Private-sector payroll jobs declined by -86,000 in February, according to data released this morning by the Bureau of Labor Statistics (BLS), within the Labor Department. Furthermore, there were -69,000 of downward revisions to previous months’ private payroll data, mostly a sharp downward revision of December job growth.

Did the labor market suddenly weaken dramatically in February, or were other factors at work? Recall that a month ago, we were skeptical about the supposedly strong January report. We think the softer data today are mostly an offset/reversal of “overstated” gains in January. In addition, a strike in the health care industry served to substantially depress jobs there. Finally, data around this time of the year are always subject to winter weather distortions, and the severe blizzards across the eastern US likely suppressed February jobs data.

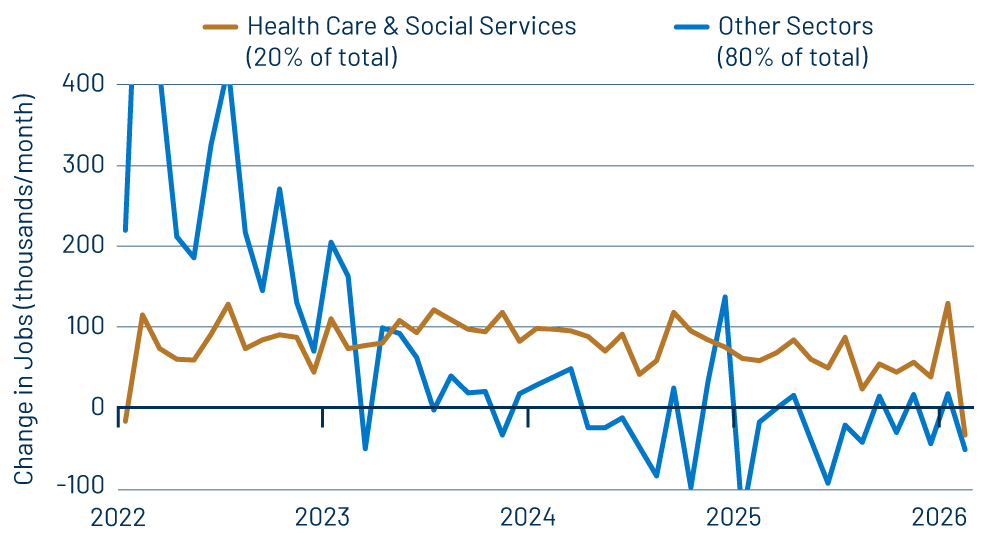

Exhibit 1 goes a long way toward making our points. Note first the wild swings in job growth within health care and social assistance, the brown line in the chart, with a large, +129,000 job gain in January and then a -34,000 decline in February. Combine the two months together, and you get a +43,000 jobs per month average, right in line with what that industry had been doing over the previous four months.

Then, fold in the fact that this sector experienced a labor strike in February. You start to get the picture that health care employers likely added on extra help in January, in anticipation of a strike, and then indeed saw the strike occur in February. It is likely that with the strike now over, March jobs for this sector will revert to their previous growth trend, leaving the January/February swings as statistical noise.

Unfortunately, as we have remarked before, there is no real job growth going on outside health care and assistance, and there has not been for three years now. For the rest of the economy, denoted by the blue line in the chart, December job growth was revised from +11,000 to -45,000, and January growth from +35,000 to +17,000, followed by a -52,000 decline in February. In effect, the previously announced “strength” in December/January was revised away.

That -52,000 February decline in private sector ex health care jobs was in line with the range of month-to-month swings over recent experience. The job losses occurred mainly in construction (-11,000), couriers and messengers (-17,000), motion pictures and sound recording (-10,000), building services (-11,000) and restaurants (-30,000). For motion pictures and building services, the February declines merely erased especially large January gains. The construction and restaurant declines came out of the blue and likely reflect bad weather. The courier declines are merely a continuation of a declining trend that has been in place for the last four years.

No, these considerations do not turn a soft jobs report into a strong one, but neither is the sky falling. Again, we were skeptical of the supposed strength in the January report, and we think the February report is mostly comeuppance (comedownance?) for January. It continues to be the case that outside of health care and social work, job growth is essentially nonexistent. That pattern is not new, but has been the case for almost three years now.

Meanwhile, despite non-growth in jobs, the economy in general has indeed improved recently. Manufacturing output has picked up, service-sector output growth is steady and today’s retail sales report shows an improvement from the last few months’ experience. We’ll cover the retail sales data in our next post, when we discuss consumer spending in general.