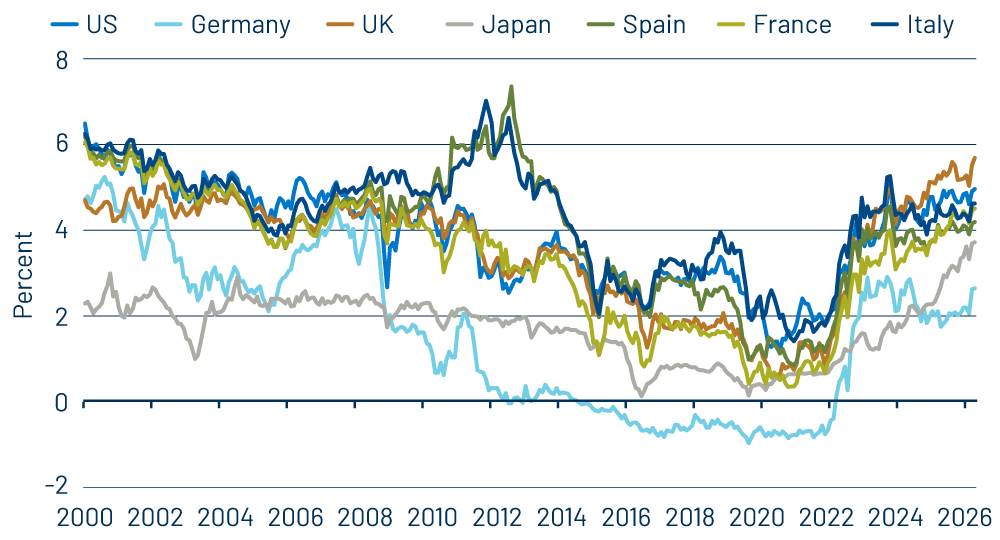

Developed-market (DM) bond markets are sending a message that investors can no longer afford to ignore. What began as a higher-for-longer rate adjustment has evolved into something much broader: a repricing of inflation risk, fiscal credibility and geopolitical uncertainty. Across the US, Europe, the UK, Australia and Japan, long-term yields have continued pushing higher as markets increasingly question whether central banks can ease policy as aggressively as once expected while governments continue running large deficits amid energy shocks, heavier debt issuance and persistent inflation pressure.

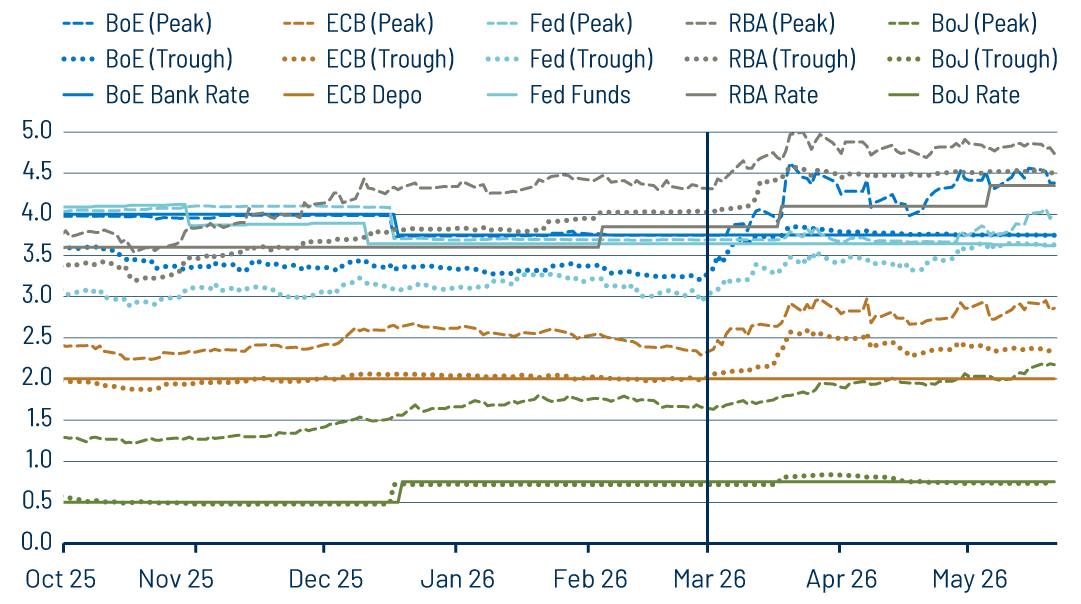

One way to track this shift is through how rate expectations have evolved over the past several months. Western Asset has long monitored what markets price for anticipated “peaks” during central bank hiking cycles and “troughs” for eventual easing cycles. Using money market futures roughly two to two-and-a-half years forward, this framework helps illustrate how market-implied policy expectations evolve alongside incoming data and geopolitical developments.

Across markets, the most abrupt shift came after the US-led strikes on Iran at the end of February. Economic data still mattered, but the geopolitical shock quickly became the dominant driver for rates markets through the inflation and energy channels.

In the US, prior to the war in Iran, markets were pricing for a continuation of the Federal Reserve’s (Fed) cutting cycle that would’ve pushed policy rates closer to 3% by the end of 2026. The repricing in the US has been slower, partly because the economy is less directly exposed to imported energy shocks and partly because investors still believed that slowing growth, a fragile labor market and a change in Fed leadership would set a high bar for hiking rates. Over the past several weeks, however, even US markets have shifted away from rate cuts and toward the possibility that rates may need to remain elevated for longer, as market pricing begins to factor in potential hikes. In our view, the speed and magnitude of the repricing suggest rate expectations may now be running ahead of underlying growth and inflation fundamentals.

In Europe, markets late last year were still debating whether the European Central Bank (ECB) might eventually need to hike modestly from its 2% policy rate, and whether that meant one or perhaps two hikes. Today, markets are pricing something materially different, with expectations now implying roughly four hikes and policy rates moving closer to 3%. We see the ECB taking a patient and data-dependent approach. European GDP growth has remained steady, if unspectacular, and we expect that trend to continue this year. That said, geopolitical risks remain elevated, with Europe particularly vulnerable to higher energy import costs that could pressure consumer spending and corporate margins. The impact of German fiscal expansion will also be closely monitored, particularly given lingering wage pressures and the potential inflation implications.

The UK has seen an even sharper repricing. Earlier in the cycle, markets viewed the Bank of England as nearing the end of its easing campaign, with perhaps two cuts remaining as inflation gradually moved toward target and labor-market conditions softened. That changed quickly after the Iran strikes. During the height of the March tensions, markets briefly shifted toward pricing three to four hikes instead. Even after some moderation in energy prices, markets continue to price roughly three hikes from current levels. Our view is that UK gilts remain attractive around the 5-year sector, although risks tied to Iran, domestic politics and fiscal policy argue for appropriately sized positions given the unusually high degree of uncertainty.

In Australia, the Reserve Bank of Australia (RBA) was already tightening policy prior to the war in Iran due to broader inflation concerns. Following its third consecutive hike earlier this month, effectively reversing all of the cuts delivered in 2025, the RBA adopted a more patient tone while monitoring incoming data and financial conditions. Policymakers acknowledged that additional hikes would do little to alter the near-term trajectory of inflation and suggested policy settings are now somewhat restrictive. Markets responded by slightly lowering expectations for the peak RBA policy rate even as policy expectations elsewhere continued moving higher. That dynamic has helped Australian government bonds outperform many of their DM peers.

Japan presents almost the opposite case. Ahead of the Bank of Japan’s (BoJ) April meeting, markets had assigned a high probability to another rate hike. Instead, the BoJ stepped back from tightening, reinforcing the perception that it remains behind the curve relative to inflation pressures. Markets have continued lifting expectations for the eventual peak in Japanese policy rates while Japanese government bonds have simultaneously had to absorb concerns around supplementary fiscal spending and additional debt issuance. In our view, the Japanese economy should continue growing, while expansionary fiscal policy, including consumption tax cut discussions and rising defense spending, is likely to place additional upward pressure on yields, particularly at the longer end of the curve. As such, we expect further curve steepening ahead.

The key takeaway is that this repricing of government bond yields is no longer just a US or UK story. Investors interested in DM countries are increasingly demanding compensation for inflation uncertainty, fiscal deterioration, heavier sovereign issuance and geopolitical risk. Higher yields alone also no longer appear sufficient to quickly restore equilibrium, particularly when fiscal deficits, energy shocks and inflation volatility remain unresolved.

At the same time, the traditional relationship between bonds and risk assets has become less predictable in an environment shaped by supply-side inflation shocks and geopolitical fragmentation. Higher starting yields certainly improve the income opportunity in fixed-income relative to the post-Global Financial Crisis period, but duration is no longer viewed as a clean hedge when volatility is being driven by inflation and government borrowing needs rather than growth concerns alone.