Performance Overview

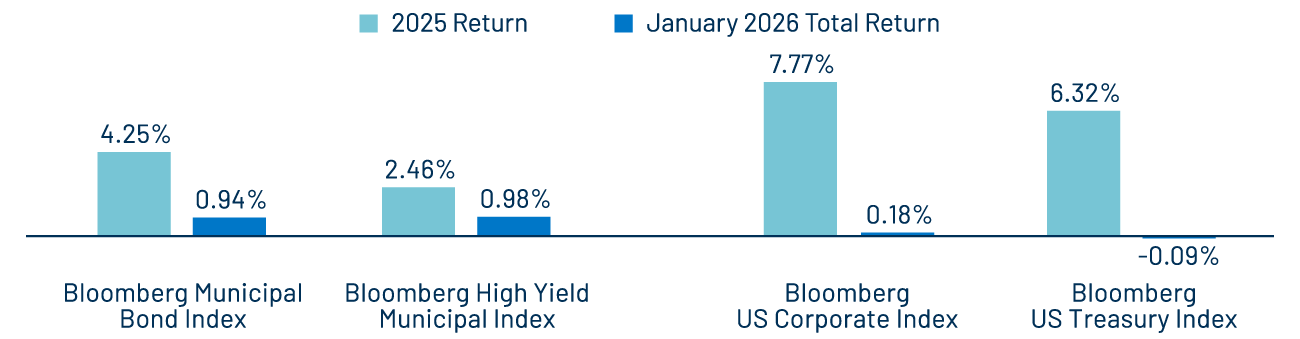

Municipals Outperformed in January, Partially Reversing 2025 Underperformance

Fixed-income markets were volatile in January amid elevated geopolitical tensions and trade threats. Yields moved higher mid-month following tariff threats related to President Trump’s effort to formally acquire Greenland, but ultimately eased as a framework with Europe was reached. Economic data was relatively steady and the labor market modestly softened as the unemployment rate increased slightly, offset by steady manufacturing data. The Federal Reserve kept rates steady, maintain the fed funds target rate range at 3.50%-3.75%.

The Treasury curve moved 3-5 basis points (bps) higher across the curve during the month. The high-grade municipal curve outperformed, with yields moving 13-20 bps lower in maturities inside of 20 years, and up to 5 bps higher in longer maturities. All told, the Bloomberg Municipal Bond Index returned 0.94%, outperforming the US Treasury and Corporate Indices which returned -0.09% and 0.18%, respectively, reversing some of the muni underperformance observed in 2025.

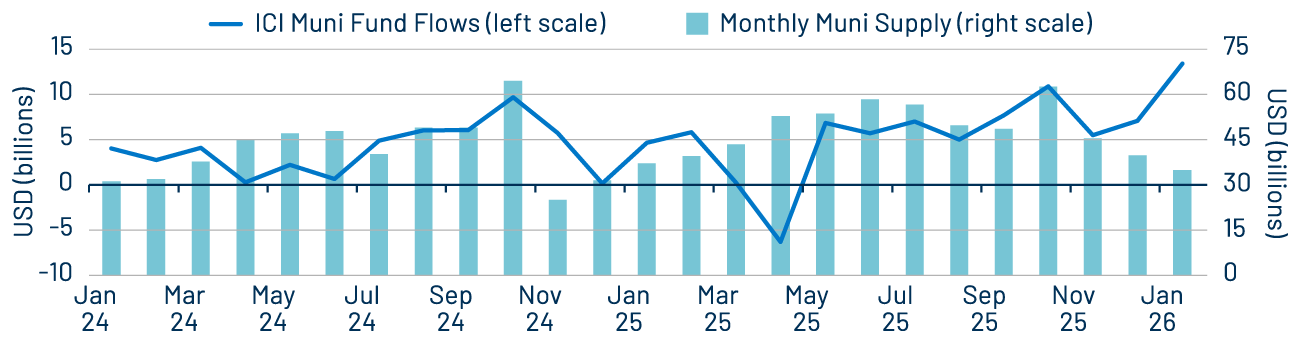

Technicals

Muni Demand Accelerated as Supply Declined

Muni outperformance was supported by traditional “January Effect” conditions, a period of technical strength where heavy coupon and principal reinvestment coincides with limited new issuance. ICI estimates municipal funds and ETFs recorded $13 billion of net inflows in January, the highest level since the market’s $120 billion major outflow cycle ended in early 2024. Meanwhile, monthly new-issue supply of $35 billion was down 6% from January 2025 levels and down 44% from the recent highs observed in October 2025, further strengthening market technicals.

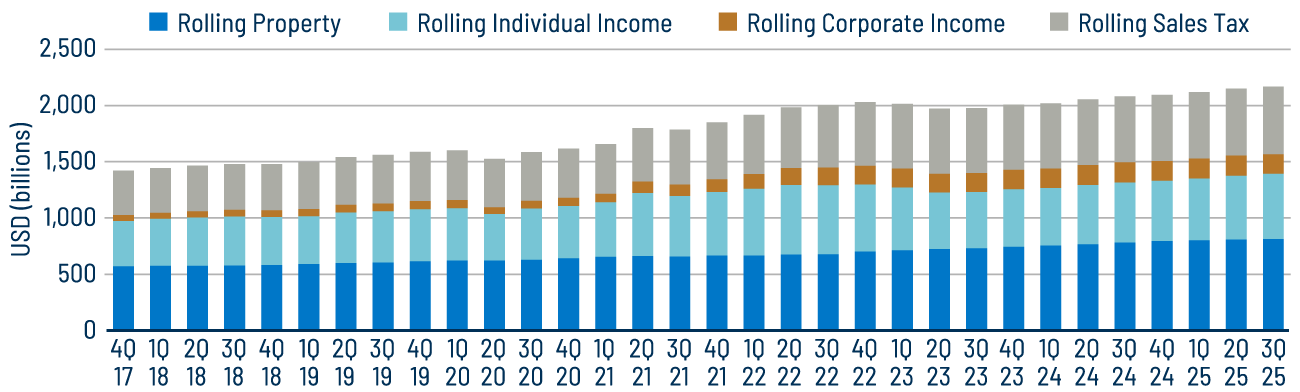

Fundamentals

Record Revenue Collections Support Muni Fundamentals

In January, the Census released 3Q25 state and local tax collection estimates, which were delayed due to the government shutdown, but underscored continued resilience for traditional state and local credit conditions. Twelve-month trailing collections increased 4.2% year-over-year (YoY) to $2.2 trillion, marking a record high, according to Census data. On a 12-month trailing basis, individual income tax collections increased 8.6% YoY and sales tax collections increased 2.6%, while corporate income tax collections declined 3.6%. Twelve-month rolling property tax collections increased 4.2% YoY.

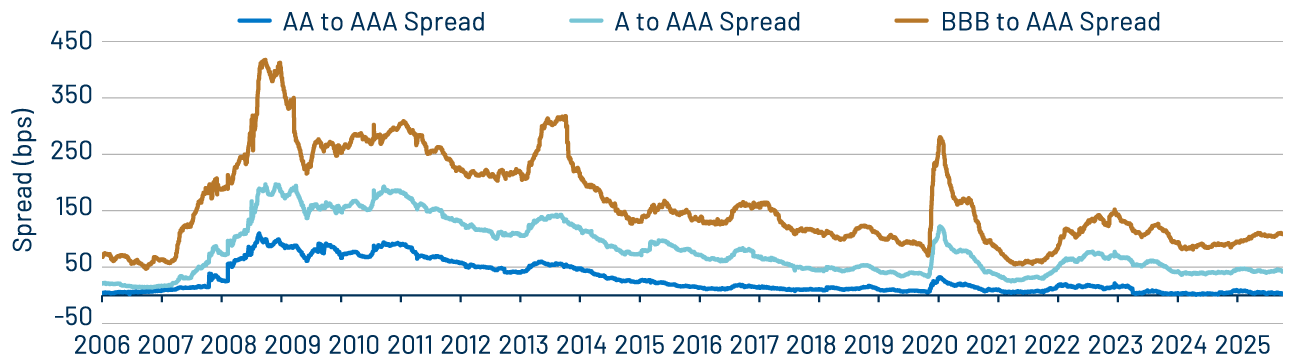

Valuations

Muni Credit Spreads Remain Tight, Warranting Diligent Credit Selection

Despite municipal yields moving lower with the yields of other fixed-income asset classes over the past year, tax-exempt income opportunities remain attractive compared with historical averages. Municipals offer a compelling after-tax yield pickup versus taxable counterparts, a trend that could continue as we transition out of “January effect” conditions into a weaker technical environment ahead of tax season. Given that tax-exempt credit spreads remain at historically tight levels, Western Asset emphasizes that diligent credit selection is paramount. Western Asset believes that long-term investors may be well-served by potential income opportunities offered by any upcoming seasonal weakness.