Real consumer spending rose 0.3% in May, or at a 3.2% annualized rate, which is a bit stronger of a pace than we had been seeing in previous months. Within the May details, spending on both basic goods and basic services rose nicely. However, there were very sharp downward revisions to previous months’ spending data all the way back to January.

This is odd in that, typically, spending data see little revision more than two months back, in this case back to March. Instead, again, the data were revised substantially all the way back to January. Similarly odd was the composition of those revisions. In preceding posts, we have been spending a lot of time talking about an apparent slowing in spending on goods, while services spending was holding up okay. Well, goods spending was actually revised up for March and April. It was services spending that saw all the big downward revisions back to January. (We’ll get into the details of the services downgrade shortly.)

So, with consumer spending revised down big-time all the way back to January, 1Q GDP was also revised lower, right? Wrong. Annualized 1Q real GDP growth was actually revised substantially higher, from 1.6% to 2.1%. Yes, 1Q real consumer spending was indeed revised substantially lower, from 1.4% to 0.5% growth. However, 1Q imports of merchandise were sharply lower, from 25.5% to 16.6% annualized growth, and since imports enter GDP negatively, that accounted for more than all of the upward lift to 1Q growth.

We hate to sound like a “two-handed” economist, but there are two conflicting aspects to this story. On the one hand, it is really odd to see such downward revisions to imports of merchandise at the same time there were (modest) upward revisions to consumer spending on merchandise. Both revisions served to boost estimated growth in domestic output of merchandise. (Higher domestic spending on goods obviously works to boost domestic output, and if the goods didn’t come from imports, they must have come from domestic production.)

And this is the “other hand” of the story. When preliminary 1Q GDP data were first announced two months ago, we pointed out that those data showed weak growth in domestic goods output, even while Federal Reserve data on industrial production were showing relatively strong 1Q growth in manufacturing output. Well, today’s revisions go a long way toward bringing the GDP and industrial production data back into agreement.

In other words, the data as they now stand actually make sense. It was just a long, strange trip getting here.

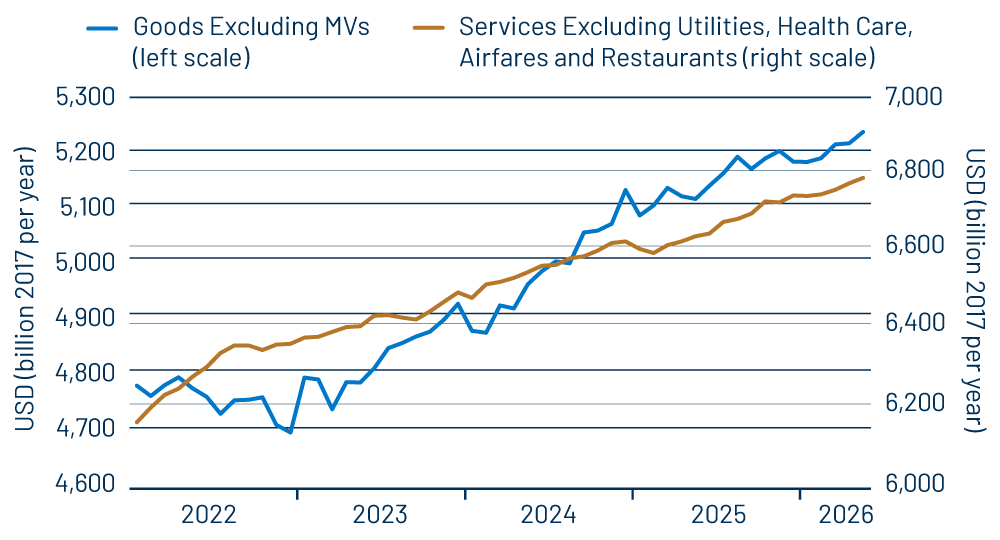

So, when the dust settles, where does the consumer stand? Well, again, the data actually show better performance lately for consumer spending on goods, as is evident from Exhibit 1. As you can also see there, consumer spending on services is still shown to be growing okay, just not as strongly as previously estimated. Services spending shows a little “wobble” in January and February but has resumed growth in the months since then.

As for the locations of the downward revisions to services spending, as large as they were, they were focused in just a few sectors. Health care spending was revised down slightly, recreational services and social services were revised down substantially, and motor vehicle services (repair, leasing and rentals) were revised down very sharply. Other services sectors actually saw upward revisions.

This is quite a complicated array of data. Our take has been that ever since the government shutdown ended, the data have evinced peculiarities. It was again so today, but again also, the data as currently portrayed are actually starting to make sense.

As for inflation, both headline and core Personal Consumption Expenditures (PCE) inflation registered relatively high monthly rates in May, with annualized monthly rates of 5.5% and 3.9%, respectively. Gas prices boosted headline inflation relative to core, and services prices rose sharply. Core goods prices declined, though, which finally brings PCE data back into accord with what the Consumer Price Index (CPI) is saying, for the month of May at least. With gas prices declining presently, both inflation measures look set to soften in June, and with goods prices behaving, there still looks to be little evidence of pass-through from Iran-affected fuel prices to the rest of the economy.