KEY TAKEAWAYS

- Now that interest rates have risen from their near-zero levels, the current environment presents an opportune time to implement a cash segmentation strategy.

- Preservation of capital is essential to successful short-term investing, but it is only meaningful when applied to a specific time frame.

- By assigning cash balances to different segments with differing time horizons, an investor is able to determine the appropriate level of risk for the overall investment, thus aiming to generate the highest level of return while still meeting the core objectives.

- Proper risk analysis is essential to any investment strategy, and it’s vital to see how a portfolio has performed in the past and how it is expected to perform in the future in times of extreme market stress.

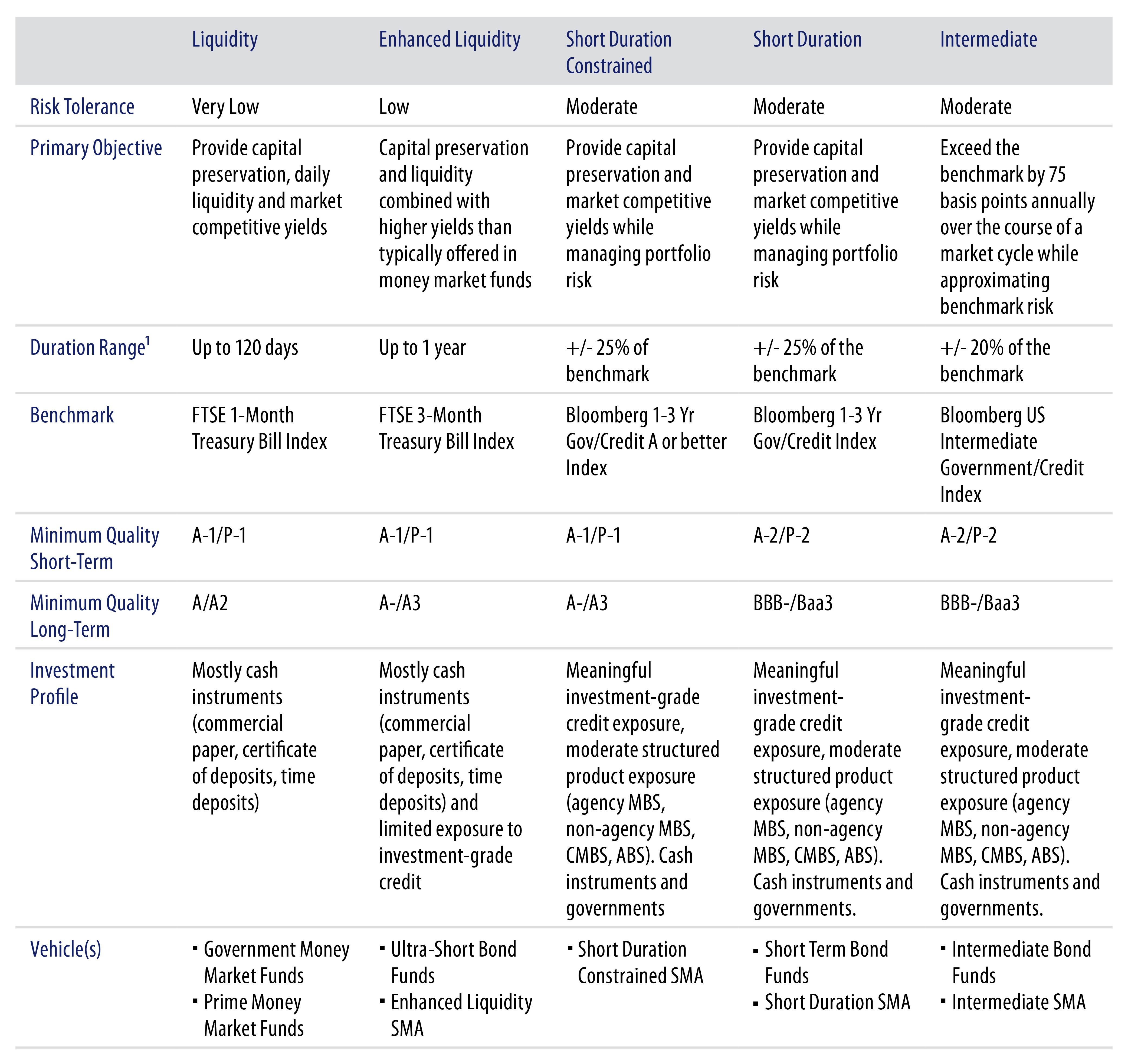

- Western Asset’s short-term investment strategies span the liquidity, maturity and risk spectrums from extremely conservative to those that combine a conservative base with the intention of generating returns incrementally higher than just cash.

Choosing the Right Short-Term Investment Strategy

Short-term investment strategies are generally defined as those using low-risk, fixed-income portfolios that range from money market funds (MMFs) to intermediate bond funds, or an equivalent in a customized separately managed account (SMA). Most short-term strategies will focus on the highest credit quality, meaning that portfolios will have a majority of their allocation in investment-grade bond issuers. Interest-rate risk is also kept to a low or moderate level by restricting investments to bonds maturing in under a year (in the case of MMFs) or up to a maximum of five years (in the case of an intermediate strategy), with a variety of different strategies in between.

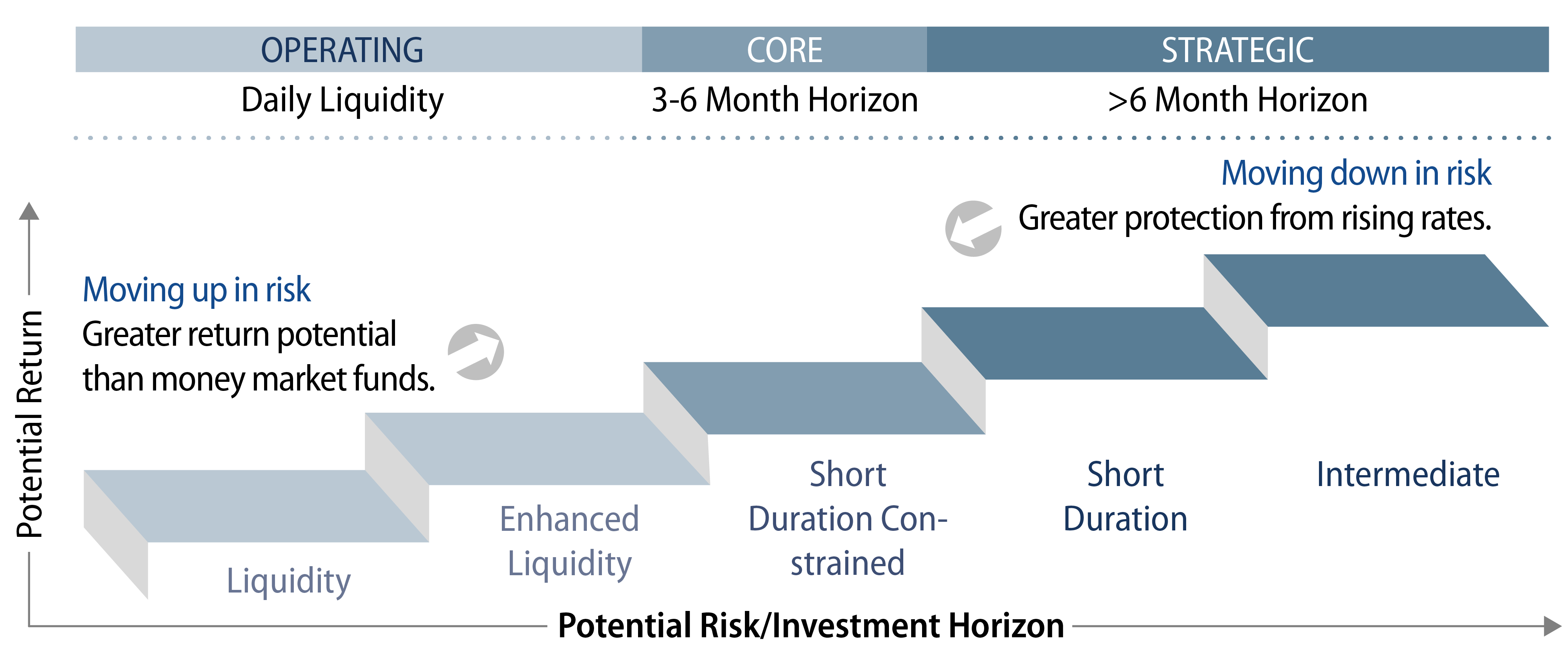

An MMF may be the best solution for cash that requires daily liquidity, but this high level of liquidity comes at a price. Setting an investment time horizon that is too low for your needs will give up valuable yield on the investment—an unwelcome result further pronounced in times of low interest rates. By lengthening the investment horizon and moving up in risk, the potential for greater returns can be obtained. Similarly, in times of heightened credit and interest-rate volatility, moving down in risk from longer-term fixed-income strategies—or even from other asset classes—can help investors to navigate times of increased market risk.

This paper looks at both of these approaches. Namely, the “up in risk” and “down in risk” investment allocation changes, which continue to make short-term strategies as valuable today as they have ever been, perhaps even more so.

Segmentation Provides the Framework to Move Up in Risk

At the heart of an investment strategy for traditional cash investors, such as corporate treasurers investing excess balance sheet cash, lie the critical interdependent objectives of preserving capital, maintaining adequate liquidity and generating an attractive level of return.

Although these goals will drive cash investment decisions, they often overlook one critical component: time. Only by assigning an investment horizon to balances—or segments—of cash can an investor effectively define what is meant by these objectives. Preservation of capital is certainly a worthwhile aim, but it is only really meaningful when applied to a specific time frame. For instance, the question should be asked of whether an investment needs to not lose money from one day to the next, or whether it is more important that the investment not lose money over a rolling time period such as three months. Could the need for liquidity occur on any given day without much warning, or will there likely be some degree of a notice period? By assigning cash balances to different segments with differing time horizons, an investor is able to determine the appropriate level of risk for the overall investment, thus aiming to generate the highest level of return while still meeting the core objectives.

The current interest-rate environment also presents an opportune time to implement a segmentation strategy. Although rates in the US have now risen from their near-zero levels, there still remains a cost to liquidity. Making an investment with an investment horizon that is too short for your needs represents leaving returns on the table at a time when additional yield can be meaningful. Similarly, the corporate credit environment remains robust as demonstrated by the current low level of negative rating changes for investment-grade companies. This suggests that increasing credit risk in an investment may now be prudent.

It should be noted that when considering an “up in risk” strategy change, particularly when that move is away from MMFs, yield is not always the same as return. The yield of a strategy represents the income received from the individual bonds held in the portfolio. The return delivered to an investor will only equal the yield if all of the bonds in the portfolio are held to maturity. This is typically the case for MMFs but not, however, for strategies investing in bonds that mature in one year or longer, as the portfolio manager will normally switch out of the bond into an alternative before the bond reaches maturity. For this reason the expected return for short-term strategies other than MMFs may be lower or higher than the quoted yield.

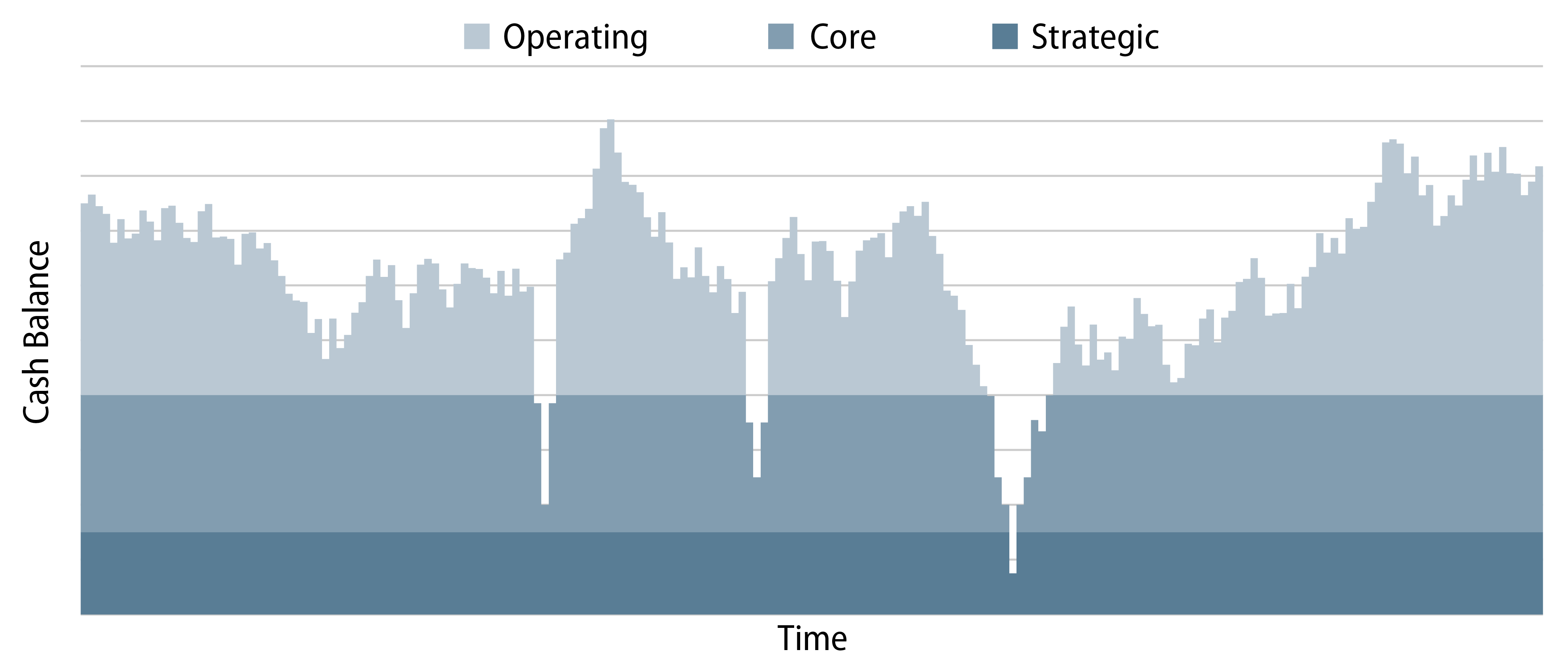

This approach to cash segmentation is only possible with a comprehensive forecast of cash flows. As the total cash balance is expected to fluctuate over time, discrete balances of cash can be aligned to differing investment horizons with associated risk and return objectives represented by distinct investment segments. For example, here’s what a cash segmentation approach could look like by the type of funds needed on hand and their associated investment horizons:

- Operating cash: daily liquidity

- Core allocation: 3-6 month horizon

- Strategic allocation: >6-month horizon

- Managing short-term investment strategies since 1975.

- AUM in short-term investments is $84.3 billion as of December 31, 2022 (includes Liquidity, Enhanced Liquidity, Short Duration and Short Duration Constrained portfolios).

Short-Term Strategies Within a Broader Portfolio Remain a Crucial Way to Move Down in Risk

Short-term strategies can be used in a broader, longer-term portfolio to address the following three significant investor concerns:

- Rising interest rates: Liquidity and other short-term strategies are generally less sensitive to interest rates and as a result may outperform longer-term strategies in an environment where rates, or even inflation, are rising. Additionally, strategies that include additional credit risk such as corporate bonds will generally offer an attractive tradeoff between yield and interest-rate risk when compared with longer-term fixed-income strategies that are more focused on US Treasuries (USTs) alone.

- Credit market deterioration: If an investor has a negative outlook for the credit market, for example, where they expect issuer downgrades—or even defaults—to become more frequent, then selecting a shorter-term strategy could provide more attractive returns. Generally in this scenario an allocation to shorter-term credit risk would outperform longer-term strategies as the probability of a negative credit event before a bond’s maturity becomes lower with the shorter time period left until that bond matures.

- Increased liquidity needs: Short-term strategies are also generally very liquid, especially those at the very short end of the spectrum. Including an allocation to short-term strategies will increase the average liquidity of an overall portfolio, which may aid future cash flows and rebalancing.

Implementing a “down in risk” strategy change to meet one or more of these views can help to satisfy minimum return targets. Short-term strategies are managed with the intent of generating incremental returns that beat benchmarks while appropriately managing risk. At the very short end, MMFs aim to beat a cash-like benchmark such as the three-month UST indices. At the longer end of the short-term spectrum, a strategy can take on more risk and aim to generate significant annualized outperformance versus a short duration benchmark, such as a 1-5 Year UST index.

Putting Short-Term Strategies in Their Place

An investment policy comes in two main parts: the objectives of the portfolio and the investments required to achieve those objectives. Although written separately, these parts, if chosen correctly, complement each other and are essentially one and the same. The objectives should directly imply the permitted investments and the permitted investments should directly imply the objectives. Reaching this duality can be achieved by extending the traditional approach for cash investors with the inclusion of techniques such as setting an investment horizon, performing cash segmentation and conducting a thorough risk analysis. Through this method the potential for greater returns can be achieved.

Furthermore, an investment strategy should also reflect the current and expected future conditions of the market. Short-term strategies can play a critical role in allowing an investor of a broader portfolio to express a bearish view though the reduction of both interest rate and credit risk, and therefore lowering the potential for a shortfall in return.

Western Asset Offers the Right Short-Term Solutions

Whether you are a cash investor looking to segment out your cash along only short-term strategies or you want to include a short-term strategy as part of your broader longer-term portfolio, we believe that Western Asset has the right solution to meet your needs. Our strategies span the liquidity, maturity and risk spectrums from extremely conservative (Cash Management and Enhanced Liquidity) to those that combine a conservative base with the objective of generating returns incrementally higher than cash alone (Short Duration Constrained, Short Duration and Intermediate). Maturities range from extremely short (0-3 months) out to intermediate strategies (1-5 years). Our most conservative strategies employ USTs and government securities, whereas those further out the risk spectrum may utilize a broader investment set.