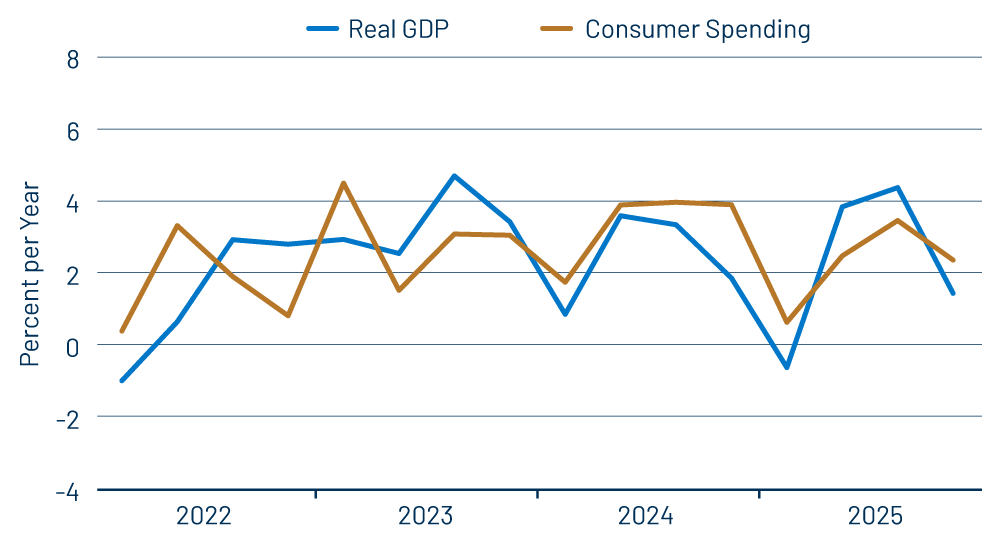

Fallen are the mighty! Not long ago, pundits were touting 5% annualized growth in the economy in 4Q. Instead, the actual advance estimate for growth at year-end came in at a scant 1.4%. What happened? We’ll walk through the details here.

First, keep in mind that the GDP data are always subject to wild swings in the short-term, and this is especially the case in the current era of Trump II, when various one-time distortions push growth up or down in one quarter, only for those factors to reverse subsequently. Thus, in 1Q25, US merchants anticipated the Trump tariffs and bulked up on imports from abroad, which worked to drive negative (-0.6%) growth in that quarter. When imports then moved back to normal, in 2Q and 3Q, growth jumped, coming in at 3.8% and 4.4%, respectively. That overstated mid-2025 growth was just the offset of understated growth in 1Q, as we remarked at the time.

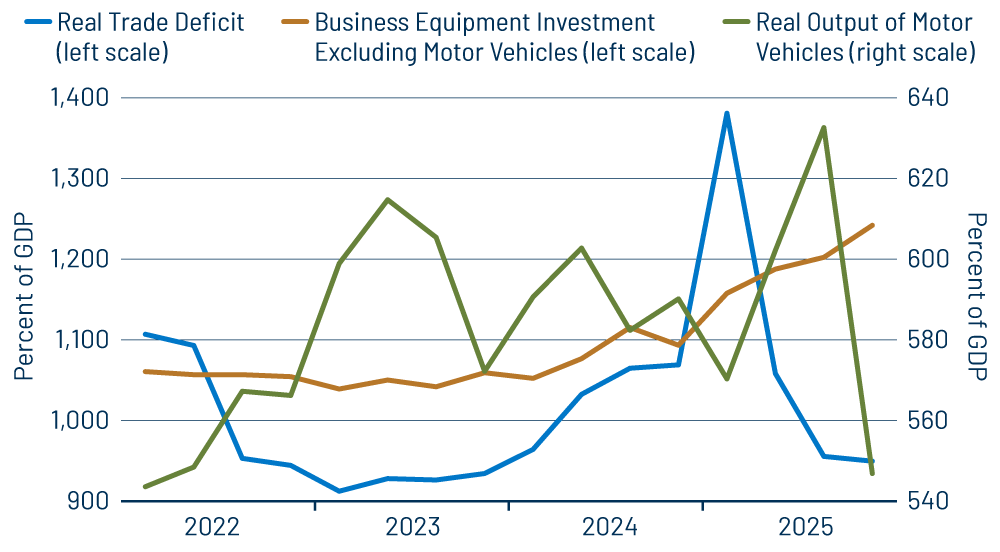

Fast forward to the present or, at least, 4Q25. US imports plunged and exports jumped in October, leading some analysts to expect a huge boost to 4Q growth from foreign trade, hence the 5% forecasts floating around in December. However, both imports and exports reverted to trend in November and December, so that the actual boost to 4Q GDP was slight (cf. Exhibit 2).

That by itself would have been enough to reduce 4Q growth to “normal,” say around 2.5% to 3.5%. In addition, however, two factors worked to pull reported growth yet lower. First, after bouncing in 2Q and 3Q, motor vehicle output reversed those gains, falling sharply in 4Q. Second, the federal government shutdown worked to sharply reduce government spending on payrolls and contractors in 4Q. Together, these two factors alone reduced 4Q GDP by 2.5 percentage points, with the drag from motor vehicles a bit larger than that from government payrolls.

There were other factors within 4Q GDP as well. Consumer spending growth slowed a bit, thanks to the lull in retail sales (thus goods consumption) discussed in our February 13 post. However, other factors worked to push up growth, such as the improvement in foreign trade already discussed and ongoing strong growth in business equipment investment.

Going forward, beneath the quarter-to-quarter noise, growth is actually picking up a bit, thanks to the faster growth in business investment. In 1Q26 and after, motor vehicle output is likely to rebound to “normal” levels, reversing some of the 4Q25 drag. Similarly, with the shutdown now over (for the moment?), federal spending on payrolls and contractors will also rebound sharply in 1Q. In sum, the 2.5 percentage-point drag from these sectors in 4Q will revert to a boost to growth of around 2 percentage points in 1Q. Finally, the 4Q lull in goods consumption could prove ephemeral, which would also work to boost growth reported in 2026.

Growth for all four quarters of 2025 came in at 2.2%, just below the 2.4% of 2024. Keep in mind that the 2025 growth tally is depressed by the especially low level of motor vehicle output (as seen in Exhibit 2) and federal payrolls in 4Q.

Last month, our assessment of the economy in 2025 was that the manufacturing sector had picked up, while the service and construction sector maintained about the same pace as in 2024. That assessment still stands after today’s data. Exhibit 1 shows quarterly growth rates are volatile but stable. The GDP data show stronger growth in goods-sector (i.e., manufacturing, etc.) GDP in 2025. The factors that restrained 4Q growth should reverse in 1Q and after, serving to overstate growth then just as 4Q growth was understated.