Emerging markets (EM) have benefited from a meaningful shift in sentiment over recent weeks. The dominant macro catalyst has been the prospect of a US-Iran peace agreement and the expected reopening of the Strait of Hormuz. Oil prices have retraced more than 30% from their wartime peak. At the same time, US equities and credit spreads have largely priced in a favorable geopolitical outcome.

For EM investors, the peace dividend is clearly positive. Lower oil prices reduce pressure on current accounts, fiscal subsidies and consumer purchasing power across many oil-importing economies. They also ease some of the immediate pressure on central banks that had been forced to respond to the inflationary consequences of higher energy prices. The risk rally has been particularly helpful for high-yield and frontier market sovereigns, where spreads had widened during the earlier phase of the conflict.

That said, one should be careful about extrapolating the market reaction too far. There is an important distinction between a financial market repricing and a real economy normalization. Markets can quickly discount a peace agreement, but physical trade flows, inventories and supply chains take longer to repair. A reopening of the Strait of Hormuz would be a major step forward, but shipping companies, insurers and commodity traders are unlikely to immediately return to pre-conflict operating behavior. Energy inventories also need time to rebuild, and disrupted regional infrastructure, including gas-related facilities, may take time to fully recover. That matters most for inflation.

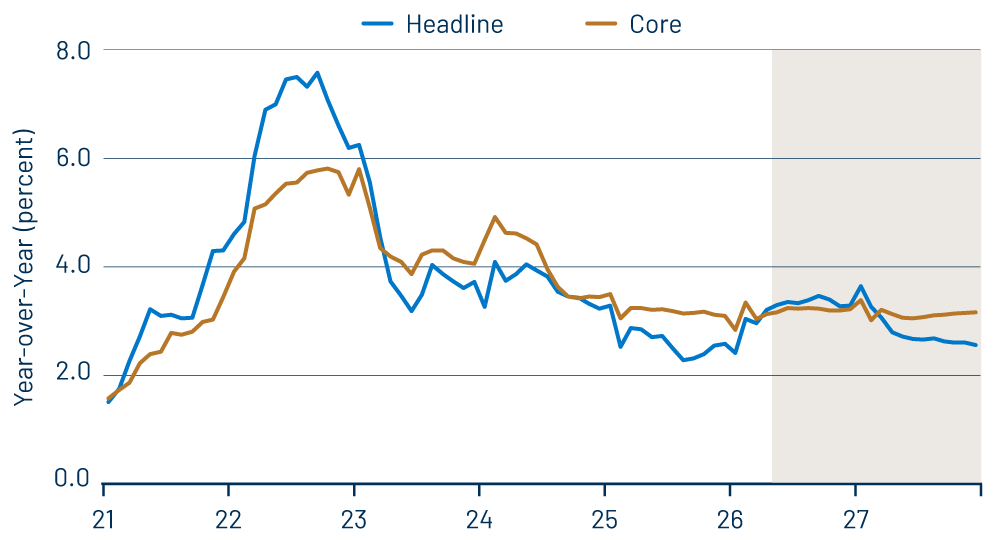

Spot oil prices have fallen, but the earlier shock has not yet fully passed through the data. Higher freight costs, disrupted shipping patterns, lower inventories and prior fuel-price increases are still likely to affect consumer prices with a lag. The impact will vary by country, but oil-importing EM regions in Asia and parts of Europe remain particularly exposed. Food, transport, electricity and administered prices often adjust gradually, and governments may also need to recalibrate subsidies or regulated prices after the fact.

As a result, we do not think we are yet at a clean disinflation inflection point. Our base case is that inflation data in several EM regions may continue to move higher over the next three to six months before stabilizing. More favorable base effects should eventually help the disinflation process, but that is more likely to become visible next year than immediately.

Rates markets are already reflecting this tension. US Treasury yields remain elevated despite stronger risk sentiment, partly because markets are still focused on fiscal concerns, supply and sticky inflation. Across various EM regions, local rates have repriced higher as central banks account for higher expected inflation and, in some cases, the need to defend currencies. Several EM central banks have adopted a more hawkish tone, and some have already tightened policy to preserve credibility.

For hard-currency EM debt, valuations are no longer as compelling as they were earlier in the shock. Spreads have tightened, frontier market bonds have performed well and the market overall has already priced a meaningful improvement in the geopolitical backdrop. The EM asset class still offers attractive carry, but future returns are likely to depend more on security selection and country fundamentals than broad beta.

Local markets may offer a more balanced opportunity set. We expect EM currencies to remain broadly range-bound versus the US dollar rather than enter a sustained appreciation trend. The dollar has not broken decisively lower, and US rates remain a constraint. However, many EM regions still offer attractive nominal and real yields. If volatility continues to decline and geopolitical risk recedes, carry trades should return to the forefront.

Overall, our view is that the backdrop for EM is constructive, but not without risk. The sector has strong technical support from limited issuance and continued inflows, while lower oil prices reduce an important macro headwind. But the market may be moving faster than the real economy. Until inflation data confirms a turn and trade flows normalize more fully, we would favor carry, selectivity and countries with credible policy frameworks over simply chasing the relief rally.