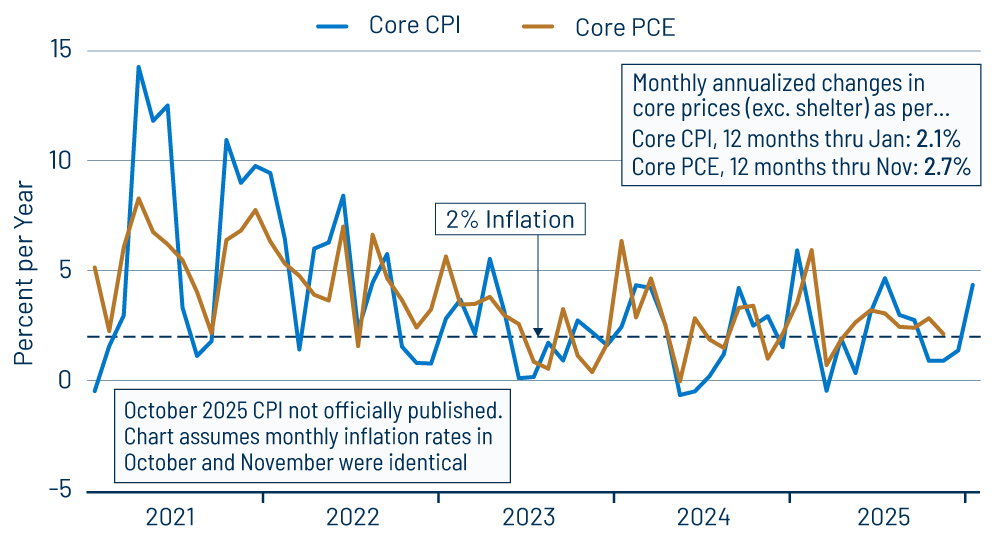

The Bureau of Labor Statistics (BLS) announced today that Consumer Price Index (CPI) inflation occurred at a 2.1% seasonally adjusted annualized rate in January. However, the more closely watched core CPI bounced to a 3.6% annualized rate in January and a 2.5% rate for the last 12 months. (Core inflation excludes the volatile food and energy components.)

Because of likely technical glitches in reporting of shelter costs, we have been focusing on a core inflation measure that also excludes shelter costs. That measure rose at a 4.4% annualized rate in January and by 2.1% over the last 12 months. (Shelter costs have recently come in more closely aligned with market data on home prices and rents, after diverging widely in 2022 and 2023, so we will likely focus primarily on overall core inflation in months to come.)

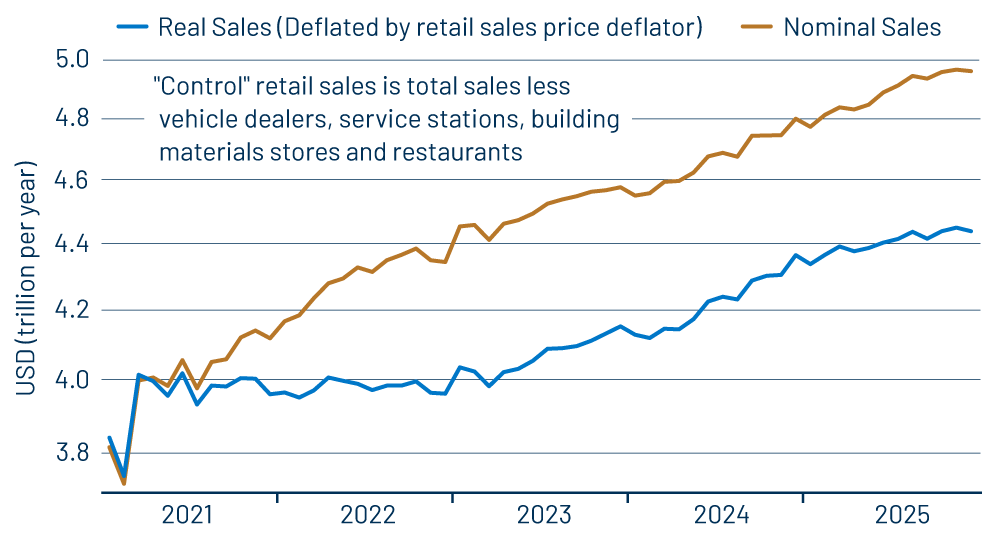

Meanwhile, earlier this week, the Census Bureau announced that retail sales were essentially unchanged in December from November, for both the headline and control sales measures. (“Control sales” excludes the volatile and business-oriented car dealer, service station, building supplies and restaurant sectors.)

Financial analysts had widely anticipated some bounce in CPI inflation in January, and the actual increase may have been smaller than expected. As you can see in Exhibit 1, core CPI also bounced in January 2025, 12 months ago, only to subside thereafter. CPI inflation will also likely subside in the months to come, but note that the January 2025 spike eased, but did not reverse. In other words, the January 2025 spike continued to hold up 12-month inflation rates over the rest of the year, and the same is likely to occur this year. So the successive January spikes should be put in perspective, but not dismissed outright.

In January, goods prices were generally well-behaved, with core goods prices essentially flat (up at a 0.5% annualized rate), food prices up only slightly (2.2% annualized), and energy prices down substantially (-16.2% annualized). However, core prices were elevated by a spike in service costs, with non-energy services up at a 4.8% annualized rate and ex-shelter services (aka ''supercore'') up 7.3% annualized.

Yes, services prices also spiked in January 2025, and much the same ''culprits'' drove the gains in both this January and last January. These sectors were utilities, hospital and doctor fees, car rental costs, sporting event prices and internet fees. For January 2026, airline fares also jumped sharply. Also this month, though, health insurance costs were reported as declining, and a few other service sectors came in milder than a year ago, so that the January 2026 services inflation spike was actually a bit milder than that of January 2025. Here too, these January price spikes will ease in the months to come, but they will keep 12-month inflation rates elevated.

All in all, the January 2026 CPI report is not good news. It is possible/likely that technical factors contributed to the spike, but that just puts the onus on the inflation data in February and beyond to come in more moderately.

The soft December retail sales report came on the heels of a downbeat November sales report as well. We saw a similar late-summer “lull” in sales activity, only to see a strong rebound in October. A similar rebound is likely in early-2026, given that personal income gains have been healthy. Also, as we have discussed before, Christmas season sales data are especially hard to seasonally adjust, and that might be an issue with the December data. On the other side of the ledger, especially cold winters have restrained January sales in years past, and extremely cold and snowy recent weather in the eastern US could work to restrain early-2026 sales.

In sum, there are a lot of factors in play in the retail sales data for the time being, and it could be a while before we get a clear picture on things. There is no reason to expect emerging weakness, but, for now, the soft sales reports over the last two months are cause for concern.

For what it is worth, the softer sales were focused at furniture stores, online retailers, drug stores and, to a lesser extent, grocery stores and restaurants. No sector showed particularly strong sales in November/December.

The fact that we are discussing January CPI inflation and December retail sales likely reminded you of our remark last time that the Census Bureau is about a month behind the BLS in catching up its releases from the effects of the shutdown. To catch up, Census will have to report two months’ worth of sales (and other indicators) in a single month. No word yet from them on when that might occur.