finally, while the establishment survey data (payroll jobs) show improvement over recent months, household survey data have moved in the other direction. No, the unemployment rate has not risen, but the civilian labor force and civilian employment have both been declining since December. This is exactly the same period over which payroll job growth has been improving. Employment data from the two surveys often move disparately, and when that occurs, we are inclined to pay more attention to the payroll data (which is why these posts focus almost exclusively on payroll jobs).

So, while household survey (civilian) employment has softened recently, that has not led to any increase in the unemployment rate (which is what the household survey is constructed to cover), and, meanwhile, establishment survey (payroll) data show a modest but noticeable improvement in recent months, without generating any inflationary pressures. Goldilocks indeed!